Nucor lifts HR coil to $820/ton

Nucor has increased its consumer spot price (CSP) for hot-rolled (HR) coil for a fourth consecutive week.

Nucor has increased its consumer spot price (CSP) for hot-rolled (HR) coil for a fourth consecutive week.

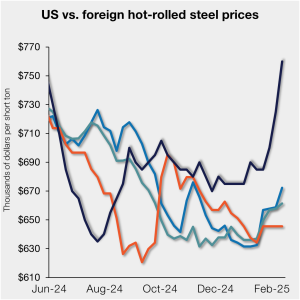

Hot-rolled (HR) coil prices rose further in the US this week, while tags abroad saw minor gains. The result: the margin US hot band holds over imports on a landed basis increased.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Josh Spoores, principal analyst at CRU, will be the featured speaker on the next SMU Community Chat webinar on Wednesday, Feb. 19, at 11 a.m. ET. The live webinar is free. A recording will be available for free to SMU members. You can register here.

Each of the steel product prices tracked by SMU saw significant increases this week. All four of our sheet price indices rose by $30-50 per short ton (st) on average. Plate prices popped $60/st compared to the week prior.

The new version of Section 232 goes into effect on 12:01 am ET on March 12, according to the executive order. The latest iteration of Section 232 removed quotas, exemptions, and other carve outs that had accumulated over years.

December 2024 marks the fourth month in a row that steel exports have declined, now at the lowest monthly rate recorded since December 2022.

President Donald Trump said he would announce 25% tariffs on all steel and aluminum imported to the US, according to Bloomberg. Trump said he would make an announcement about the matter on Monday. It was not clear when the tariffs might take effect.

Following the one-year low recorded in November, steel imports rose by 3% in December to 2.14 million short tons (st) according to final US Commerce Department data. January could be the highest month for steel imports witnessed in nearly three years.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

After reaching multi-month lows in mid-January, SMU’s Steel Buyers’ Sentiment Indices rebounded this week to some of the highest readings recorded in months.

While we have seen some movements in recent weeks, steel mill production times remain within a few days of the historical lows observed over the last two years, a trend observed since mid-2024.

Steel mill negotiation rates have declined in each of our last two surveys; this week’s rate is the lowest recorded since March 2024.

SMU’s steel price indices rose across the board this week. Sheet prices increased as much as $35 per short ton (st) compared to last week, while our average plate price ticked up by$10/st.

SMU’s Monthly Review provides a summary of important steel market metrics for the previous month. Our latest report includes data updated through January 31st.

Muted demand from the auto industry took a particular toll later in the year.

Nucor increased its consumer spot price (CSP) for hot-rolled (HR) coil to $775 per short ton (st) on Monday, Feb. 3. The $15/st week-on-week (w/w) rise marks the first back-to-back increases in the steelmaker’s weekly CSP since last August, according to SMU’s mill price announcement calendar. Nucor’s joint-venture subsidiary California Steel Industries (CSI) is also up […]

U.S. Steel has increased sheet prices by $50 per short ton (st), according to market participants. The Pittsburgh-based steelmaker has also set a new target price of $800/st for hot-rolled (HR) coil, they said.

Prices for the seven steelmaking raw materials SMU tracks moved in differing directions from December to January, according to our latest analysis.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

SMU’s sheet prices were mixed this week. Hot-rolled (HR) coil and plate notched gains while prices for coated products stagnated or dipped lower. Our HR price now stands at $700 per short ton (st) on average, up $15/st from last week and marking the highest level for HR prices since $705/st in early October. SMU’s […]

Nucor increased its consumer spot price (CSP) for hot-rolled (HR) coil to $760 per short ton (st) on Monday, Jan. 21. The $10/st week-on-week (w/w) rise marks the first increase in the CSP since Nov. 12. According to SMU’s mill price announcement calendar, the Charlotte, N.C.-based steelmaker held the weekly price at $750/st for 11 […]

The volume of crude steel produced around the world declined 2% month over month (m/m) in December, according to the World Steel Association (worldsteel). This is the second-consecutive monthly decline in production, following November’s 3% m/m drop.

SMU’s Steel Buyers’ Sentiment Indices saw a slight decline this week, slipping to levels last observed in early November

Steel mill lead times were mixed across the sheet and plate products SMU tracks, according to buyers responding to our latest market survey.

The majority of steel buyers we canvassed this week continue to report that mills are willing to negotiate prices on new spot orders, though not as much as they were in early-January.

The latest SMU Community Chat webinar reply is now available on our website to all members. After logging in at steelmarketupdate.com, visit the community tab and look under the “previous webinars” section of the dropdown menu. All past Community Chat webinars are also available under that selection. If you need help accessing the webinar replay, or if your company […]

Sheet and plate prices remained in a holding pattern this week as the market awaited more specifics on potential Trump administration tariffs.

Recent Federal Reserve data indicates that the US manufacturing sector remains healthy and stable. The strength of the manufacturing economy has a direct relationship to the health of the steel industry.

The 106” Mill was part of Algoma's plate and strip combination facility.