HARDI: Galv market conditions signal firmer terrain in 2026

The galvanized steel market is navigating price increases and longer lead times with a surer footing than in prior months.

The galvanized steel market is navigating price increases and longer lead times with a surer footing than in prior months.

Since late 2025, mills have begun to hold a firmer stance on prices, tightening their grip at the start of this year and holding on since

Once wintery weather gives way to sunnier spring conditions, plate sources foresee the market accepting the $50-60 per short ton spot price increases issued by Nucor Plate Group, Oregon Steel Mills, and SSAB.

Three of SMU’s price indices increased this week, while two remained steady, all holding at multi-month highs.

SSAB Americas wants to increase plate prices by at least $60 per short ton, $10 more than rival Nucor’s price hike last week.

Nucor increased its list price for hot-rolled (HR) coil to $980 per short ton (st) on Monday, up $5/st from last week.

Nucor on Friday announced plans to increase plate prices by $50 per short ton (st).

CRU: US Midwest sheet prices have continued to rise from our mid-January assessment.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

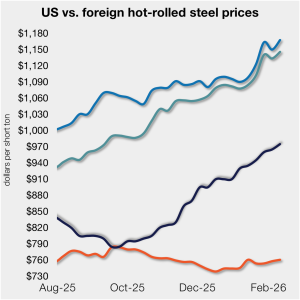

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product was largely flat this week, as price movements stateside and abroad mirrored each other. Still, the premium for US hot band over imports has remained in a relatively tight band since early December.

SMU’s sheet price indices inched up to new multi-month highs this week, while plate prices held steady.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $975 per short ton (st), up $5/st from last week.

Plate market participants expect domestic producers to issue a $40-60 per short ton (st) price increase.

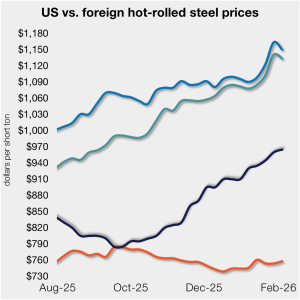

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

US rebar and wire rod prices rose month on month (m/m) alongside continued scrap increases, while merchant bar and structurals were unchanged.

One third of the steel buyers responding to our market survey this week reported that domestic mills are negotiable on new spot order pricing. Mills began to hold a firmer stance on prices towards the end of last year, tightening their grip in early January and holding it since.

Sheet market participants said conditions this week were more stable than in past weeks, but they remain cautiously optimistic overall.

Flat-rolled steel prices inched upward again this week as mixed demand appeared to be offset by limited supplies.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $970 per short ton, up $5/st from last week.

Participants in the hot- and cold-rolled coil markets said winter storms in the East and Midwest may disrupt weekly order volumes and prices.

At SMU, we ask the big questions: To be or not to be? Hot band at a grand? On the one hand, whether hot-rolled coil price can or can’t go above $1,000 per short (st) is a silly argument. It’s just a number. On the other hand, round numbers are something that we tend to fixate on. They can be psychologically important to a market – even if they shouldn’t be.

All but one of the steelmaking raw materials we track increased in price over the last month

SMU polled steel buyers on an array of topics earlier this week, ranging from market prices and demand, to inventories, imports, and evolving market events.

What do SMU's latest survey results show about the current market take on tariffs and where HRC prices are going?

Sheet prices mostly continued their uneven but steady march higher this week, according to SMU’s latest check of the market.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $965 per short ton (st), up $5/st vs. the prior week.

A report on the sheet market this week.

Lower finished steel imports continued to support US domestic prices this month. HR coil prices are up more than $40 per metric ton (mt) month-on-month (m/m) due to higher seasonal demand in January and tightening domestic supply.

The plate market’s swell of optimistic sentiment marking the start of 2026 dissipated this week.

The price gap between US hot-rolled coil (HR) and landed offshore product has been relatively flat to begin the year.