HRC Futures: The role a hedge plays

Last week in Chicago, we hosted several metals companies for our bi-annual Metals Price Management Seminar (“MPMS”).

Last week in Chicago, we hosted several metals companies for our bi-annual Metals Price Management Seminar (“MPMS”).

The spread between hot-rolled coil (HRC) and prime scrap prices widened slightly this month, according to SMU’s most recent pricing data.

Sheet prices increased again this week on the heels of higher costs for scrap, pig iron, and iron ore.

US scrap prices shot up in December and are expected to continue their rise in January, market sources told SMU.

The prices for all grades of pig iron have dramatically risen since SMU’s last report from Nov. 18.

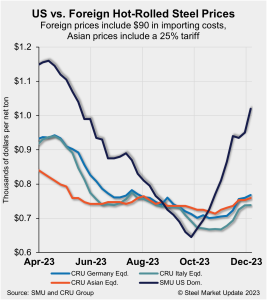

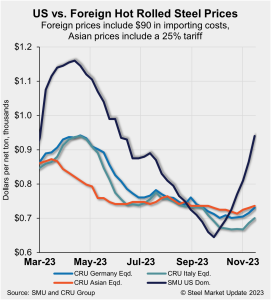

US Hot-rolled coil (HRC) prices keep rising on the heels of continued mill hikes, outpacing increases for offshore product. Domestic tags are now 26% more expensive than imports, the widest pricing gap since January 2022.

A large Detroit-area scrap buyer entered the market on Wednesday at significantly higher prices than a month earlier.

Cleveland-Cliffs is now targeting base prices of $1,100 per ton ($55 per cwt) for hot-rolled coil (HRC).

Sheet prices shot higher again this week on the heels of another round of mill price increases as well as on reports of production and supply chain issues at certain domestic producers.

The export market for ferrous scrap has been strengthening over the last month by a sizable margin.

Oct. 26 was my previous Steel Market Update contribution. The night before, Ford and the United Auto Workers (UAW) announced they had reached a tentative agreement for a new labor contract.

US scrap prices are expected to rise in December, industry sources told SMU.

Sheet prices continued to move higher this week on the heels of mill price hikes and extending lead times.

Nucor aims to increase base prices on all new sheet orders, effective immediately. The Charlotte, N.C.-based steelmaker seeks at least $1,100 per ton ($55 per cwt) for hot-rolled coil (HRC), according to a Monday letter to customers.

Flat-rolled steel prices were in a holding pattern ahead of Thanksgiving.

Prices of steelmaking raw materials are largely up over the over the last 30 days, as they were the month prior, according to Steel Market Update’s latest analysis.

Turkish scrap import prices increased for a third consecutive week.

The spread between hot-rolled coil (HRC) and galvanized sheet base prices has been hovering near $200 per net ton since late July, according to SMU’s latest analysis.

European Aluminium, an association representing the entire European aluminum value chain, announced in a press release that it supports the European Commission's proposed 12th package of sanctions against Russia.

The importation of basic pig iron has allowed EAF steelmakers to implement thin-slab casting technology to make drawing-quality flat-rolled sheet over the last 30 years.

The US plate market has been rather quiet over the past couple of weeks since Nucor Corp. caught many off guard with a $140-per-ton price cut.

SMU discussed wind energy, a promising end-use market for steel, with SSAB Americas’ SVP and CCO Jeff Moskaluk.

The spread between HRC and prime scrap prices widened considerably this month, according to Steel Market Update's most recent pricing data.

In the dynamic landscape of the steel futures market, a confluence of factors is shaping the current narrative.

US Hot-rolled coil (HRC) prices continue to surge on the heels of mill increases. They have become significantly more expensive than prices for hot band imported from offshore. Domestic hot band tags moved higher for a seventh consecutive week. Imports have seen only marginal gains over the same period, according to SMU’s latest foreign vs. domestic price analysis.

Spot prices for steel sheet shot upward again this week on the heels of steep price increases announced by domestic mills last week. SMU’s hot-rolled coil price rose to $940 per ton ($47 per cwt) on average, up $75 per ton from last week and up nearly $300 per ton from a 2023 low of […]

Canadian miner Teck Resources has announced the sale of its metallurgical coal business, Elk Valley Resources, with Swiss miner Glencore becoming the majority stakeholder.

Domestic scrap prices rose in November month over month for all grades that SMU covers, market sources said.

The iron and steel foundry industries consume about 17% of the ferrous scrap in the US each year. They purchase several grades of scrap in common with steelmakers, such as shredded and turnings. But, most of the grades are much more restrictive than what larger mills require.

Several past columns in SMU have included comments about the futures forward curve, using terms like contango and backwardation