Cliffs opens May spot order book at $975/ton HR

Cleveland-Cliffs opened its May order book for spot material at $975 per short ton (st).

Cleveland-Cliffs opened its May order book for spot material at $975 per short ton (st).

US scrap prices declined in April for all the grades tracked by SMU amid tariff uncertainty, according to market sources.

SMU’s Steel Demand Index growth eased again, according to early April indicators. The slowdown comes after the index reached a four-year high in late February.

This week is the first time all of our indices have moved lower in unison since July 2024.

Nucor’s consumer spot price (CSP) for hot-rolled (HR) coil remains unchanged again this week. The pause over the past two weeks stands in contrast to the nine-week rally that saw the company increase prices regularly by double-digits. The Charlotte, N.C.-based steelmaker told customers on Monday that this week’s consumer spot price (CSP) for HR coil […]

Four out of every five steel buyers who responded to our latest market survey say domestic mills are unwilling to negotiate on new order spot pricing. Mills have shown little flexibility on pricing for nearly two months.

Sheet and plate prices were mixed on Tuesday as the market took a wait-and-see approach to the Trump administration’s “Liberation Day” tariffs.

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through March 31.

Nucor paused its weekly hot-rolled (HR) coil price this week, keeping it flat for the first time since Jan. 21. This comes after a nine-week rally that saw the company increase prices by double-digits for eight of those weeks.

Nucor aims to increase prices for steel plate by $40 per short ton (st) with the opening of its May order book. The Charlotte, N.C.-based steelmaker said the increase was effective with new orders received on Friday, March 28, in a letter to customers dated the same day. The company said the price hike applied […]

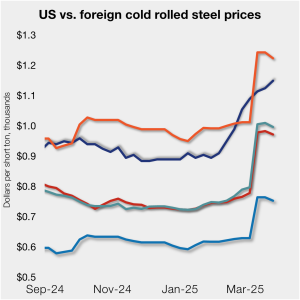

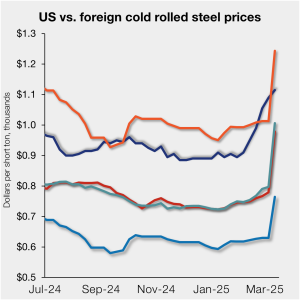

US cold-rolled (CR) coil prices increased again this week, while offshore prices declined.

A personal perspective on Galvalume prices from SMU analyst Brett Linton.

This week, SMU polled steel buyers on an array of topics, including market prices, demand, tariff policies, inventories, imports, and emerging market events.

Steel Market Update is pleased to share this Premium content with Executive members. Contact info@steelmarketupdate.com for information on how to upgrade to a Premium-level subscription. Growth in SMU’s Steel Demand Index eased in March after reaching a four-year high in late February. Despite a moderate gain, the index remains in expansion territory. The Steel Demand […]

SMU's steel price indices moved in differing directions this week but remained largely stable as cautious buyers await clarity on pending steel tariffs and trade cases.

Have we hit a bit of a lull when it comes to the recent price bump? Mills certainly capitalized on the threat of tariffs and the unknown, with much that still could unfold.

SSAB Americas aims to increase plate prices by at least $60 per short ton (st) ahead of opening their May order book.

US cold-rolled (CR) coil prices moved higher this week, a trend not evenly shared by offshore prices.

The majority of the steel buyers responding to our latest market survey continue to report that domestic mills remain firm on pricing, showing little willingness to talk price on new spot orders this week.

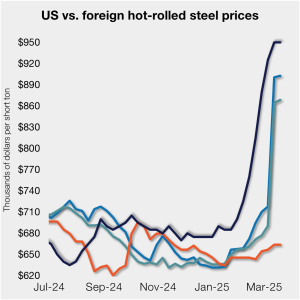

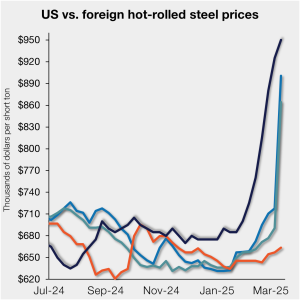

Domestic hot-rolled (HR) coil prices were flat this week, a trend mirrored in offshore markets.

In this Premium analysis we explore North American oil and natural gas prices, drilling activity, and crude oil stock levels.

Steel prices were stable to higher this week for the second consecutive week across the sheet and plate products tracked by SMU. Three of our price indices increased from the previous week, while two held firm.

Demand is up, but tariffs raise concerns

Prices for five of the seven steelmaking raw materials tracked by SMU increased from February to March, according to our latest analysis.

This marks the eighth week of increases

Fully restored Section 232 tariffs on steel on March 12 cut the widening premium US prices had over most imports on a landed basis.

Domestic hot-rolled (HR) coil prices moved higher this week, still largely outpacing increases seen in offshore markets. But the reinstatement of undiluted Section 232 tariffs on steel on March 12 cut the ballooning premium stateside prices had gained on most imports on a landed basis. The premium stateside tags had over prices abroad stood at […]

What are steel buyers saying this week about prices, demand, the import market, the evolving tariff situation, and more?

After over a month of increases, steel prices paused this week for some of the products tracked by SMU. Three of our price indices continued to climb, while two held steady from the prior week.

Manufacturing activity exhibited slight to modest increases across a majority of districts. However, manufacturers expressed concerns over the potential impact of looming trade policy changes between late January and February.