AMU

February 21, 2025

CRU: US smelter restarts more likely due to Trump tariffs but remain limited

Written by CRU Group

President Trump announced earlier this month that he will increase the Section 232 tariffs indiscriminately from 10% to 25% to US imports of all aluminum.

The precise details and duration of the plan remain uncertain, but assuming the tariff on imported aluminum is enacted, CRU believes it will lead to a sustained step change in the Midwest premium. This will impact the economics of potential restarts in the US and may have implications for future expansion.

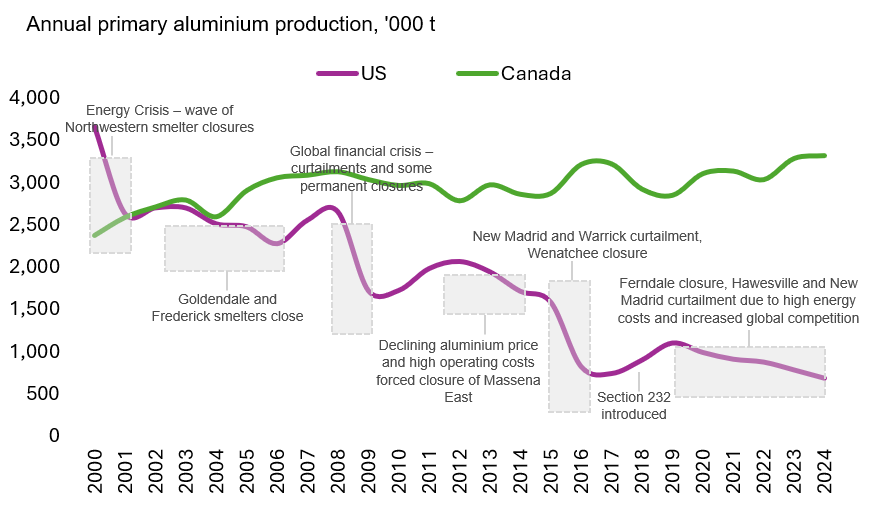

US primary output is at its lowest level this century

CRU estimates that US primary aluminum output was 688 kt in 2024 – the lowest this century – down over 80% on 2000 production levels. Four smelters remained in operation by the end of 2024, namely Warrick, Mt Holly, Massena West and Sebree. At the start of this millennium, 23 primary aluminum smelters were operating in the US, primarily focused in the West and Midwest.

Closures have occurred over this period for several reasons, including energy costs, maintenance costs linked to aging infrastructure, environmental infrastructure and environmental regulation. The latest curtailment occurred at Magnitude 7’s New Madrid smelter in early Q1 2024, primarily due to high energy costs.

DATA: CRU

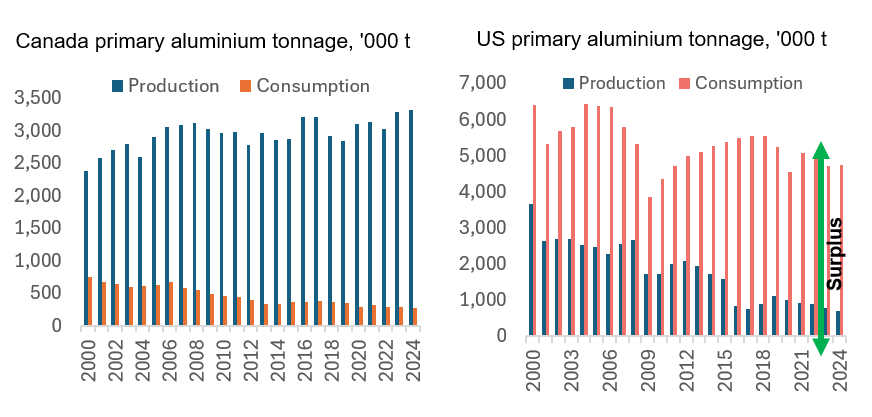

In contrast, Canadian primary aluminum output gradually grew to its highest level, reaching an estimated 3.3 Mt in 2024. Primarily, access to cheap and abundant hydropower has enabled this in tandem with continued provincial and federal government support. However, another key factor in the growth of Canadian output is increased global demand and, in particular, growing demand in the US against a backdrop of declining domestic production. In 2024, CRU estimates that domestic US production was equal to ~15% of domestic consumption.

