SMU survey: Lead times remain short, nearing 9-month lows

Steel mill lead times remain near some of the lowest levels witnessed in months, according to our latest market canvass to steel service centers and manufacturers.

Steel mill lead times remain near some of the lowest levels witnessed in months, according to our latest market canvass to steel service centers and manufacturers.

US sheet prices moved lower again this week, continuing a trend seen since early April. The slowdown aligns with the typical summer doldrums, when lax demand and shorter lead times often take center stage. The current market is also characterized by ample supply and concerns about restocking – especially with few signs of a bottom […]

Low global sheet demand continued to weigh on prices around the world this week. In the US, mills were forced to remain aggressive to secure orders during this period of demand weakness. And compounded by recent new capacity ramp-ups, has forced US hot rolled (HR) coil prices down closer to levels seen in offshore markets. […]

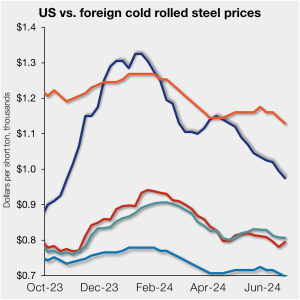

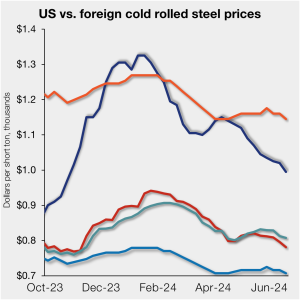

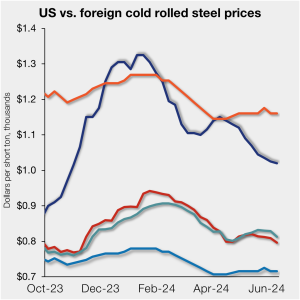

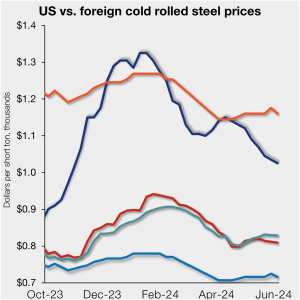

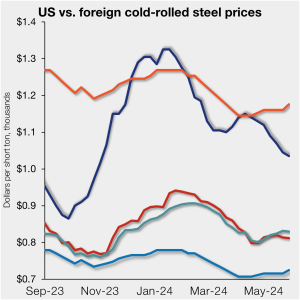

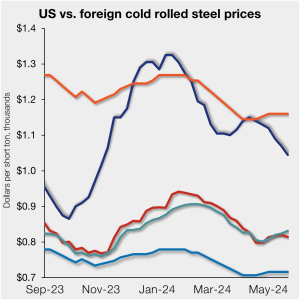

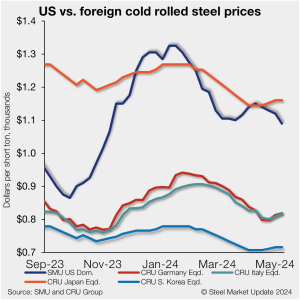

Offshore cold-rolled (CR) coil remains cheaper than domestic product pricing even as US CR coil prices slip to an eight-month low. Domestic CR coil tags stood at $975 per short ton (st) on average in our check of the market on Tuesday, June 25, down $20/st from the week before. Domestic CR prices are, on […]

Following a relatively stable first quarter, steel imports climbed in May to levels not seen in over two-years, according to preliminary Census data released earlier this week. Projected June license data suggests imports could ease from May, though still strong in comparison to levels witnessed over the past year.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

US sheet prices continued to drift lower this week on lackluster demand, short lead times, and ample supply. SMU’s hot-rolled (HR) coil price now stands at $670 per short ton (st) on average, down $15/st from last week. Hot band is down $175/st from a recent high of $845/st in early April. It is also […]

Offshore cold-rolled (CR) coil prices are cheaper than domestic product despite US CR coil prices ticking lower. Domestic CR coil tags stand at $995 per short ton (st) on average, down $25/st vs. our prior check of the market on Tuesday, June 18. (We will update prices again on Tuesday, June 25.) All told, US […]

Steel mill lead times remain short for all steel products tracked by SMU, according to our latest market survey. Service center and manufacturers continue to report short to normal lead times for sheet and plate products.

