Chicago Business Barometer drops in August

The Chicago Business Barometer, a leading indicator for the broader US economy, remains in contraction, slipping 5.6 points to 41.5 in August.

The Chicago Business Barometer, a leading indicator for the broader US economy, remains in contraction, slipping 5.6 points to 41.5 in August.

Another record-breaking SMU Steel Summit is in the books. Thanks to all of you – attendees, speakers, sponsors, and exhibitors – for making it possible it in what has been an uncertain year for steel.

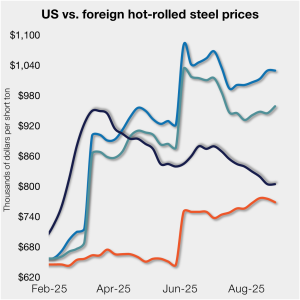

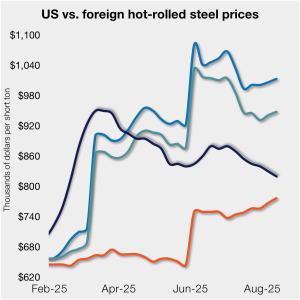

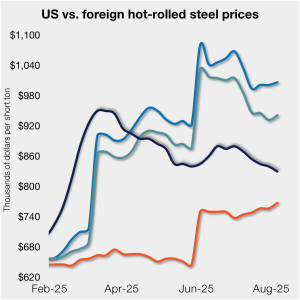

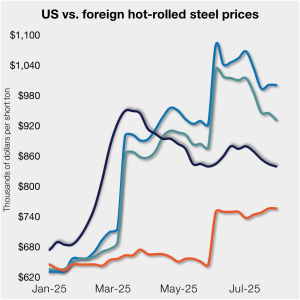

Domestic hot-rolled (HR) coil prices were flat this week, while offshore prices varied week over week (w/w). The price margin between stateside and foreign product was little changed as a result.

Steel prices, end-use demand, inventory levels, tariffs, imports, and evolving market events... what is the steel industry talking about this week?

Steel prices remained largely unchanged this week, staying at or near lows last seen in February. All five sheet and plate products tracked by SMU moved by no more than $5 per short ton (st) from the previous week.

Carbon steel plate market participants suspect that this week’s modestly softer prices are the result of quietly negotiated prices between plate purchasers and mills.

With SMU Steel Summit starting in just a few days, I decided to go back and do a quick check on where things stand now compared to the week before Summit last year.

The majority of steel buyers responding to our market survey this week continue to say that mills are negotiable on new spot order prices. Negotiation rates have remained high since May.

Sheet and plate prices were flat or lower again this week on continued concerns about demand and higher production rates among US mills.

Nucor has lowered its hot-rolled (HR) spot price by another $10 per short ton (st) this week.

On Monday and Tuesday of this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices ticked higher again week over week (w/w).

All five of SMU's steel sheet and plate price indices declined this week, falling to lows last seen in February.

Sources in the carbon and alloy steel plate market said they are less discouraged by market uncertainty resulting from tariffs or foreign relations, but are instead, eager to see disruption to the flat pricing environment.

Nucor has implemented a double-digit price decrease on spot hot-rolled (HR) coil for the second consecutive week.

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices increased week over week (w/w).

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through July 31.

Most steel buyers continue to report that mills are open to negotiating spot prices. Negotiation rates have remained high for most of the past three months.

Sheet and plate prices were either flat or modestly lower this week on softer demand and increasing domestic capacity.

Nucor Plate Group has informed customers that August spot prices will remain flat.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil was adjusted $10 per short ton (st) lower this week after holding steady last week.

Prices for four of the seven steelmaking raw materials we track were unchanged from late June through the end of July, while two increased and one declined. Collectively, these material prices rose 1% month over month (m/m), but are down 3% compared to three months ago.

Hot-rolled (HR) coil prices in the US edged lower again this week, while offshore price were little changed. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Sheet prices slipped again this week amid discounting from certain mills and ongoing concerns about demand.

Nucor maintained its weekly list price for hot-rolled (HR) coil flat this week, following a price cut the previous week.

More than nine out of every ten steel buyers polled by SMU this week reported that mills are negotiable on new order prices. Negotiation rates have increased in each of our last three surveys following the early-June lull, reaching a record high this week.

Galvanized steel prices ping-ponged in the $50/hundredweight range during the month of July, settling in at roughly the same position as in June.

Nucor is lowering its list price for spot hot-rolled coil for the first time since May 27.

Section 232 tariffs have doubled to 50%. Reciprocal tariffs rates remain uncertain. But while prices have softened on even softer sentiment, tariffs have firmed the floor.