US CR, import prices trend higher

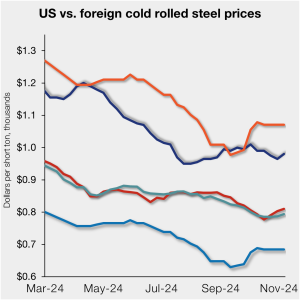

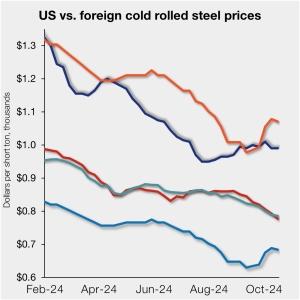

The price spread between US-produced cold-rolled (CR) coil and offshore products remained largely flat in the week ended Nov. 8, on a landed basis.

The price spread between US-produced cold-rolled (CR) coil and offshore products remained largely flat in the week ended Nov. 8, on a landed basis.

Russel Metals Inc.’s profit shrank during the third quarter as steel prices continued to be volatile.

Most steel buyers polled in our market poll this week continue to report mills are open to negotiation on new order pricing. In fact, negotiation rates have been strong for the majority of 2024, trending higher since September.

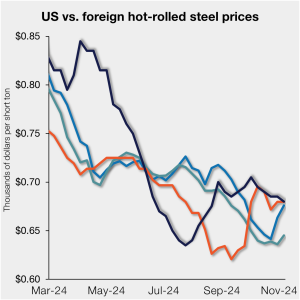

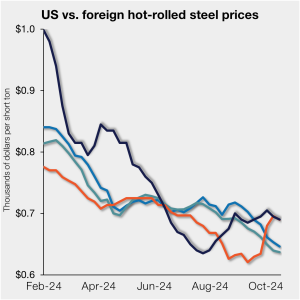

US hot-rolled (HR) coil prices moved lower this past week while tags in offshore markets were largely higher. Domestic tags are again nearly level with imports on a landed basis.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on the next SMU Community Chat. The webinar will be on Wednesday, Nov. 13, at 11 am ET. It’s free to attend. You can register here. Timna – who has coined Sheet Storm, Scrap Squeeze, and Galv Galore – is one of the most popular guests on our Community Chats. Her insights and forecasts are always thought-provoking.

Votes were still being counted when this column posted on Tuesday evening. And I’d be surprised if we know who the president will be by the time some of you are reading it on Wednesday morning.

SMU price indices edged lower this week for all products but one, marking the fifth consecutive week of overall declining prices.

Nucor’s weekly consumer spot price (CSP) for hot-rolled coil was unchanged week on week at $740 per short ton as of Monday, Nov. 4.

Next week promises to be a big week for the country. Could even top the World Series (congrats to the Dodgers). As we all hold our breath to see what happens next, it’s a good time to reflect.

The premium galvanized-coil prices carry over hot-rolled (HR) coil continues to decline following the uptick seen earlier this year.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Nucor Corp. announced that its plate mill group would cut prices for as-rolled, discrete, and cut-to-length plate with the opening of its December order book.

Nucor said it is seeking $740 per short ton (st) for hot-rolled (HR) coil this week, up $20/st from last week. USS, meanwhile, is shooting for up $30/st for sheet products in general. (USS did not announce a target price for HR.)

SMU price indices declined again this week for all products other than hot-rolled sheet. Our indices have trended lower across October, falling as much as $75 per short ton (st) in that time.

Nucor has raised its weekly consumer spot price (CSP) for hot-rolled (HR) coil by $20 per short ton (st), now at $740/st as of Monday, Oct. 28.

US plate prices are at their lowest level in almost four years, and less than half of what they were when they reached an all-time high of $1,940 per short ton (st) in May 2022.

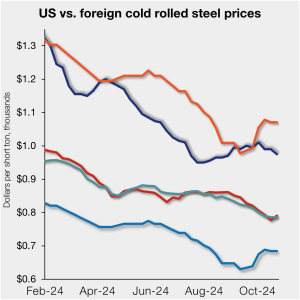

The price spread between US-produced cold-rolled (CR) coil and offshore products was negligibly tighter in the week ended Oct. 25, on a landed basis.

U.S. Steel plans to increase sheet prices by at least $30 per short ton (st). That's something we haven't seen for a while.

SSAB Americas plans to increase plate prices by at least $60 per short to, according to a letter to customers dated Thursday, Oct. 24. The higher prices are effective immediately for all new non-contract orders scheduled to ship on or after Dec. 2.

More than nine out of every 10 steel buyers polled by SMU this week reported that mills are flexible on prices for new orders. Negotiation rates have been strong since April and on the rise since early September.

U.S. Steel aims to increase spot prices for all new orders of flat-rolled steel by at least $30 per short ton (st), according to an internal letter dated Thursday.

US hot-rolled (HR) coil prices moved lower again this past week. A similar trend was seen in offshore markets, keeping domestic tags marginally above imports on a landed basis.

SMU's hot-rolled (HR) coil price slipped this week to $685 per short ton (st) on average. We also adjusted our sheet momentum indicators to lower for the first time since July.

Steel prices ticked lower again this week for most of the products SMU tracks. Our indices have declined as much as $40 per short ton (st) across the last four weeks.

Steelmaking raw material prices strengthened for all but one product in October, a change in pace compared to recent months, according to SMU’s latest analysis.

Nucor is holding its hot-rolled coil consumer spot price at $720/short ton this week.

The price spread between US-produced cold-rolled (CR) coil and offshore products was negligibly wider in the week ended Oct. 18, on a landed basis.

We had an October surprise here at SMU on Wednesday. I was working from the CRU office in Pittsburgh, and the internet connection briefly went out. As luck would have it, that happened smack in the middle of a live Community Chat webinar. Fortunately, my colleague David Schollaert stepped in, Zekelman Industries CEO Barry Zekelman rolled with the punches – and the show went on. Could there be any more October surprises in store for us and for the steel market?

US hot-rolled (HR) coil prices slipped again this past week, mirroring movement in offshore markets. This kept domestic tags marginally higher than imports on a landed basis.

Prices, demand, inventories, evolving market events... What are buyers and sellers of steel talking about this week?