Nucor maintains $720/ton HR base price

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil is unchanged from last week.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil is unchanged from last week.

We got a little flack for adjusting our sheet momentum indicators to neutral last week. To be clear, we didn’t adjust them to lower. Part of the reason we moved them to neutral was because there are some unusual cross-currents in the current market. On the news side, you could make a case that there should nowhere to go but up.

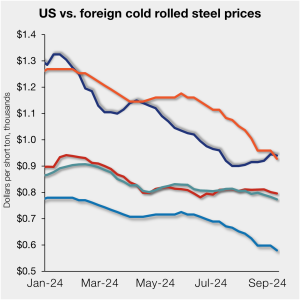

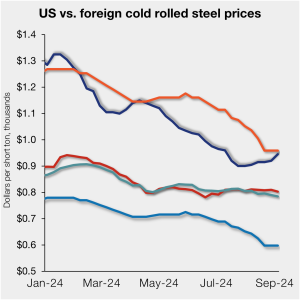

The price gap between US cold-rolled (CR) coil and offshore product is a bit broader this week despite slightly lower tags stateside. The premium is still widening since falling to a 10-month low in late July.

The US plate market finds itself in unfamiliar territory, well maybe unfamiliar territory for this side of the post-Covid “normal,” that is.

Negotiation rates have edged lower from our previous market check, a downward trend witnesses since July.

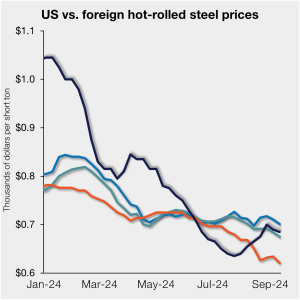

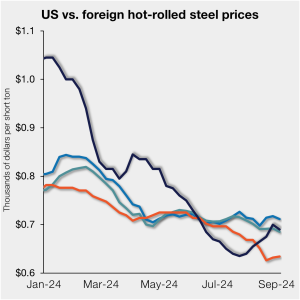

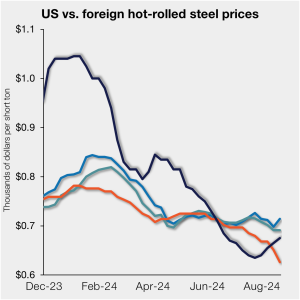

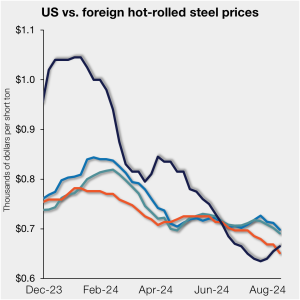

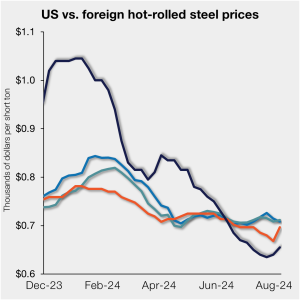

US hot-rolled (HR) coil prices edged down slightly this past week but remain at a slight premium to offshore material on a landed basis.

SMU’s steel price indices showed mixed signals for a second consecutive week. Our hot rolled, cold rolled, and plate price indices inched lower from last week, as the galvanized index held steady and Galvalume's ticked higher.

The price gap between US cold-rolled (CR) coil and offshore product has widened again. The premium has grown repeatedly since falling to a 10-month low in late July.

US hot-rolled (HR) coil prices were largely flat over the past week, remaining higher than tags for offshore material on a landed basis for a second consecutive week.

Nucor intends to keep plate prices unchanged with the opening of its October order book, according to a letter to customers dated Wednesday, Sept. 4. The Charlotte, N.C.-based steelmaker said it would maintain prices set in its July 1, 2024, price letter.

SMU indices moved higher on cold rolled products this week, while galvanized prices were flat. Our indices for plate, hot rolled, and Galvalume all edged lower.

SMU’s Monthly Review provides a summary of important steel market metrics for the previous month. Our August report includes data updated through August 30th.

“It's been a very interesting year in that the price of scrap should have gone down earlier this year."

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil is unchanged from last week.

Steel buyers found mills slightly more willing to negotiate spot prices this week, according to our most recent survey data. Though this negotiation rate has ticked up vs. our previous market check, overall rates have been trending downward since July’s highs.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil increased $15 per short ton (st) from last week to $710/st.

Steelmaking raw material prices have moved in differing directions across August, a change of pace from the declines seen in June and July, according to SMU’s latest analysis.

US hot-rolled (HR) coil prices continue to inch up and are now roughly even with prices for offshore material on a landed basis. The closing of the gap between cheaper US prices and more expensive import tags was driven by improving domestic prices on the heels of firmer US mill offers. SMU’s check of the […]

Cleveland-Cliffs aims to fetch $730 per short ton (st) for hot-rolled coil, up $30/st from its last published price. The steelmaker said the move was effectively immediately and “due to ongoing market developments” in a letter to customers on Wednesday, Aug. 21.

Sheet prices trended sideways to modestly up this week in a market that appears to be in “wait-and-see” mode.

Nucor increased its consumer spot price (CSP) for hot-rolled (HR) coil to $695 per short ton (st), up $5/st from last week.

Three out of four of our market survey respondents report that steel mills are open to negotiating new order prices this week, a slight decline compared to our previous market check.

This Premium analysis covers North American oil and natural gas prices, drilling rig activity, and crude oil stock levels. Trends in energy prices and rig counts are an advanced indicator of demand for oil country tubular goods (OCTG), line pipe, and other steel products.

US hot-rolled (HR) coil prices are nearly even with prices for offshore material on a landed basis as domestic tags continue to inch up.

SMU’s sheet prices increased across the board this week, marking the third consecutive week of rising prices, while plate prices held stable.

The countdown is on! In less than two weeks, we’ll kick off the 2024 SMU Steel Summit. This year is poised to be the best attended yet. More than 1,350 delegates have already registered – so we’re within sight of last year’s record number of nearly 1,450. I’m looking forward to learning from executives across […]

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil is unchanged from last week at $690/ton.

I asked in a prior Final Thoughts where some of you thought Nucor’s weekly spot HR price would land. One opinion: $720 per short ton (st). That would allow the Charlotte, N.C.-based steelmaker to one up competitor Cleveland-Cliffs and to re-establish its position as a market leader.

US hot-rolled (HR) coil remains cheaper than offshore material on a landed basis despite domestic tags inflecting upward lately. But the spread between domestic and foreign HR has tightened on the heels of price hikes by US mill over the past two weeks. (Visit SMU’s price increase calendar to keep track of the latest mill price announcements).

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.