Steel buyers of hot-rolled, cold-rolled, and galvanized products found mills more willing to negotiate spot pricing this week, according to our most recent survey data. However, buyers of Galvalume and plate products said mills were less willing to talk price.

US sheet prices edged lower this week as discounting continues. Major factors remain ample supply, shorter lead times, and lower input costs. Meanwhile, demand had remained steady to soft, depending on the end market. SMU’s hot-rolled (HR) coil price now stands at $685 per short ton (st) on average, down $25/st from last week. Hot […]

Offshore cold-rolled (CR) coil prices have changed little, but they are still notably cheaper than domestic product. That remains the case even as US CR coil prices ticked lower this week.

US sheet prices continued to tick down this week as supply seems to outweigh demand, and deep discounts are not only for large-ton buys.

Total steel exports rebounded 6% in April, rising to 842,000 short tons (st) according to the latest US Department of Commerce data.

Now that June has arrived, the official countdown until SMU’s Steel Summit 2024 – North America’s premier flat-rolled steel conference – has begun. If you haven’t already registered, don’t delay. More than 700 attendees from more than 300 companies have already registered to be in Atlanta this August. In short, it’s poised to be another […]

Offshore cold-rolled (CR) coil prices remain notably cheaper than domestic product. That remains the case even as US CR coil prices continue to tick lower.

It feels like the summer doldrums arrived a little earlier than usual this year. I know there had been rumors of a price hike. The prospect of a sharply lower June scrap trade probably didn't help the chances of that actually happening.

US sheet prices remained on a downward course again this week amid chatter in some corners about a potential broader slowdown in demand. SMU’s hot-rolled (HR) coil price now stands at $730 per short ton (st) on average, down $20/st from last week and down $115/st from a recent high of $845/st in early April. […]

We’re just a few months away from SMU’s Steel Summit 2024 – North America’s premier flat-rolled steel conference.

Offshore cold-rolled (CR) coil prices remain significantly cheaper than domestic product. That remains the cause even as US CR coil prices continued to tick lower. All told, US CR prices are now 17.6% more expensive than imports. While still high, that premium is down from 19.4% last week and down from 31.5% in early January.

Sheet prices slipped again this week on a combination of moderate demand, increased imports, and higher import volumes.

Offshore cold-rolled (CR) coil prices remain a cheaper option over domestic product, even as US CR coil prices tick lower, according to SMU’s latest check of the market.

Hot rolled buyers found mills less willing to negotiate spot pricing this week, while other products SMU tracks were mixed, according to our most recent survey data.

Lead times on most steel products tracked by SMU held steady or contracted this week compared to two weeks earlier, according to our latest market survey.

Steel prices eased for both sheet and plate products this week, according to our latest canvass of the market

Steel prices were overall mixed this week, according to our latest check on the market. Sheet prices were flat to down, while plate prices inched up. SMU indices on hot rolled, cold rolled, and galvanized are now down to the lowest levels seen since November.

Offshore cold-rolled (CR) coil prices remain much less expensive than domestic product, even as domestic prices have slipped to a six-month low, according to SMU’s latest check of the market.

Hot rolled, cold rolled, and plate buyers said mills are more willing to talk price on spot orders this week, while the overall negotiation rate for products SMU surveys remained level, according to our most recent survey data.

Most steel products tracked by SMU saw lead times contract this week from two weeks earlier, according to SMU’s most recent survey data.

Sheet prices fell across the board this week – largely in response to Nucor’s $65-per-short-ton price cut for hot-rolled (HR) coil on Monday morning. SMU’s HR coil price is $780/st on average, a $35/st decrease week over week (w/w). Our average cold-rolled coil price is $1,090/st (down $30/st w/w). Our galvanized base price is $1,100/st […]