Plate market participants predict more mill price hikes

Plate market participants expect additional base price hikes from domestic mills, something that has some eyeing imports.

Plate market participants expect additional base price hikes from domestic mills, something that has some eyeing imports.

A weekly guest column that examines North American steel issues leading up to the USMCA periodic review in July.

AISI, SMA, and the Canadian Steel Producers Association will each publish a monthly column in the lead-up to the USMCA periodic review.

President Donald Trump has threatened to raise tariffs on auto imports from the European Union to 25% from 15%.

The Canadian government has announced CAD$1.5 billion (USD$1.1 billion) in funding available to help companies impacted by US metals tariffs.

It's cliche to say it. But spring traditionally brings new hope and green shoots—whether that's looking forward to vacations or increased business activity. While I viscerally share these positive feelings, I can’t help but thinking of three areas where I'm not feeling very hopeful. Namely, the US electrical grid, the national debt, and the Iran war.

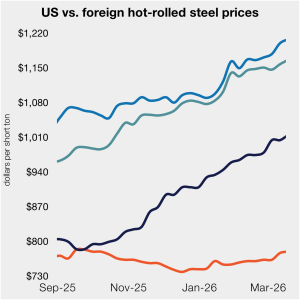

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week. The dynamic continues even as stateside and import prices diverged a bit vs. the prior week.

ArcelorMittal’s North American operations posted higher sales results sequentially and year over year (y/y) in its Q1 earnings report. The North American segment of the Luxembourg-based steelmaker reported 8.3% higher sales in Q1’26 compared with the previous quarter. The steelmaker credits higher average selling prices, up 3.5% from Q4, and a jump in steel shipments, up 5.2%.

The US Department of Commerce has released new procedures allowing certain steel and aluminum producers in Canada and Mexico to qualify for reduced Section 232 tariffs – but only if they commit to building new primary production capacity inside the United States.

Imports of various iron and steelmaking raw materials are eligible. These include pig iron, direct-reduced iron (DRI)/hot-briquetted iron (HBI), iron ore pellets, and ferroalloys, to name a few.

USMCA provides strong support for North American competitiveness. US manufacturing has lost considerable capabilities over the last few decades. “Cheating” by other countries is not the only reason. Nor is it even the most important reason

US Trade Representative Jamieson Greer said rules of origin will be a major focus of upcoming USMCA review talks.

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week. The dynamic continues as both stateside and offshore prices have largely trended higher.

The countdown continues. 123. That’s how many days before Steel Summit 2026 kicks off on Aug. 24 in Atlanta. And it looks like there will be no shortage of things to talk about.

The Canadian International Trade Tribunal (CITT) determined oil country tubular goods (OCTG) sold by Tenaris S.A. and certain exporters from South Korea, Turkey, and the Philippines are subject to antidumping tariffs.

Dozens of Canadian United Steelworkers (USW) labor union members lobbied federal politicians on Thursday, April 23 in Ottawa.

US Trade Representative (USTR) Jamieson Greer said Mexico should not expect the upcoming USMCA review to result in the removal of US steel and aluminum tariffs, according to media reports.

According to the latest findings from SMU’s survey, more respondents answered that President Trump’s tariff policies have been helpful to their businesses than in the prior survey.

North American steel buyers are signaling stronger interest in foreign material amid a tight market and rising global substrate costs, which are complicating purchasing decisions.

The construction market is seeing activity from data centers and the energy infrastructure to support them. But other factors are dragging the sector down: The Iran war is spiking inflation; tariffs are driving up material costs; and immigration crackdowns are hurting labor.

No doubt, events will scramble the status quo. Meanwhile, the global systems that have prevented major wars for 80 years are sagging.

The president’s April 2 proclamation restructures how derivative products are classified, valued, and tariffed – a shift that industry groups say will close loopholes but could raise costs for certain downstream imports.

If I had to sum it up, I’d say “pain at the pump” is back. AAA says gasoline now averages more than $4 per gallon nationally ($4.08 to be precise) for the first time in for years. Meanwhile, diesel prices average $5.40 per gallon, according to the US Energy Information Administration. That’s up $1.81 per gallon from a year ago.

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week.

The Trump administration has implemented changes to its steel and aluminum tariff framework that alter how duties are applied to imported manufactured goods, according to an April 2 presidential proclamation.

With global capacity projected to increase by 138 million mt by 2028, the gap between capacity and demand will continue to grow over the next three years. And that assumes the conflict in Iran does not stifle global demand.

CR imports from Germany, Italy, and Japan on a landed basis remain much more expensive than domestic product. But South Korean imports remain competitive, in theory, even with the 50% Section 232 tariff.

Most steel buyers see prices continuing to inch higher on stable or improving demand. But some are concerned higher energy prices stemming for the Iran war could dent the overall economy.

The price gap between US hot-rolled coil (HR) and landed offshore product remained within a tight band this week. The dynamic continues as both stateside and offshore prices have trended higher.

Ken Simonson, chief economist for The Associated General Contractors of America (AGC), will join SMU for a Community Chat webinar on Wednesday, April 15, at 11 a.m. ET.