US HR prices up slightly vs. imports

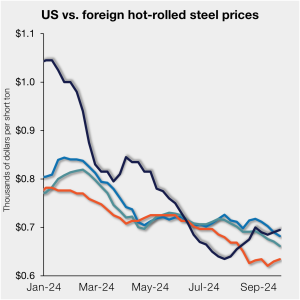

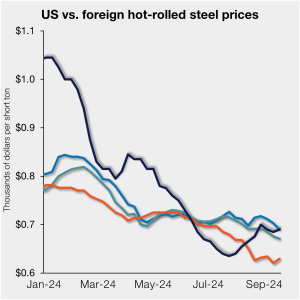

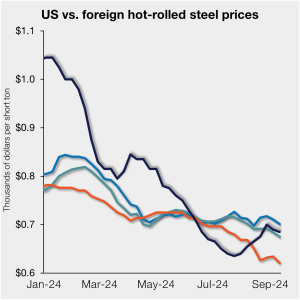

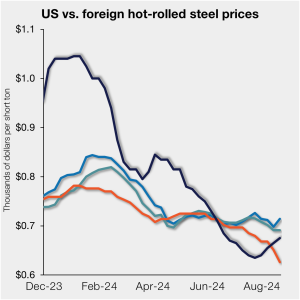

US hot-rolled (HR) coil prices inched up again this past week but remain just a touch more expensive than offshore material on a landed basis.

US hot-rolled (HR) coil prices inched up again this past week but remain just a touch more expensive than offshore material on a landed basis.

The Conference Board reported that consumer confidence in the US dropped to one of the lowest readings of the year in September. With concerns mounting about business conditions and the labor market, the tumble was the biggest monthly decline since August 2021.

SMU’s Key Market Indicators include data on the economy, raw materials, manufacturing, construction, and steel sheet and long products. They offer a snapshot of current sentiment and the near-term expected trajectory of the economy.

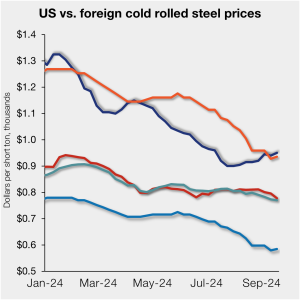

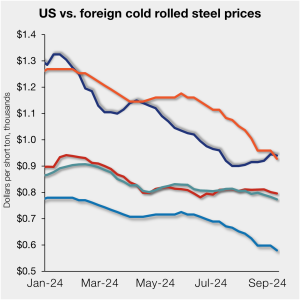

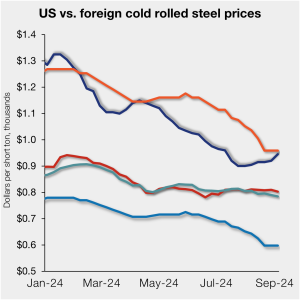

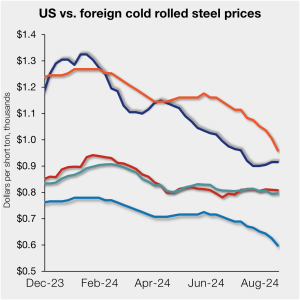

The price gap between US cold-rolled (CR) coil and offshore product widened this week as stateside tags inched up. The premium has been steadily increasing after falling to a 10-month low in late July.

US hot-rolled (HR) coil prices edged up this past week and remain modestly more expensive than offshore material on a landed basis. Since reaching parity with import prices in late August, domestic prices have been slowly pulling ahead of imports. The move has been driven largely by declines overseas.

Triple-S Steel Holdings has acquired West Coast steel products distributor Borrmann Metals Co.

Steel Market Update’s Steel Demand Index ticked back seven points last week, falling further into contraction territory.

Flat rolled = 66.3 shipping days of supply Plate = 57.0 shipping days of supply Flat rolled Flat-rolled steel supply at US service centers grew further in August. The dynamic resulted from some Q3 restocking efforts at a perceived market bottom, met with shorter lead times and weaker demand. At the end of August, service […]

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil is unchanged from last week.

The price gap between US cold-rolled (CR) coil and offshore product is a bit broader this week despite slightly lower tags stateside. The premium is still widening since falling to a 10-month low in late July.

Oil and gas drilling activity in the US recovered the week ended Sept. 13, but remains near multi-year lows.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

The US plate market finds itself in unfamiliar territory, well maybe unfamiliar territory for this side of the post-Covid “normal,” that is.

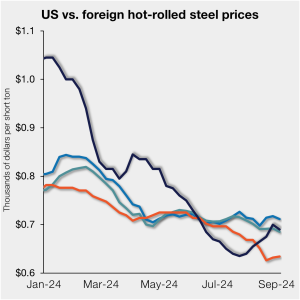

US hot-rolled (HR) coil prices edged down slightly this past week but remain at a slight premium to offshore material on a landed basis.

US light-vehicle (LV) sales improved to an unadjusted 1.42 million units in August, up 7.6% from a year ago, the US Bureau of Economic Analysis (BEA) reported.

Commercial planning momentum continues to drive the Dodge Momentum Index (DMI) higher, pushing August up to a 21-month high.

The price gap between US cold-rolled (CR) coil and offshore product has widened again. The premium has grown repeatedly since falling to a 10-month low in late July.

Construction spending in the US in July was slightly lower than June. Despite the decline, it increased notably year on year (y/y).

US hot-rolled (HR) coil prices were largely flat over the past week, remaining higher than tags for offshore material on a landed basis for a second consecutive week.

Nucor intends to keep plate prices unchanged with the opening of its October order book, according to a letter to customers dated Wednesday, Sept. 4. The Charlotte, N.C.-based steelmaker said it would maintain prices set in its July 1, 2024, price letter.

Growth in the US economy continues to struggle in most districts. The Federal Reserve’s Beige Book report for August shows two-thirds of reporting districts flat or declining economic activity.

US manufacturing activity contracted for a fifth straight month in August, as reported in the latest release from the Institute for Supply Management (ISM). The Index has indicated contraction in the manufacturing sector for 21 of the last 22 months.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil is unchanged from last week.

Steel Market Update will be taking time off in observance of Labor Day. We will not publish an issue on Sunday, Sept. 1, and our offices will be closed on Monday, Sept. 2. Our weekly pricing service will not be impacted. We will resume our regular publication schedule and our pricing service on Tuesday, Sept. […]

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.”

US hot-rolled (HR) coil prices continue to move higher, surpassing tags for offshore material on a landed basis. Domestic prices, improving on the heels of firmer US mill offers, pulled ahead of import tags as the stateside gains this week were sharper than the increases in overseas markets. SMU’s check of the market on Tuesday, […]

Day one and two of SMU's Steel Summit 2024 are officially in the books. We covered a lot of ground, and the agenda sure did deliver.

The price gap between US cold-rolled (CR) coil and imported CR has widened since falling to a 10-month low in late July.

US hot-rolled (HR) coil prices continue to inch up and are now roughly even with prices for offshore material on a landed basis. The closing of the gap between cheaper US prices and more expensive import tags was driven by improving domestic prices on the heels of firmer US mill offers. SMU’s check of the […]

Mill Steel Co., a supplier of flat-rolled steel and aluminum products, has named Scott Hauncher as chief financial officer.