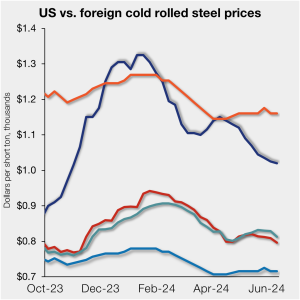

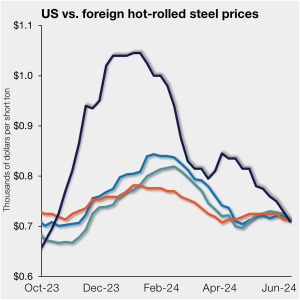

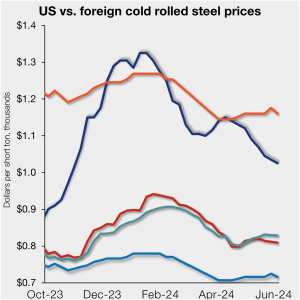

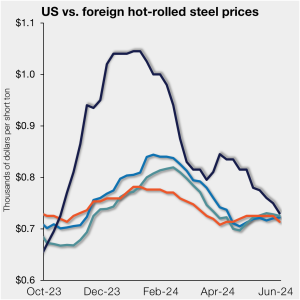

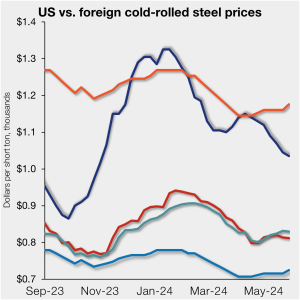

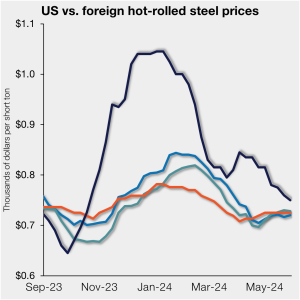

Final thoughts

The conventional wisdom is that sheet prices will trend down for the next few weeks (maybe the next two months) before rising again in August – around when lead times stretch into the busier fall months. We see that reflected in our survey results and in market chatter. And there are plenty of data points to choose from if you want to support of that position.