HR vs CR price gap continues to increase

The dollar premium cold-rolled coil (CRC) carries over hot-rolled coil (HRC) continues to expand according to our latest scope of the market.

The dollar premium cold-rolled coil (CRC) carries over hot-rolled coil (HRC) continues to expand according to our latest scope of the market.

Sheet prices reversed course and moved higher this week, while plate priced remained flat, according to our latest canvas of the market.

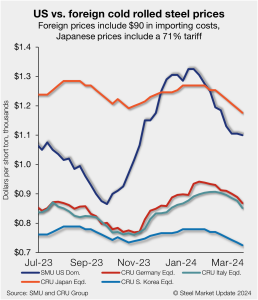

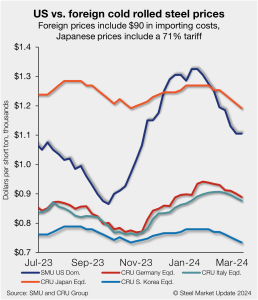

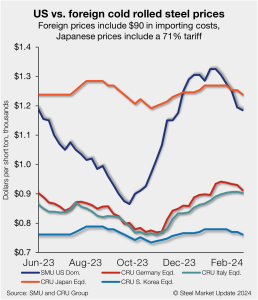

Foreign cold-rolled (CR) coil remains notably less expensive than domestic product even with repeated tag declines across all regions, according to SMU’s latest check of the market.

Sheet and plate prices mostly moved lower this week after little change was noted the week prior. Despite edging down, sentiment is mixed, and many suggest a bottom may be near.

Foreign cold-rolled coil (CR) remains significantly less expensive than domestic product even as US tags continue to decline in a hurry, according to SMU’s latest check of the market.

Sheet and plate prices were mostly flat this week – largely in response to the mill price blitz from last week – pausing the downtrend they’d been on for the better part of 2024.

The price premium cold-rolled coil (CRC) carries over hot-rolled coil (HRC) remains wide, according to our latest market check. Based on our steel price indices published Tuesday, the spread between these products is at the fifth-highest weekly level seen over the last 16 months.

Sheet and plate prices this week continued the downward trend they’ve been on for most of 2024. Some market sources predicted that a wave of spring maintenance outages would help to stabilize lead times and prices in the weeks ahead – especially should service center inventories, high at the beginning of the year, come down meaningfully.

US hot-rolled (HR) coil prices have fallen further this week, working their way to $800 per short ton (st) on average – a mark not seen since late October.

Foreign cold-rolled coil (CR) remains much less expensive than domestic product even as prices in the US have declined at a rapid pace over the past month, according to SMU’s latest check of the market.

US hot-rolled (HR) coil prices have fallen below $900 per short ton (st) on average for the first time since early November. SMU’s HR price stands at $875/st on average, down $65/st from a week ago and down $170/st from the beginning of the year.

Mill lead times for flat-rolled steel were mostly stable over the past two weeks. With several mills slow to come out of outages and upgrades, cold rolled and coated lead times have been holding up better than hot rolled.

Algoma Steel has restarted its blast furnace and resumed steelmaking at its mill in Sault Ste. Marie, Ontario.

The pace of sheet price declines accelerated this week as steel buyers said that domestic mills were competing against each other while also coping with higher-than-expected import volumes. “They are getting rid of the fluff. When you can pit 2-3 mills against each other, the fat margins get cut,” one industry source said.

Algoma Steel reported a wider loss in its fiscal third quarter amid lingering impact from the United Auto Workers (UAW) strike and “heavy seasonal maintenance.” Additionally, the Canadian steelmaker said it has completed repairs at it blast furnace and “restored partial coke-making capabilities” after a previously reported incident on Jan. 20.

Sheet prices fell across the board this week as SMU’s hot-rolled (HR) coil price slipped below $1,000 per short ton (st) on average for the first time since November.

Steel mill lead times for sheet products saw substantial declines over the past two weeks, while production times for plate held steady during the month of January.

Steel buyers said mills were much more willing to negotiate spot pricing this week on all products SMU surveys, according to our most recent survey data.

Sheet prices were mixed this week, with hot-rolled (HR) coil unchanged but cold-rolled and coated prices down.

Domestic sheet prices slipped again this week, marking the first week of consecutive declines for hot-rolled (HR) coil since September. SMU’s HR price now stands at $1,000 per short ton (st) on average, down $25/st from last week and down $45/st from the start of the year.

Canadian flat-rolled steelmaker Algoma Steel said its blast furnace could be down for approximately two weeks following an incident at its coke batteries over the weekend. “We expect some impact on shipments, the extent of which will depend on the timeline to resume blast furnace operations,” the Sault Ste. Marie, Ontario-based company said

The slipping lead times for flat-rolled steel were not just due to the holiday slowdown, it seems, as production times for four out of five products contracted again this week.

Domestic buyers of steel sheet said mills were much more willing to negotiate spot pricing this week, according to our most recent survey data.

The spread between cold-rolled coil (CRC) and hot-rolled coil (HRC) prices jumped during the week of Jan. 8 as cold rolled tags continued to rise while hot rolled tags held steady.

Steel mill lead times pulled back across the board this week but are still said to be at healthy levels, according to SMU's market survey this week.

Sheet prices were mixed in SMU’s first assessment of the market in the New Year.

All of the products SMU surveys notched an increase in the percentage of buyers saying mills were willing to negotiate spot pricing, with the exception of cold rolled, according to our most recent survey data.

US hot-rolled coil (HRC) prices were unchanged week over week (WoW) following a string of mostly upward moves dating back to late September.

U.S. Steel has resumed normal production of cold-rolled coil (CRC) at its Irvin Plant, part of the steelmaker’s Mon Valley Works in western Pennsylvania.

Steel is up again this week. Scrap is up by a lot this month: $85 per gross ton for busheling, by our calculations.