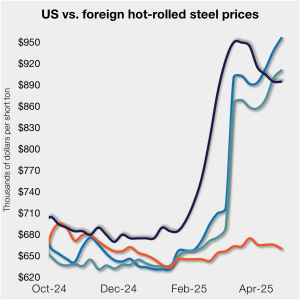

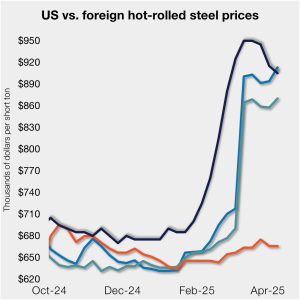

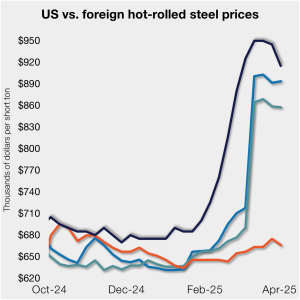

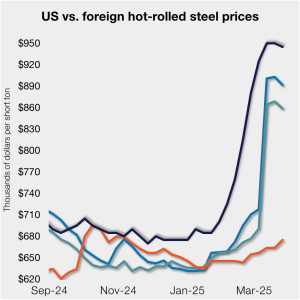

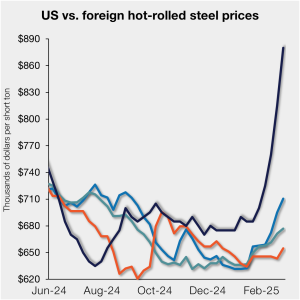

S232 lifts EU HR price over US, Asian HR still well behind

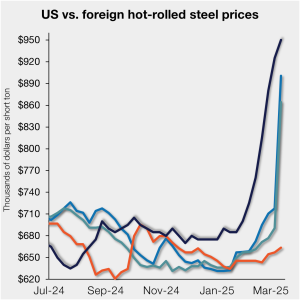

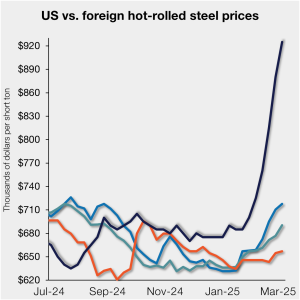

Domestic hot-rolled coil prices were flat this week after dropping for four straight weeks. Most offshore markets bucked the trend and gained ground.

Domestic hot-rolled coil prices were flat this week after dropping for four straight weeks. Most offshore markets bucked the trend and gained ground.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

US domestic sheet price gains have begun to slow as previously pulled-forward demand has led to a decline in orders.

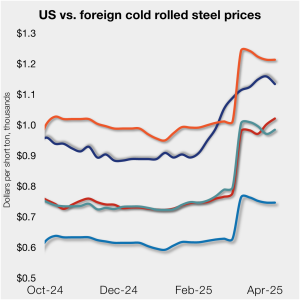

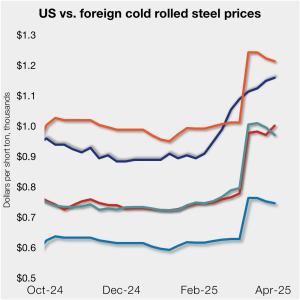

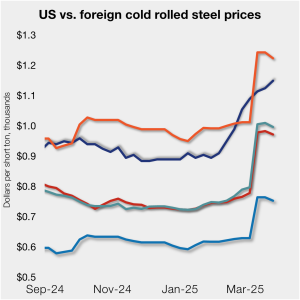

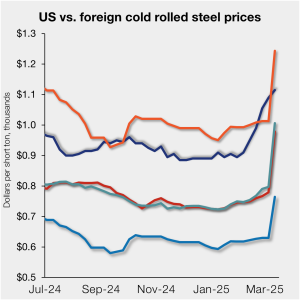

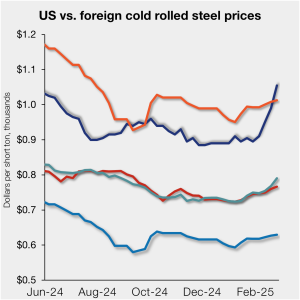

US cold-rolled (CR) coil prices declined this week, slipping for the first time since early February. Most offshore markets deviated, moving higher this week.

The amount of finished steel that entered the US market in February receded from January’s peak, according to our analysis of Department of Commerce and American Iron and Steel Institute (AISI) data.

Domestic hot-rolled (HR) coil prices declined this week for a third straight week. Most offshore markets bucked the trend and gained ground. Uncertainty in the US market around tariffs, especially after “Liberation Day,” caused US prices to slip as buyers moved to the sidelines. It’s unclear to date whether the 90-day pause on the more […]

US steel imports returned to normal levels in February after climbing to a near three-year high in January, according to finalized trade data published by the US Commerce Department. March license data suggests imports have remained within this normal range.

