Steel buyers ignore tariff noise amid slow summer market

Section 232 tariffs have doubled to 50%. Reciprocal tariffs rates remain uncertain. But while prices have softened on even softer sentiment, tariffs have firmed the floor.

Section 232 tariffs have doubled to 50%. Reciprocal tariffs rates remain uncertain. But while prices have softened on even softer sentiment, tariffs have firmed the floor.

Chinese steel export prices are expected to rise and support prices across most of Asia in the coming month. In Europe, buyers are likely to frontload import orders ahead of CBAM imposition, while new trade agreements are likely to emerge in the US. Steel prices in the APAC are expected to rise, except in India […]

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

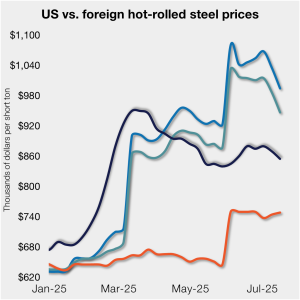

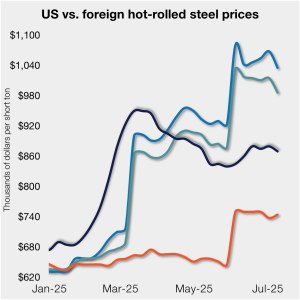

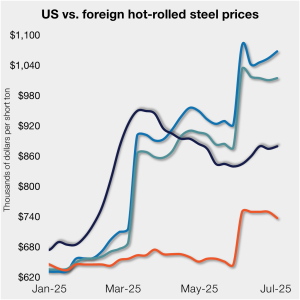

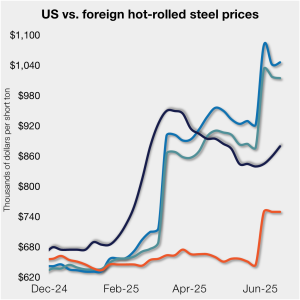

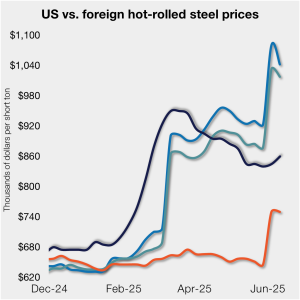

Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

US sheet and plate prices were flat or lower as reduced import volumes were offset by so-so demand.

Hot-rolled (HR) coil prices in the US ticked down this week but have fluctuated little over the past month. Stateside tags continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

Domestic mills are more open to talk price on new orders than they were in June, according to most steel buyers responding to our market survey this week. Negotiation rates have recovered from the early-June lull and are now just a few percentage points shy of the high levels seen late last year.

We can interpret that managed money still has expectations of price strength while physical participants are running closer to a balance on a net basis.

It will be a shorter week as the United States celebrates Independence Day on Friday. But we won’t leave you high and dry.

David Schollaert presents this week's analysis of hot-rolled coil prices, foreign vs. domestic.

Steel buyers this week are lamenting weak demand, cautious buying, and So. Much. Uncertainty. I'm no doctor, but I suggest a dual diagnosis of extreme tariff fatigue and early-onset summer doldrums.

Sheet and plate prices were little changed in the shortened week ahead of Independence Day, according to SMU’s latest check of the market.

Nucor aims to keep plate prices flat again with the opening of its August order book.

The majority of steel buyers responding to our latest market survey say domestic mills are more willing to talk price on sheet and plate products than they were earlier this month. Sheet negotiation rates rebounded across the board compared to early June, while our plate negotiation rate hit a full 100%.

As of June 24, the premium galvanized coil carries over hot-rolled coil is just $5 per short ton (st) above the lowest level recorded in almost two years.

Prices for steel sheet slipped this week despite Section 232 tariffs remaining at 50% and a US strike on nuclear facilities in Iran over the weekend.

Nucor maintained its weekly list price for hot-rolled (HR) coil this week, following two consecutive increases.

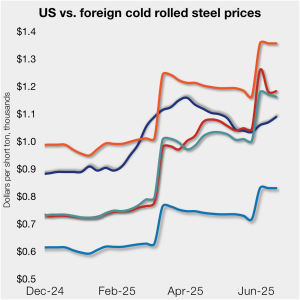

US cold-rolled (CR) coil prices continued to tick higher this week, while offshore markets were mixed.

According to our latest analysis, prices for four of the seven steelmaking raw materials we track declined from May to June. Collectively, these materials declined 3% month over month (m/m) and are down 9% compared to three months ago.

Several steel market sources say they were blindsided when mills increased spot prices for hot-rolled coils this week.

US hot-rolled coil prices crept up again this week but still trail imports from Europe.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Steel prices inched higher again this week across most of the sheet and plate products tracked by SMU.

Nucor raised its published weekly spot price for hot-rolled (HR) coil by $10 per short ton (st) on Monday.

Most steel buyers responding to our market survey this week reported that domestic mills are considerably less willing to talk price on sheet products than they were in recent weeks, but remain open to bargain on plate prices.

Domestic hot-rolled (HR) coil prices edged up marginally again this week, while offshore prices ticked down.

Steel prices climbed for a second straight week across all five sheet and plate products tracked by SMU.

The increases are effective June 6.

US manufacturers brace for the implications spurred by the latest round of Section 232 tariffs.

A fierce flat price rally started this week that saw the nearby months rally by over $120/ short tons, exceeding the contract highs seen in February ahead of the first batch of tariffs.