Sheet

April 29, 2025

Service centers: Mill orders retreat in March

Written by David Schollaert

Steel Market Update is pleased to share this new, Premium content—an index comparing service centers’ new order entries from steel mills—with Executive members. For information on upgrading to a Premium-level subscription, email info@SteelMarketUpdate.com.

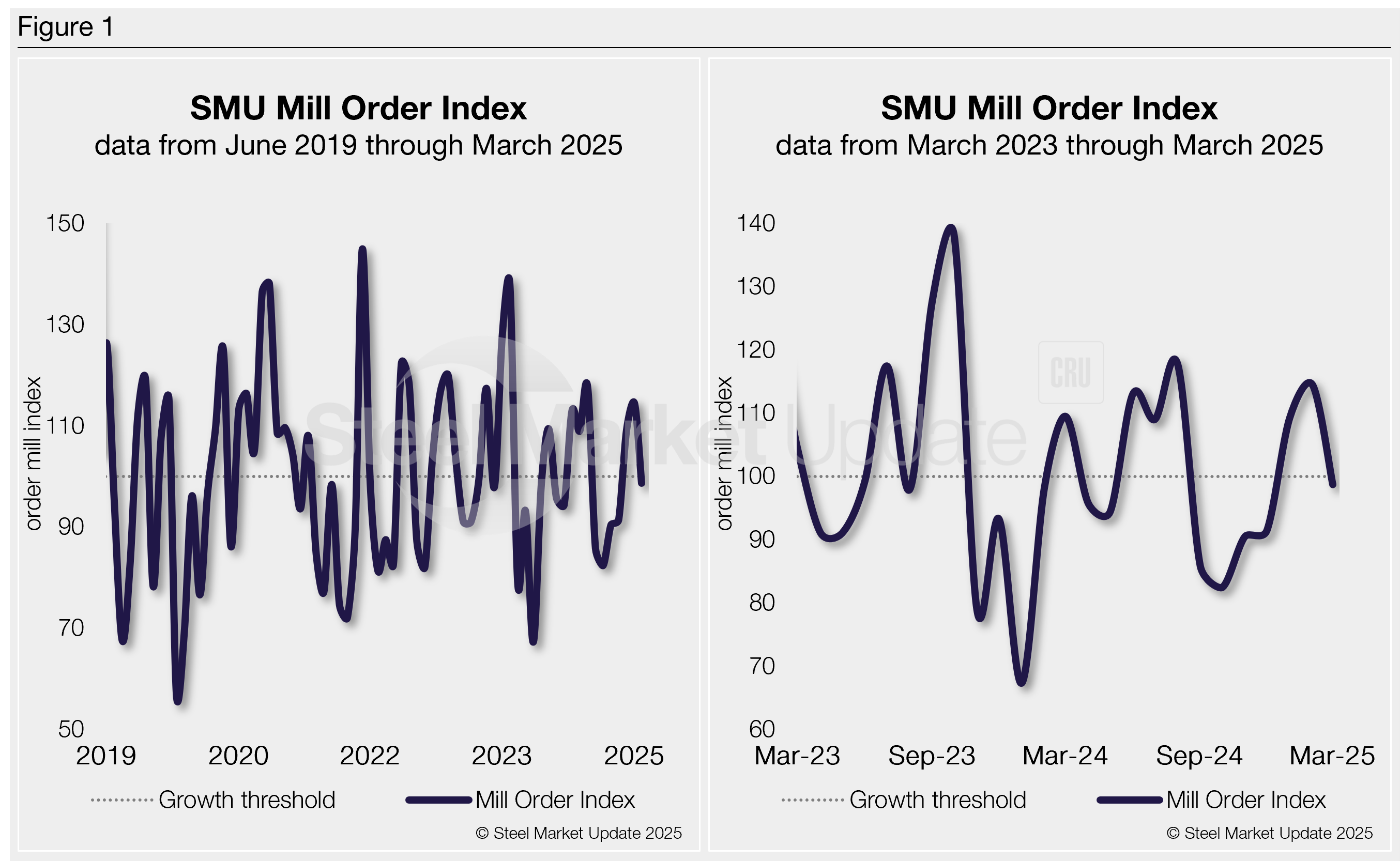

SMU’s Mill Order Index (MOI) declined in March after repeated gains at the start of the year, according to our latest service center inventories data. The slowdown comes after a ramp-up in shipments was met by a slight decline in intake as services centers looked to right-size inventories.

The MOI now stands at 98.7, down from a six-month high of 114.5 in February.

A boost in intake volume was reported in January and February, and early parts of March. This was in response to a boost in demand from downstream customers pulling forward demand ahead of tariff-fueled price increases. The increase in service center orders was met with a rapid rise in mill prices.

Methodology

SMU’s MOI, which evaluates the latest change in service center mill order entries, is a relative index derived from our monthly service center inventories data. This index is a good indicator of current service center buying patterns, displaying perceived demand and lead times. This is notable given that lead times are typically a leading indicator of steel price moves.

The MOI uses a base period, presently 2022-24, to establish a reference point for measuring service centers’ mill orders over time. This base period is assigned an index value of 100. Subsequent MOI values are then calculated relative to this base.

An index score above 100 indicates an increase in buying, and a score below 100 indicates a decrease.

Figure 1 shows the nearly six-year history of the index on the left and provides a closer look at the MOI readings of the past two years on the right (100 = 2022-24 average).

Background

In the second half of last year, demand saw a slow and steady decline, spot buying pulled back, and prices faded.

There were some brighter moments—backed by a few sharp price hikes from mills—but they didn’t last. And buyers were opportunistic. Service centers bought at bottom-dollar levels from June through August (see the right-side chart in Figure 1 above), before pulling back and managing inventories.