Tariffs are taxes that the government collects. Funds are disbursed by acts of Congress. If domestic companies, including manufacturers, are to benefit from “protective” tariffs, they must raise their prices as well. Maybe not by the entire amount of the tariffs, but by some. Inflation will come.

US cold-rolled (CR) coil prices moved higher again this week, while offshore prices were mixed.

The US Commerce Department on Friday released preliminary anti-dumping margins in a trade case targeted imports of coated flat-rolled steel from 10 countries. Certain countries and mills were hammered while others were largely spared. Brazilian steelmaker CSN, for example, received a preliminary rate of 137.76%. Some Turkish mills – including Boreclik and ArcelorMittal Celik Ticaret – received no dumping margin at all.

The Commerce Department has made a preliminary determination that ‘critical circumstances’ exist for certain imports of corrosion-resistant (CORE) flat-rolled steel from the United Arab Emirates (UAE). Commerce decided that critical circumstances did not apply to CORE from South Africa. The department also found that critical circumstances did not apply to CORE from UAE producers Al-Ghurair Iron & Steel LLC and United Iron & Steel Company LLC.

Domestic hot-rolled (HR) coil prices declined this week, a trend again reflected in most offshore markets. Despite similarities, the shifting tariff landscape has made for a wild ride in Q1.

The United Arab Emirates’ Emirates (UAE) Emirates Global Aluminum (EGA) announced plans to spend $1.4 trillion dollars in the US over the next 10 years, including a greenfield primary aluminum smelter. Is this real or another soundbite?

US cold-rolled (CR) coil prices increased again this week, while offshore prices declined.

Upon the request of US chassis manufacturers, the Commerce Department this week initiated investigations into the alleged dumping and subsidization of chassis imported from Mexico, Thailand, and Vietnam.

The threat of tariffs over the past two months has been a springboard for US prices. But the Section 232 reinstatement on March 13 narrowed the domestic premium over imports on a landed basis.

US cold-rolled (CR) coil prices moved higher this week, a trend not evenly shared by offshore prices.

Domestic hot-rolled (HR) coil prices were flat this week, a trend mirrored in offshore markets.

Fully restored Section 232 tariffs on steel on March 12 cut the widening premium US prices had over most imports on a landed basis.

President Trump’s tariffs are aimed in large part at bringing manufacturing back to the United States. In theory, it’s simple enough: Want to avoid a big tariff? Make it in the US!

Domestic hot-rolled (HR) coil prices moved higher this week, still largely outpacing increases seen in offshore markets. But the reinstatement of undiluted Section 232 tariffs on steel on March 12 cut the ballooning premium stateside prices had gained on most imports on a landed basis. The premium stateside tags had over prices abroad stood at […]

The volume of finished steel entering the US market in January climbed to the highest level recorded in two and a half years.

US cold-rolled (CR) coil prices continued to rise this week, well ahead of offshore prices. The price spread between stateside-produced CR and imports reached a 14-month high in the week ended March 7. Steady price gains in overseas markets continue to be overshadowed by increases in domestic prices. The result? The US premium over imports […]

Steel imports ended 2024 on a low note, with November trade falling to a one-year low and December seeing a modest 3% recovery. Then as the new year began, import volumes spiked.

Wonder what the fallout from all the Trump tariffs might be? A manufacturing renaissance? A post-WWII order in ashes? Or something a little more down the middle? Then register for our next Community Chat on Thursday, March 13 at 11 am ET. Yes, you read that correctly, SMU is shattering precedent by holding a Community Chat on a day that is not Wednesday. Our featured speaker will be Alan Price, a leading trade attorney at Wiley and someone whose columns you read regularly in SMU.

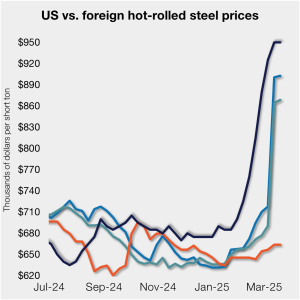

Domestic hot-rolled (HR) coil prices moved higher this week, widely outpacing increases seen in offshore markets.

The demise of the VAT rebate system in China might be the most tangible sign that Beijing realizes that its unbridled access to global markets is over. There was no point in continuing a system of financial incentives to the export sector when the tariff headwinds were getting stronger.

The price spread between stateside-produced CR and imports reached its widest margin in over a year.

That’s not to say Section 232 shouldn’t be tightened up. Or that certain trade practices – even among our traditional allies – weren’t problematic. But when it comes to the reboot of Section 232, I do wonder whether there will be some unintended consequences.

Hot-rolled (HR) coil prices continued to rally in the US this week, quickly outpacing price gains seen abroad. The result: US hot band prices have grown widely more expensive than imports on a landed basis. The premium US HR tags carry over HR prices abroad now stands at a 14-month high. SMU’s average domestic HR […]