SMU survey: Lead times slip for most sheet and plate products

Most steel products tracked by SMU saw lead times contract this week from two weeks earlier, according to SMU’s most recent survey data.

Most steel products tracked by SMU saw lead times contract this week from two weeks earlier, according to SMU’s most recent survey data.

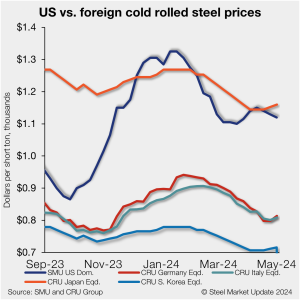

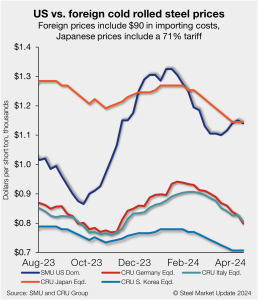

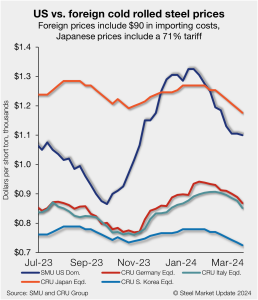

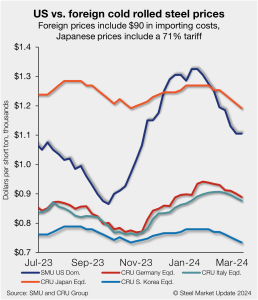

Foreign cold-rolled (CR) coil remains much less expensive than domestic product even as domestic prices continue to decline, according to SMU’s latest check of the market.

Olympic Steel logged lower earnings in the first quarter of 2024, but the company said all three of its segments contributed to profitability.

Russel Metals’ earnings fell in the first quarter, but the Toronto-based metals distributor sees steel prices stabilizing in the near term and staying above historical averages.

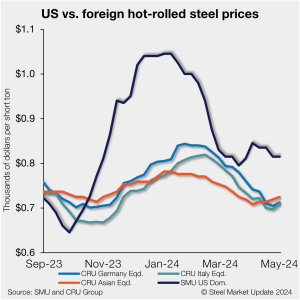

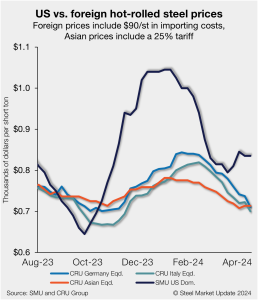

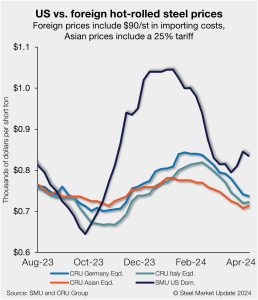

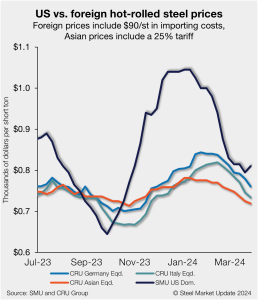

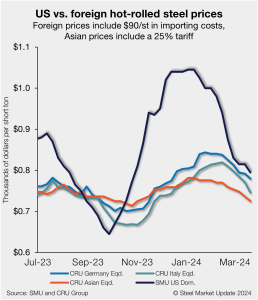

US hot-rolled (HR) coil price premium over offshore hot band has tightened on the back of lower domestic tags, though stateside HR coil remains markedly more expensive than imports.

Foreign cold-rolled (CR) coil remains much less expensive than domestic product, according to SMU’s latest check of the market.

Hot-rolled coil and plate lead times contracted this week, with most other products remaining flat, according to SMU's most recent survey data. Cold-rolled products, however, saw lead times extend 0.1 weeks to an average of 7.5 weeks vs. two weeks earlier. Hot rolled and plate lead times both contracted 0.3 weeks from our last market check.

US hot-rolled (HR) coil remains more expensive than offshore hot band, though with a tighter premium as prices stateside and abroad have ticked lower in recent weeks.

Foreign cold-rolled (CR) coil remains less expensive than domestic product, according to SMU’s latest check of the market.

While general economic conditions across the US improved slightly over the last six weeks, activity in the manufacturing sector was weak, according to the Fed’s latest Beige Book report.

