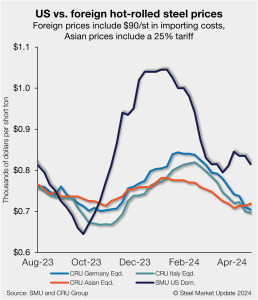

SMU price ranges: Sheet down broadly, HR $35/t lower

Sheet prices fell across the board this week – largely in response to Nucor’s $65-per-short-ton price cut for hot-rolled (HR) coil on Monday morning. SMU’s HR coil price is $780/st on average, a $35/st decrease week over week (w/w). Our average cold-rolled coil price is $1,090/st (down $30/st w/w). Our galvanized base price is $1,100/st […]