The back half of 2024 was underscored by inventory management as large-volume buyers capitalized on discounted steel, but weak end-market demand prevailed.

The Skinny

While demand remains steady and, in some sectors still shows growth, the recent tariff-driven buying surge has passed. Most are now tightening their belt and thus intake and SMU’s MOI should tick lower.

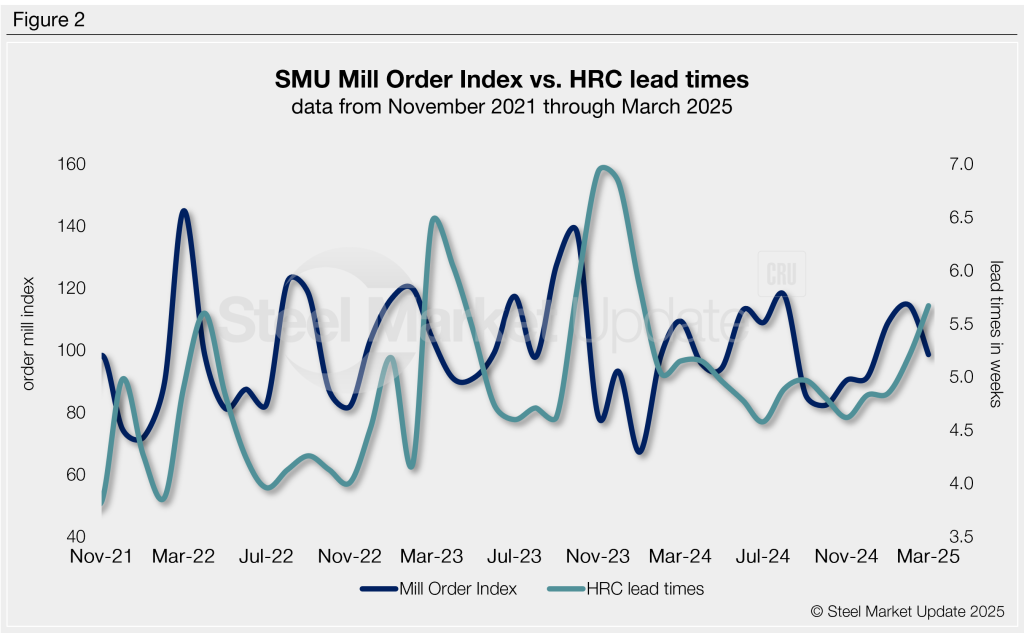

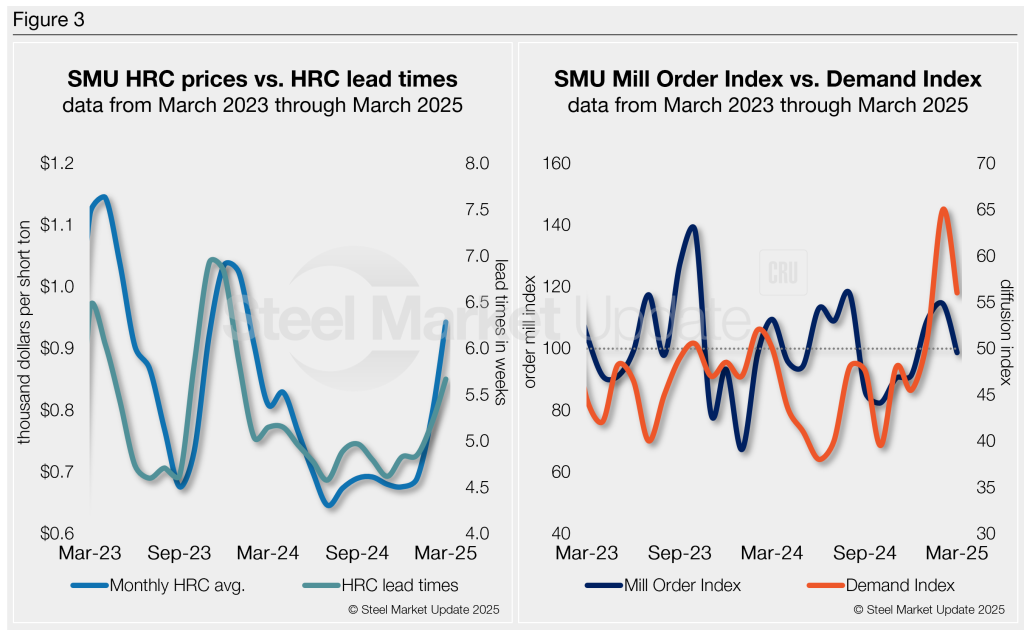

SMU’s MOI pairs well with—and has for the past five years proceeded—moves in mill lead times (Figure 2). And SMU’s lead times have also been a leading indicator of flat-rolled steel prices, particularly for HRC (see left-side chart in Figure 3).

But our MOI also pairs well with our Steel Demand Index (see right-side chart in Figure 3), which for nearly a decade, has preceded moves in mill lead times.

We’ve already started seeing prices edge down—now averaging $885/st, down $10/st week over week (w/w), according to our April 29 check of the market. And lead times were down marginally in our latest assessment two weeks ago. They are presently 5.05 weeks on average, down from 5.55 weeks in early April.

Our next lead time assessment will be published this Thursday, May 1, and the early indication is for them to edge down slightly again.

Recent survey data suggest the market has peaked for the time being, and now it’s a matter of managing the gap that’s been broadened by Q1 buying that pulled forward demand.

Editor’s Note

Order entries, demand, lead times, and prices are based on the average data from manufacturers and steel service centers who participate in SMU’s monthly inventories and every other week market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.