SDI Q2 earnings fall, but 'pivot point to the upside' seen for prices

Steel Dynamics Inc.’s (SDI’s) earnings slid in the second quarter, but the company's top executive believes steel tags are set to rise.

Steel Dynamics Inc.’s (SDI’s) earnings slid in the second quarter, but the company's top executive believes steel tags are set to rise.

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed for the third consecutive month, hitting a level not seen since 2020, according to SMU’s most recent pricing data.

There are just 40 days left until the 2024 SMU Steel Summit gets underway on Aug. 26 at the Georgia International Convention Center (GICC) in Atlanta. And I’m pleased to announce that it's official now: More than 1,000 people have registered to at attend! Another big development: The desktop version of the networking app for the event has officially launched!

Cleveland-Cliffs has been pursuing M&A opportunities for some time now and thinks it has found a solid partner with aligned interests in Stelco. The companies announced on Monday that Cliffs would acquire the integrated Canadian steelmaker. That same day, Cliffs held a conference call with analysts to discuss the acquisition. Lourenco Goncalves, Cliffs’ chairman, president, […]

SMU’s hot-rolled coil price fell to $640 per short ton (st) on average on Tuesday. That’s down $10/st from last week and marks the lowest point for HR prices since December 2022, according to our pricing archives. SMU’s HR price is now $5/ton below 2023’s low of $645/st, which occurred against the backdrop of a United Auto Workers (UAW) union strike.

Flat Rolled = 60.9 Shipping Days of Supply Plate = 59 Shipping Days of Supply Flat Rolled US service center flat-rolled steel supply remained high at the end of June at 60.9 shipping days of supply, according to adjusted SMU data. This translates to 3.05 months of supply in June. At the end of May, […]

Scrap prices came in mostly sideways in July, with prime scrap prices edging down while shredded and HMS tags ticked up slightly, scrap sources told SMU. They believe a bottom has been reached in the market.

Nucor dropped its consumer spot price (CSP) for hot-rolled coil to $650 per short ton, down $20/st from last week. The Charlotte, N.C.-based steelmaker also said base prices for HR from CSI, its subsidiary in California, would be $720/st. That’s a $30/st decrease from $750/st a week ago.

There are a lot of rumors swirling around the steel market over the last couple of weeks. Chief among them was that we might see a price hike after Independence Day. Another concerns a key detail in the new Section 232 agreement with Mexico. Namely, steel imported from Brazil into Mexico. Of particular interest is its potential implication for slabs imported from Brazil, rolled in Mexico, and then exported to the US.

A month ago, when we last presented this column, there was a surprising amount of optimism in the presumably imminent reversal of the downtrend in hot-rolled steel prices in the second half of this year.

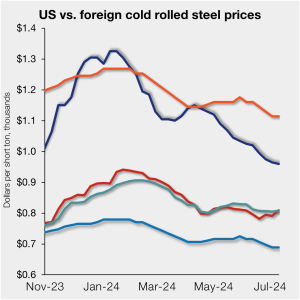

Offshore cold-rolled (CR) coil remains cheaper than domestic product. The gap continues to tighten, however, as US CR coil prices slip to a nine-month low. Domestic CR coil tags averaged $960 per short ton (st) in our check of the market on Tuesday, July 9, down $5/st from the week before. CR tags are now […]

Global Plate prices declined in all regions this week amid slow seasonal demand. With bearish outlooks on demand in the near term, market participants are watching how mills will react to low order entry levels and short lead times. In the US and China, production has been steady, but in Europe, steel mills are contemplating […]

A roundup of CRU aluminum news.

Renewable energy infrastructure, including wind turbines, solar farms, and electric-vehicle charging stations, requires substantial amounts of steel. The domestic steel industry, with its capacity to produce world-class steel with the world’s smallest carbon footprint, should be at the forefront of this supply chain. Yet the United States is increasingly importing steel from abroad to meet its renewable energy needs.

The ferrous scrap export market on the Atlantic and Gulf Coasts of North America has maintained its pricing for several months despite continuing declines in domestic markets.

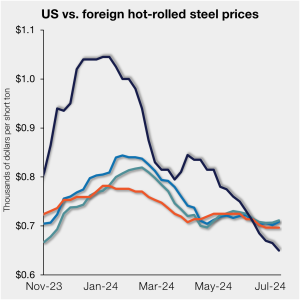

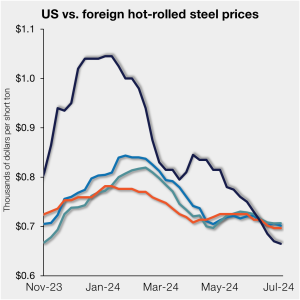

US hot-rolled (HR) coil prices continued to drift lower this week, falling further below imported hot band tags on a landed basis. SMU’s check of the market on Tuesday, July 9, put domestic HR coil tags at $650 per short ton (st) on average, down $15/st vs. last week. Domestic HR coil prices are now […]

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Flat-rolled steel prices have been largely falling since the beginning of the year. Even after a slight bump in early April when mills tried to halt the downtrend, the decrease resumed.

US sheet prices saw a similar pattern this week, customary for much of the year – new week, lower prices. Domestic tags moved lower this week, aligning with the typically slower summer period – but maybe a further indication of dwindling demand.

Nucor has kept its consumer spot price (CSP) for hot-rolled (HR) coil flat this week.

First off, we hope everyone had a safe and happy July 4th holiday, with fireworks seen and BBQs attended. Many parts of the country are quite toasty at the moment, signaling that, yes, summer has indeed arrived. And looking at our most recent survey results, the summer doldrums have arrived as well.

The latest SMU market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.”

US hot-rolled (HR) coil prices fell again this week – now on a 13-week run – causing tags to drift further below offshore hot band prices on a landed basis.

After celebrating the July 4th holiday, let’s have a look back at the first half of 2024.

Steel mill lead times remain near some of the lowest levels witnessed in months, according to our latest market canvass to steel service centers and manufacturers.

Radius Recycling continued to bleed red in its most recent quarterly report as it negotiated persistently challenging conditions in the recycled metals market.

Sheet steel buyers found mills more willing to negotiate spot pricing this week, according to our most recent survey data.

Most longs prices in the US were unchanged this month, except for rebar, which declined by $1.50/cwt ($30/short ton) m/m. While end-use demand is stable, inventories are well-stocked, keeping purchases limited. Domestic availability is sufficient to meet current demand, hindering the appetite for imported material. Meanwhile, prices for scrap remained under pressure in June, with […]

US sheet prices moved lower again this week, continuing a trend seen since early April. The slowdown aligns with the typical summer doldrums, when lax demand and shorter lead times often take center stage. The current market is also characterized by ample supply and concerns about restocking – especially with few signs of a bottom […]

It’s been a slow start to the week as far as news goes, something you’d expect ahead of a shortened Independence Day week. That said, it’s not as if transactions have completely ground to a halt. (Prices continue to drift lower.) And while news might be slow, rumors of low-priced deals, price hikes, and trade cases seem to have filled that void.