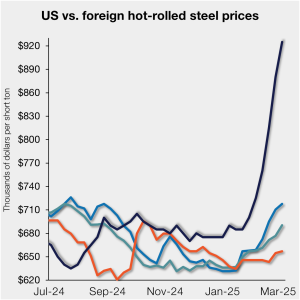

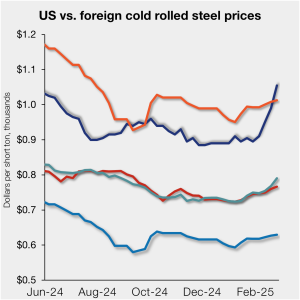

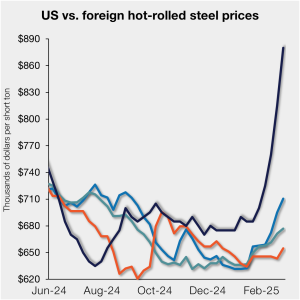

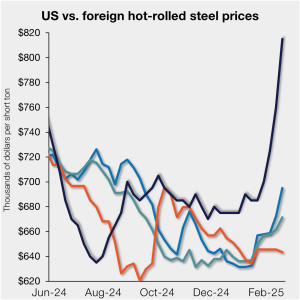

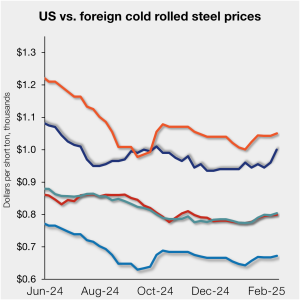

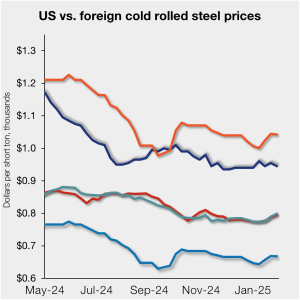

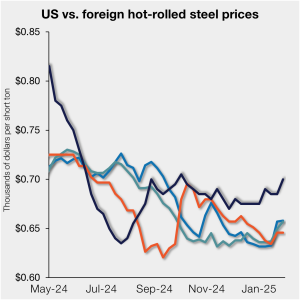

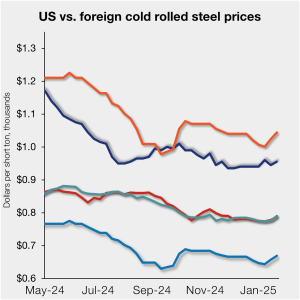

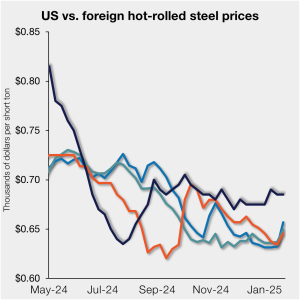

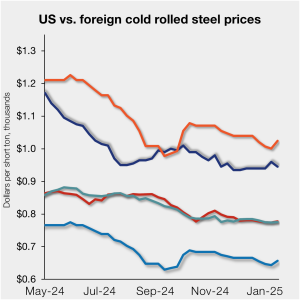

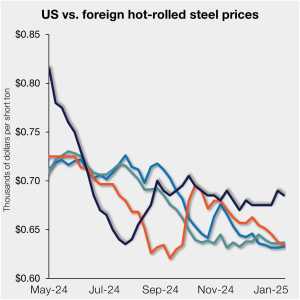

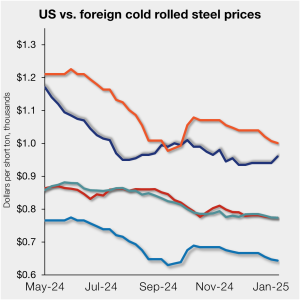

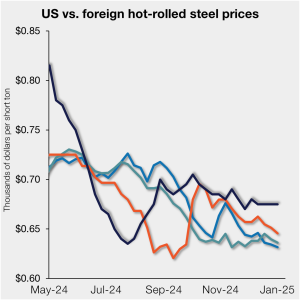

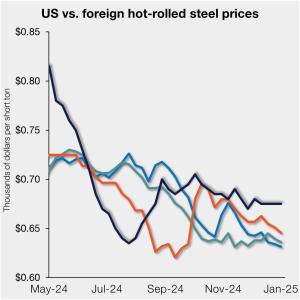

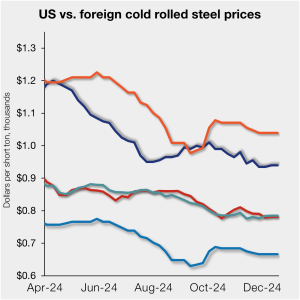

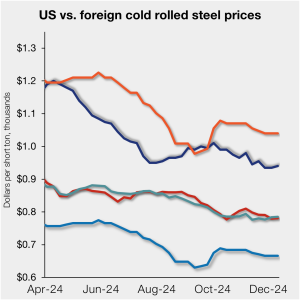

Domestic CRC price gains still outpacing imports

US cold-rolled (CR) coil prices continued to rise this week, well ahead of offshore prices. The price spread between stateside-produced CR and imports reached a 14-month high in the week ended March 7. Steady price gains in overseas markets continue to be overshadowed by increases in domestic prices. The result? The US premium over imports […]