Galvanized prices maintain big premium over HR

Prices for hot-rolled (HR) coil in recent weeks have been declining faster than those for galvanized sheet, resulting in a growing price spread between the two steel products.

Prices for hot-rolled (HR) coil in recent weeks have been declining faster than those for galvanized sheet, resulting in a growing price spread between the two steel products.

Wolfe Research Managing Director Timna Tanners cautioned clients about the darkening clouds of a brewing steel sheet storm in the company's Basic Materials Weekly Webcast on Monday. “This one we’ve been talking about for a while, and we feel like the theme is coalescing here,” she said.

What's the tea in the steel industry this week? Here's the latest SMU gossip column! Just kidding... kind of. Yes, some of the comments we receive in our weekly flat-rolled market steel buyers' survey are honestly too much to put into print. Some make us laugh. Some make us cringe. Some are cryptic. Most are serious. We appreciate them all. Below are some highlights from our survey results this week. Some of the comments that we can share with you are also included, in italics, in the buyers' own words, with minimal editing on our part.

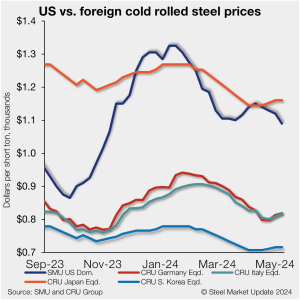

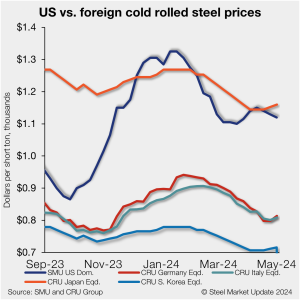

Offshore cold-rolled (CR) coil prices remain much less expensive than domestic product, even as domestic prices have slipped to a six-month low, according to SMU’s latest check of the market.

The Mexican federal government backed down on the application of tariffs on raw non-alloyed and alloyed aluminum decreed on April 22.

In this Premium analysis we cover North American oil and natural gas prices, drilling rig activity, and crude oil stock levels.

Steel Market Update’s Steel Demand Index fell eight points, and back into contraction territory, an indication demand might be slipping as prices have trended lower, according to our latest survey data.

The latest SMU market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Historical survey results are also available under that selection. If you need help accessing the survey results, or if […]

Japanese steelmaker JFE Holdings will invest abroad as part of a drive to lift income, says group president Yoshihisa Kitano.

Last week we wrote about a brief lull in price movement, labeling it a period of wait and see. It did, in fact, turn out to be pretty brief. This week... things are little bit different. Perhaps right now we are more in a period of "hope and pray" or "Here we go, hold on to your hats."

Steel prices trickled lower across the month of April for both sheet and plate products.

Stelco reported a positive start to 2024 in its first-quarter earnings report on Thursday. And with steady demand and a stable market, the Canadian flat-rolled steelmaker is optimistic for the remainder of the year.

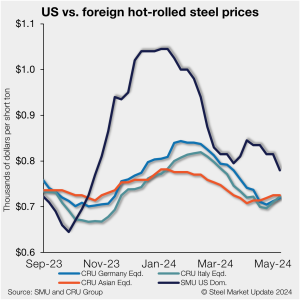

US hot-rolled (HR) coil prices declined again, tightening their premium over offshore hot band, and moving closer to parity.

Hot rolled, cold rolled, and plate buyers said mills are more willing to talk price on spot orders this week, while the overall negotiation rate for products SMU surveys remained level, according to our most recent survey data.

Most steel products tracked by SMU saw lead times contract this week from two weeks earlier, according to SMU’s most recent survey data.

Klöckner & Co. logged a wider net loss in the first quarter on-year, but the Duisburg, Germany-based service center group expects higher shipments and sales in the upcoming three months.

After a considerable wait, the market for ferrous scrap for May shipment has started to form.

Unless you've been under a rock, you know by know that Nucor's published HR price for this week is $760 per short ton, down $65/st from the company’s $825/st a week ago. I could use more colorful words. But I think it’s safe to say that most of the market was not expecting this. For starters, US sheet mills never announce price decreases. (OK, not never. It has come to my attention that Severstal North America rescinded a price increase back on Feb. 14, 2012. And it caused quite the ruckus.)

Sheet prices fell across the board this week – largely in response to Nucor’s $65-per-short-ton price cut for hot-rolled (HR) coil on Monday morning. SMU’s HR coil price is $780/st on average, a $35/st decrease week over week (w/w). Our average cold-rolled coil price is $1,090/st (down $30/st w/w). Our galvanized base price is $1,100/st […]

Turkish scrap import prices were stable last week. CRU’s assessment for HMS1/2 80:20 and shredded was unchanged at $384 per metric ton (mt) CFR and $408/mt, respectively.

When we were asked to provide some additional commentary to SMU about the futures markets for flat rolled, our only reluctance to contribute was rooted merely in the fact that SMU (1) already offers an excellent array of authors on this topic and (2) a concern regarding what new ground could be covered that hasn’t already been discussed to death on this issue. Thankfully, however, Nucor has offered up something we can describe, without hyperbole, as simply revolutionary for spot pricing in flat rolled - a development that we simply could not resist commenting on with respect to its probable impacts on the futures market.

Nucor started off May with a bang, dropping its weekly base spot price for hot-rolled (HR) coil by $65 per short ton (st) this week.

Is it just me, or does it seem like the summer doldrums might have arrived a little early? I could be wrong there. It’s possible we could see a jump in prices should buyers need to step back into the market to restock. I’ll be curious to see what service center inventories are when we update those figures on May 15. In the meantime, just about everyone we survey thinks HR prices have peaked or soon will. (See slide 17 in the April 26 survey.) Lead times have flattened out. And some of you tell me that you’re starting to see signs of them pulling back. (We’ll know more when we update our lead time data on Thursday.)

The election campaign is white-hot right now, and the Biden administration is touting its protectionist message. Just this past week, the Office of the US Trade Representative (USTR) touted this message. In a release entitled “What They are Saying,” USTR quoted many of the usual protectionist groups praising government action against Chinese steel exports and shipbuilding. Consuming industries in the United States, which employ many times the American workers as the industries seeking trade protection, were not mentioned.

US announces new import duties on aluminum extrusions The US Department of Commerce has placed preliminary antidumping (AD) duties of 2-600% on imports of aluminum extrusions from 14 countries. The rates are: “[The findings] show just how widespread dumping practices are globally and highlight the importance of strongly enforcing the antidumping laws to shield US […]

Foreign cold-rolled (CR) coil remains much less expensive than domestic product even as domestic prices continue to decline, according to SMU’s latest check of the market.

Olympic Steel logged lower earnings in the first quarter of 2024, but the company said all three of its segments contributed to profitability.

Brazil’s chamber of foreign trade, Camex, has approved quotas on imports of 11 steel products and a 25% levy on shipments 30% above a product’s average import volume between 2020 and 2022.

As we approach “buy week,” a term industry veterans use to refer to steel mill scrap buying time and an excuse to remain in the office, we have seen a variety of slants on the May market.

Everybody has a plan… until they’ve dealt with volatility in the HRC market. While Mike Tyson’s original quote was about getting punched in the mouth, it’s unlikely the ex-champ has gone many pricing rounds with hot-rolled coil.