Tariffs impact boost the case for restarts, but hurdles remain

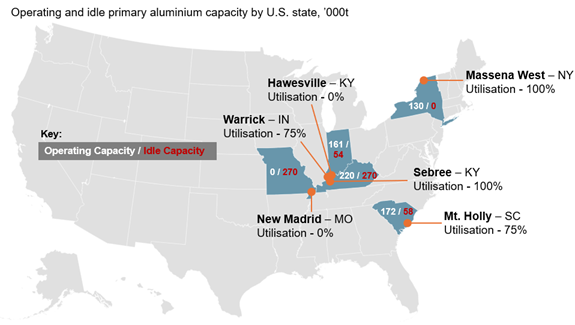

Should Trump enact and maintain a 25% Section 232 tariff on aluminum imports – notably including metal from Canada that was previously exempt – CRU expects the Midwest premium to rise to 42 ¢/lb. This drastically changes the economics of US restarts. At present, CRU estimates that there is ~630 kt of idled capacity that has the potential to restart over the next two years. This includes idle capacity at Mt. Holly, Warrick, New Madrid and Hawesville.

DATA: CRU, company reports

CRU had already expected the restart of the idled Century Aluminum Mt Holly potline (58 kt/y) from Q3 2025 and that Hawesville would also be restarted from Q1 2026 based on the assumption that energy and raw material costs would have declined to a sustainable level. No other restarts were expected in the medium term. The third potline at Warrick was expected to remain offline due to high energy costs and the producer’s emissions reduction targets. Capacity at Magnitude 7’s New Madrid smelter was also not considered viable for a restart due to continued high energy costs, lack of labor and lack of tax relief.

However, CRU believes the imposition of universal Section 232 tariffs at 25% will impact the purchasing power of US aluminum producers. Specifically, CRU analysis shows that the windfall earned should the Midwest premium reach full ad valorem duty, would enable US producers to increase their ability to buy power by ~$30/MWh. This would be sufficient to restart idle capacity at Mt Holly and Warrick. Therefore, CRU maintains the view that Mt Holly will restart from Q3 2025 but acknowledges an upside risk of an earlier restart. A restart at Warrick is forecast from the same time.

The potential restart of the Hawesville smelter faces the additional hurdle of costs associated with restarting capacity from zero. The profitability of the site for data center usage is also under consideration by Century. At this time CRU maintains its forecast for this smelter.

New Madrid also faces similar challenges, despite only being idle for 12 months. Nevertheless, without tax relief or subsidy, CRU believes a restart remains unlikely, particularly if the duration of the tariffs is short-lived. A restart at this smelter remains outside the base case.

Long-term US primary project pipeline remains sparse, imports will be crucial

One of the key stated aims of the tariffs is to onshore and protect the US primary production industry. Only one primary aluminum project has been announced in recent years and this was prior to the tariff announcement. This project is at a very early stage, with location, power source and capacity yet to be publicly detailed. This project is not currently considered in CRU’s long-term project base case as a result.

Even if this project doubles the size of the current US industry as previously announced and all currently idle capacity were to come online (which, as described, is unlikely) the US would still need to import around half of its primary aluminum requirement. This requirement is highly likely to continue to be predominantly met by Canada, which produced more than 10 times its primary aluminum requirement in 2024. CRU expects this trade flow to maintain its importance to both nations, even if Canada decides to diversify its export profile by increasing exports to regions like the European Union.

DATA: CRU

Editor’s note

This analysis was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.