Nucor warns of weaker Q2 earnings on lower prices, volumes

Nucor Corp. has guided to much lower second-quarter earnings, as profitability in its steel mills segment suffers due to lower prices and volumes.

Nucor Corp. has guided to much lower second-quarter earnings, as profitability in its steel mills segment suffers due to lower prices and volumes.

The spread between hot-rolled coil (HRC) and prime scrap prices has narrowed for the second consecutive month, according to SMU’s most recent pricing data.

US sheet prices continued to tick down this week as supply seems to outweigh demand, and deep discounts are not only for large-ton buys.

Movements in steel mill lead times were mixed this week, according to our latest steel buyers survey results. Service centers and manufacturers reported short to average production times, little changed from our last report.

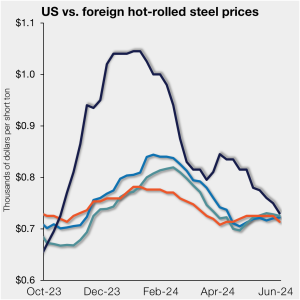

US hot-rolled (HR) coil prices ticked down again this past week, nearly reaching parity with offshore hot band prices on a landed basis. This week, domestic HR coil tags were $730 per short ton (st) on average based on SMU’s latest check of the market on Tuesday, June 4. Domestic HR coil prices are now […]

Steel buyers found mills more willing to negotiate spot pricing this week on all products SMU tracks with the exception of Galvalume, according to our most recent survey data.

ArcelorMittal plans to continue to invest and expand its operations in North America, a senior company executive said in an exclusive interview with SMU. “People were talking about our demise in North America or maybe our exit. And I want to emphasize that nothing could be further from the truth,” said Brad Davey, executive vice president and head of corporate development at the company.

US sheet prices remained on a downward course again this week amid chatter in some corners about a potential broader slowdown in demand. SMU’s hot-rolled (HR) coil price now stands at $730 per short ton (st) on average, down $20/st from last week and down $115/st from a recent high of $845/st in early April. […]

Hot-rolled coil prices are known for their volatility. There are a variety of hedging strategies industry players have used to manage it, one of them being the use of HRC futures. However, some have been hesitant to dip in their toe, and their money, in futures and have preferred other approaches.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

Sheet prices slipped again this week on a combination of moderate demand, increased imports, and higher import volumes.

Prices for galvanized products have fallen from last month, and many market participants expect tags to continue their descent or at best remain flat in the month ahead.

Cleveland-Cliffs is potentially eyeing a buy of NLMK USA’s Midwest assets, according to a report in Bloomberg.

Nucor moved its published consumer spot price (CSP) up again this week.

The Biden administration recently announced tariffs on several products from China, including steel and aluminum. There has been much rejoicing over this move and there has been a great deal of support from the steel industry.

Nucor’s Consumer Spot Price (CSP), a legitimate mill offer price, is a potential disruptor to North American steel sheet commercial and procurement strategies. We will dive into the details of what we think the CSP is and why we believe it is a potential disruption to how the North American sheet market operates.

Hot rolled buyers found mills less willing to negotiate spot pricing this week, while other products SMU tracks were mixed, according to our most recent survey data.

Cleveland-Cliffs is seeking at least $800 per short ton (st) for hot-rolled (HR) coil with the opening of its July order book. The Cleveland-based steelmaker said the move was effective immediately in a letter to customers on Thursday, May 23. Recall that Cliffs announced in April that it would publish a monthly HR price. The […]

Steel prices eased for both sheet and plate products this week, according to our latest canvass of the market

Nucor upped its published consumer spot price (CSP) this week.

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed this month, according to SMU’s most recent pricing data.

Earlier this month, steelmakers entered the scrap market at mixed pricing. The prevailing price for obsolescent grades fell $20 per gross ton (gt). However, some notable districts decided to only drop $10/gt.

The last time we were together on April 18, the June hot-rolled coil (HRC) future was sitting around the $800 support level where the May future found a bottom in mid-February.

Domestic scrap prices this month are flat for prime material, but down for HMS and shredded, scrap sources told SMU.

Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact info@steelmarketupdate.com. Flat Rolled = 57.8 shipping days of supply Plate = 58.3 shipping days of supply Flat Rolled US service center flat-rolled steel supply edged lower in April, though shipments continue to […]

Steel prices were overall mixed this week, according to our latest check on the market. Sheet prices were flat to down, while plate prices inched up. SMU indices on hot rolled, cold rolled, and galvanized are now down to the lowest levels seen since November.

Steel Market Update’s Steel Demand Index fell eight points, and back into contraction territory, an indication demand might be slipping as prices have trended lower, according to our latest survey data.

CRU Senior Analyst Ryan McKinley will be the featured speaker on the next SMU Community Chat on Wednesday, May 15, at 11 am ET. You can register here. Note that the live webinar is free for all to attend. A recording will be available only to SMU members.

Hot rolled, cold rolled, and plate buyers said mills are more willing to talk price on spot orders this week, while the overall negotiation rate for products SMU surveys remained level, according to our most recent survey data.

Most steel products tracked by SMU saw lead times contract this week from two weeks earlier, according to SMU’s most recent survey data.