US hot-rolled (HR) coil has become gradually more expensive than offshore hot band in recent weeks, as stateside prices have stabilized while imports moved lower.

Metalformers expect economic activity to remain level over the next three months, according to the April Business Conditions Report from the Precision Metalforming Association (PMA).

Flat Rolled = 58.3 shipping days of supply Plate = 60.6 shipping days of supply Flat Rolled US service center flat-rolled steel inventories edged up in March as shipments remained low. At the end of March, service centers carried 58.3 shipping days of supply on an adjusted basis, up from 56.6 shipping days in February. […]

As we navigate through the first half of 2024, we are seeing early signs of an inflationary rate environment for flatbed shipping, albeit slightly later than anticipated. Excess supply has persisted longer than expected for both flatbed and dry van, resulting in rates remaining lower than for longer than anticipated.

While shipping and supply chains have always been subject to wars, pirates, privateers, geopolitical issues, and natural disasters, it seems that “it’s been busier lately when it comes to dealing with significant supply chain disruptions,” according to logistics expert Anton Posner.

The market appears to be taking a pause after the heavy buying that occurred in March.

US hot-rolled (HR) coil has become increasingly more expensive than offshore hot band as stateside prices have moved higher at a sharper pace vs. imports.

Steel Dynamics Inc. (SDI) has announced new roles for current executives James Anderson and Chad Bickford. SDI said James Anderson will take over responsibility and oversight for the company's long products group, effective May 1.

After stabilizing in our last check of the market, production times for flat-rolled steel have begun to push out further, according to steel buyers responding to SMU's market survey this week.

US hot-rolled coil and offshore hot band moved further away from parity this week as stateside prices have begun to move higher in response to mill increases.

Metalformers are expecting business conditions to remain steady over the next few months, according to the March Business Conditions Report from the Precision Metalforming Association.

A container ship collided with the Francis Scott Key Bridge in Baltimore on March 26, causing it to collapse. This has blocked sea lanes into and out of Baltimore port, which is the largest source of US seaborne thermal coal exports. The port usually exports 1–1.5 million metric tons (mt) of thermal coal per month. It is uncertain when sea shipping will be restored. But it could be several weeks or more. There are coal export terminals in Virginia, though diversion to these ports would raise costs.

SMU’s sheet prices firmed up modestly this week, even as CME hot rolled futures declined. What gives? My channel checks suggest that demand remains stable and that buyers have returned to the market following new HR base prices announced by mills earlier this month. I’m looking forward to seeing whether lead times, which have stabilized, will start extending. SMU will have more to share on that front when we release updated lead time figures on Thursday. As for HR futures, what a reversal! As David Feldstein wrote last Thursday, bulls expected mill price increase announcements. And we briefly saw the May contract climb as high as ~$1,000 per short ton (st).

Foreign cold-rolled (CR) coil remains notably less expensive than domestic product even with repeated tag declines across all regions, according to SMU’s latest check of the market.

US hot-rolled coil (HRC) remains more expensive than offshore hot band but continues to move closer to parity as prices decline further. The premium domestic product had over imports for roughly five months now remains near parity as tags abroad and stateside inch down.

SMU caught up with Barry Zekelman, executive chairman and CEO of Zekelman Industries, on Wednesday’s Community Chat. As one of the largest independent steel pipe and tube manufacturers in North America, his company is also one of the largest steel buyers in the region. This year alone, the Chicago-based company will buy roughly 2.8 million tons of steel. As such, Zekelman provides a great perspective on the steel industry and the markets it serves.

The spot rate trend in the flatbeds has seen a positive upturn. There are potential rate accelerators and decelerators, however, likely to influence spot and contract flatbed rates. The flatbed market for spot rates is showing signs of improvement as we move through the new year. February increased slightly from January, marking the third consecutive […]

Foreign cold-rolled coil (CR) remains significantly less expensive than domestic product even as US tags continue to decline in a hurry, according to SMU’s latest check of the market.

Flat Rolled = 56.6 Shipping Days of Supply Plate = 58.8 Shipping Days of Supply Flat Rolled After weaker-than-expected shipments in January, US service center shipments of flat-rolled steel picked up in February, which caused supply to decrease. At the end of February, service centers carried 56.6 shipping days of flat-rolled steel supply on an […]

Steel mill lead times were flat to slightly up, according to our market survey this week.