Final Thoughts

Waiting for possibly more changes to tariffs.

Waiting for possibly more changes to tariffs.

The US House of Representatives voted on a resolution on Wednesday, Feb. 11, to disapprove of President Trump's national emergency declaration that led to the imposition of tariffs on Canada.

I want to say a big thank you to everyone who attended the Tampa Steel Conference. More than 600 people – smashing the record we set last year.

Last week, news stories (first in the Financial Times) appeared that the Trump administration was working on adjustments to steel and aluminum derivative tariffs. Ostensibly, these tariffs are only imposed on the steel or aluminum “content” of derivative products. But Customs has not provided clear guidance on how to calculate content. Confusion and controversy are running rampant.

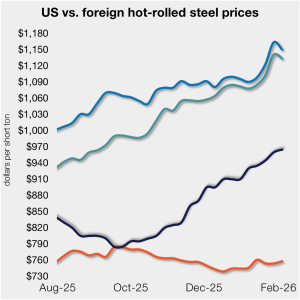

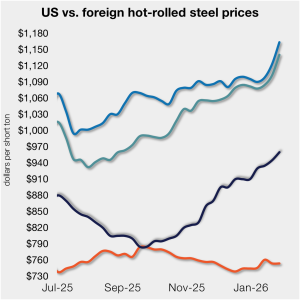

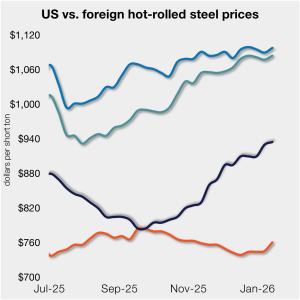

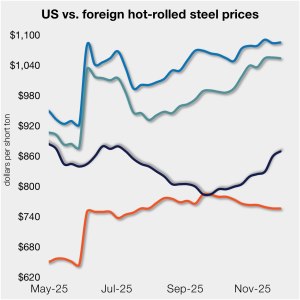

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product was largely flat this week, as price movements stateside and abroad mirrored each other. Still, the premium for US hot band over imports has remained in a relatively tight band since early December.

Former smelter sites have become increasingly attractive to data center developers competing for electricity to support AI.

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

The Tampa Steel Conference will kick off just a few days after the Super Bowl, and I think it’s fair to say that we could be reacting to market developments in real time – again.

There is no evidence that unofficial talks are taking place to secure tariff reductions on Canadian aluminum or steel. One of the biggest challenges is simply understanding what the US actually wants from Canada.

Tariffs affect different parts of the economy differently. Tariffs on steel imports have contributed to price increases from domestic mills, improving their bottom lines. But orders from customers are slowing down, hurting downstream industries’ profitability and job prospects.

A coalition of US steel industry CEOs has formally urged President Trump to maintain—and fully enforce—current Section 232 tariffs on steel and steel‑containing goods.

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.

The price gap between US hot-rolled coil (HR) and landed offshore product has been relatively flat to begin the year.

CSN LLC General Director Jerry Richardson will join Steel Market Update (SMU) for a Community Chat on Wednesday, Jan. 21, at 11 am ET.

As we move into 2026, it’s time to look forward. While the “Donroe Doctrine,” Venezuela, and Greenland absorb significant press attention, important trade developments will also continue to make headlines this year. The unprecedented changes we saw in 2025 will continue in 2026, particularly in the areas of IEEPA and tariffs, USMCA, and the WTO.

We will examine the wisdom of hedging from the perspective of both the LME and Midwest premium, and whether you are approaching the market as a buyer or a seller.

Canadian Prime Minister Mark Carney said the US probably won't reduce tariffs on steel, aluminum, and other goods from Canada anytime soon.

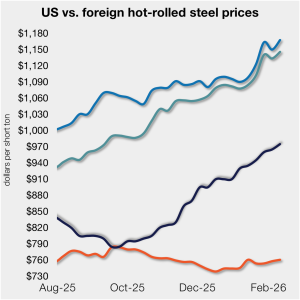

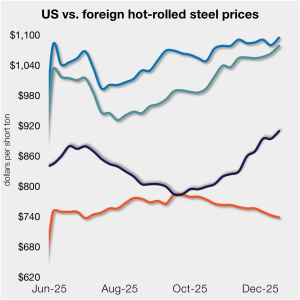

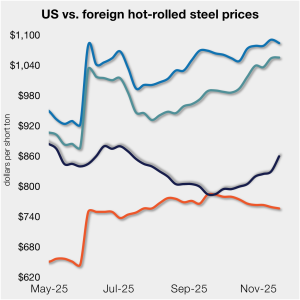

The price gap between stateside hot band and landed offshore product continues to narrow, inching closer toward parity. The premium is now, on average, at its lowest level since July.

The European Commission is aiming to have Section 232 tariffs eased on steel and aluminum, with a special eye towards derivative products as well, as it negotiates with the Trump administration, according to a report in Politico on Dec. 15.

In our opinion, it is striking that for all the bold talk about establishing a "common external tariff" — or "Fortress North America" — the solutions being proposed fail to live up to their promises. As we have commented recently, USMCA certainly needs a rethink. But we have serious concerns about Canadian and Mexican proposals that suggest common trade policies that are, as we see it, more illusory than effective.

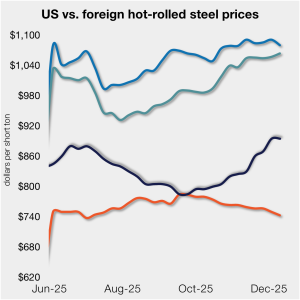

The price gap between stateside hot band and landed offshore product continues to narrow toward parity, now at its lowest level in five months.

SMU and AMU are pleased to announced that Wells Fargo Managing Director Timna Tanners will be joining us for a Community Chat webinar next Wednesday, Dec. 17, at 11 am ET.

U.S. Steel has begun the process of restarting the 'B' blast furnace at its Granite City Works near St. Louis. “After several months of carefully analyzing customer demand, we made the decision to restart a blast furnace,” U.S. Steel President and CEO David B. Burritt said in a statement on Thursday afternoon.

It's important to keep in mind - maybe especially for those of us in the US - that the rest of the world can act too. And I think we're already seeing signs of that action, or at least that's been my takeaway from some of SMU's recent reporting and from Community Chat webinars for both SMU and AMU.

The Coalition for a Prosperous America (CPA) is urging the Trump administration to keep Section 232 steel and aluminum measures focused on rebuilding US capacity, rather than using them as bargaining chips in unrelated negotiations.

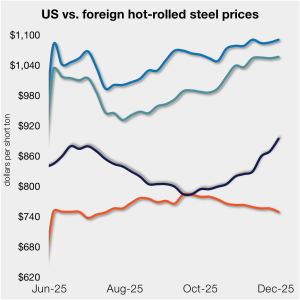

The price gap between stateside hot band and landed offshore product has inched closer to parity, now at its lowest level since the summer.

The price gap between stateside hot band and landed offshore product tightened further this week, as the average price for domestic hot-rolled was $10/st higher w/w.

Wiley attorneys Alan Price and Ted Brackmeyer argue that significant changes to the USMCA and continued Section 232 tariffs on Canada and Mexico are needed to support American steelmaking.

The price gap between stateside hot band and landed offshore product shrank week over week (w/w).

The SMU Steel Demand Index slackened from late October, remaining below expansion territory, according to SMU's mid-November indicators.