ITC votes not to impose duties on tin mill product imports

At the final hour, the trade case investigating unfairly traded imports of tin mill products has been terminated.

At the final hour, the trade case investigating unfairly traded imports of tin mill products has been terminated.

Former President Donald Trump discussed, if re-elected, placing a 60%-or-more tariff on all Chinese imports in an interview with Fox News on Sunday.

I participated in the 35th annual Tampa Steel Conference last week, a conclave of steel producers, consumers, traders, logisticians, and (a few) trade lawyers. I participated in a panel discussion concerning challenges in managing supply chains in these troubled times. Things appear to be heading in the wrong direction in this field. Supply chains were shown to be vulnerable to pandemics in 2020 and 2021, and, in 2022 and 2023, to regional conflicts and weather slowing or stopping the free movement of goods through trade bottlenecks (the Suez Canal, the Panama Canal, the Bosporus, etc.)

Timna Tanners, managing director of equity research at Wolfe Research, will be the featured speaker on our next SMU Community Chat on Feb. 7.

The Department of Commerce has adjusted the countervailing duty (CVD) rates on imports of corrosion-resistant (galvanized/Galvalume) steel from South Korea after an administrative review.

Speaking during a fireside chat at the Tampa Steel Conference on Monday, Jan. 29, Hybar CEO David Stickler provided a status update on the company’s new rebar mill project and its plans for the future, including the possibility of a flat-rolled steel mill.

The US Midwest premium was flat week over week (w/w) at 18.8–19.4¢/lb. Again, the premium has exhibited remarkably low levels of volatility and has yet to react to news in the geopolitical or macroeconomic spaces.

I thought Nippon Steel’s $14.1-billion deal for U.S. Steel might become a political football in this year’s presidential election. Now there is little doubt that it will after Trump told reporters in Washington, D.C., earlier this week that he would “absolutely” block the transaction – and that he would do so “instantaneously.”

Steel mill lead times for sheet products saw substantial declines over the past two weeks, while production times for plate held steady during the month of January.

If reelected in the November presidential election, Donald Trump said he would block the sale of U.S. Steel to Japan’s Nippon Steel Corp. (NSC).

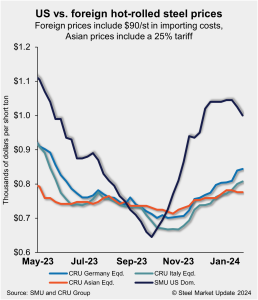

US hot-rolled coil (HRC) prices law little movement this week, a similar trend seen in offshore markets. Thus, the price premium domestic hot band carries over imported products was largely unchanged vs. the prior week.

I’m writing these final thoughts from the JW Marriott in Tampa. And I’m looking forward to seeing some of you reading this in just a few hours at the opening networking reception of the Tampa Steel Conference. Nearly 550 people will be there – a new record for the event. If you’re looking for things […]

Trade is not the major focus of the campaigns for the 2024 elections, either at the presidential or congressional level. But it is there as a live issue for business. And last August, former President Trump suggested a 10% tariff on virtually all imports as a “ring around the collar” of the US economy.

The Steel Manufacturers Association (SMA) outlined its praise for the US and EU extension on negotiations towards the proposed Global Arrangement on Sustainable Steel and Aluminum.

This week Magnitude 7 Metals issued a statement to announce the curtailment of its New Madrid smelter in Marston, Mo. The plant, one of only five remaining primary smelters in the US, employs approximately 450 union workers. With over 275,000 metric tons (mt) of capacity per year, New Madrid is the second-largest plant by capacity […]

December’s import level was slightly lower than an earlier license count had suggested, resulting in December marking the second-slowest month for imports in 2023.

Brazilian steel maker Usiminas has resumed operations at blast furnace (BF) No. 3 at its Ipatinga works in the state of Minas Gerais. The restart comes after a BRL2.7-billion ($546-million) refurbishment on the unit, which has capacity of three million metric tons (mt) per year.

The American steel market, including the stainless steel market, continues to face serious threats from subsidized and dumped imports resulting from foreign government policies creating an unfair playing field. It is no secret that China is a major culprit.

The Tampa Steel Conference is just a few days away. Here are some topics I’m looking forward to learning more about during the proceedings on Monday and Tuesday. For starters, we’ll have about a month of 2024 under our belt when we convene on Sunday. How does that compare to what we thought the start of the year would look like? And what’s the outlook for the balance of the year?

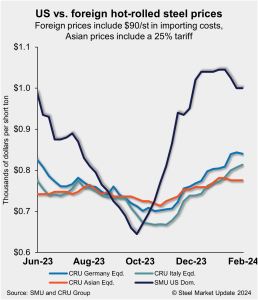

US hot-rolled coil (HRC) prices declined further this week, easing to their lowest level since late November. And while domestic tags remain notably more expensive than offshore product, the premium has declined as imported hot band tags have moved higher.

What's being talked about in the US steel market this week?

Steel Dynamics Inc.’s (SDI’s) top executive sees hot band demand remaining strong in 2024, which should support pricing.

SMU’s Jan. 24 Community Chat, featuring CRU's Principal Analyst Erik Hedborg, provided viewers with an update on the current state of the global iron ore market.

US hot-rolled coil (HRC) prices edged down this week while import prices moved higher on average. Domestic hot bands’ premium over cheaper imports declined as a result. But overall, US product remains substantially more expensive than overseas material. All told, US HRC prices are 21.4% more expensive than imports, a premium that is down three […]

What are people in the steel marketplace talking about this week?

There seems to be a growing consensus that the US sheet market has peaked at a high level and could begin losing ground from here. Whether declines happen quickly or whether sheet prices bop around at current levels for a few weeks more is the primary question.

Coming out of a strong fourth quarter, galvanized steel market participants are reporting an above-average start to January and are cautiously optimistic for 2024.

US service center flat-rolled steel inventories surged in December with the seasonal slowdown in shipments. At the end of December, service centers carried 64.8 shipping days of supply, according to adjusted SMU data, up from 54 days in November.

Turkish scrap import prices increased last week with CRU’s assessment for HMS1/2 80:20 at $423 per metric ton (t) CFR, up by $7/t week over week (w/w) but down $2/t month over month (m/m). This was driven by a pickup in buying activity.

It’s been a sloppy start to the year for domestic hot-rolled (HR) coil and ferrous scrap markets. One of the loudest things to happen in HR this year might be something that didn’t happen at all. Namely, Nucor didn’t follow competitor Cleveland-Cliffs higher when Cliffs announced a price hike to start the year.