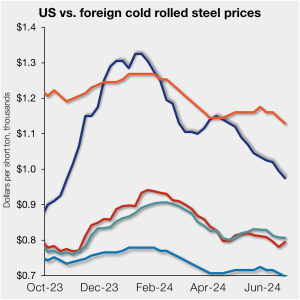

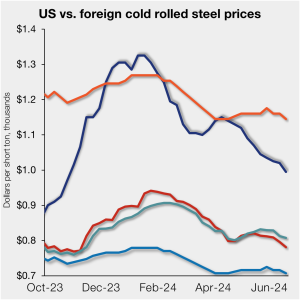

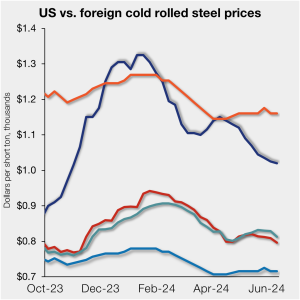

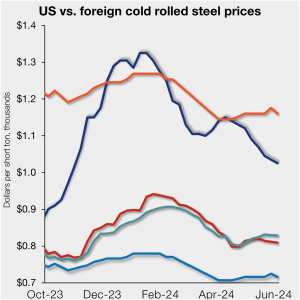

SMU price ranges: Sheet dips lower, more to come?

US sheet prices saw a similar pattern this week, customary for much of the year – new week, lower prices. Domestic tags moved lower this week, aligning with the typically slower summer period – but maybe a further indication of dwindling demand.