Logistics

January 30, 2025

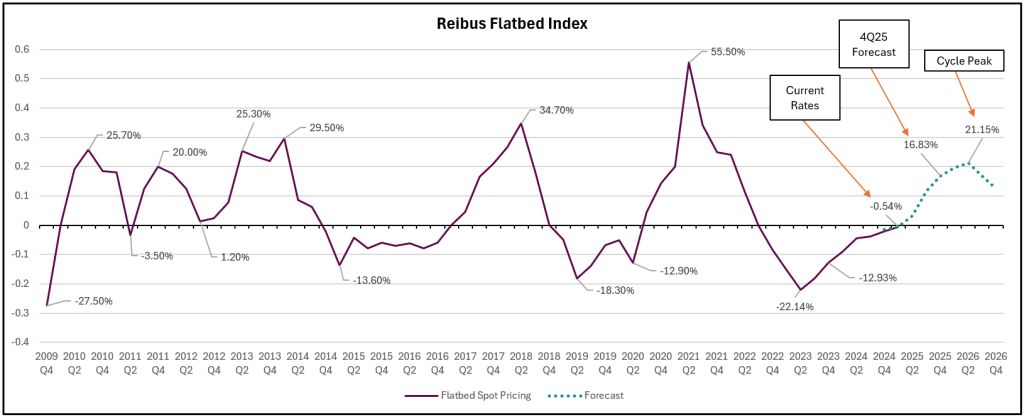

Reibus: Flatbed rates up slightly but uncertainty ahead

Written by Robert Martin

After closing Q4 -1.50% year over year (y/y), flatbed spot rates have ticked up slightly in January bringing our y/y read effectively flat at -0.54%.

With construction seasonally soft, the flatbed market remains softer than the other main trailer types. Hurricane recovery will support demand in 2025, but already high and potentially rising interest rates suggest an unfavorable housing market outlook. The US industrial sector remains soft but resilient with interest rate headwinds and rolling downturns in some sectors like agriculture. Industrial activity will likely increase near term on pre-tariff shipping, pulling forward future activity.

Looking at government backed programs, while it seems increasingly likely that much of the IRA will be cut, the IIJA and CHIPS Act will continue to provide industrial stimulus. Contract rates tend to follow the path of spot rates, and with spot pricing finally on the rise, we expect contract rates to follow suit.

After respective declines of 10% and 2% in 2023 and 2024, we expect flatbed contract rates to begin to tick higher in 2025, likely increasing between 4%-8% on a y/y basis.

Boosted by winter storms Cora and Enzo, the dry van spot market has seen a meaningful uptick for the first time since 2021. Spot rates are currently up 6% on both a month-over-month (m/m) and y/y basis and are up 10% since November.

As the winter weather gives way to warmer temperatures, it remains to be seen whether this

trend will hold. In addition to the weather, pre-trade war shipping is beginning to hit US ports and is

providing a lift in demand. Depending on the severity and timing of tariffs, large shippers pulling inventory forward could continue to support an inflationary rate environment.

DAT’s dry van load to truck ratio continues to gain momentum with a current read of ~5.5:1. With peaks in the range of 8:1 in 2018 and 12:1 in 2021 against troughs in the 1-2 range in 2019 and 2024, this is another sign of strength in the dry van space.

As contract rates have normalized over the past 24 months, comparative private fleet rates

continue to look higher and higher (currently 64% higher than spot rates). It remains to be seen how large shippers will view their private fleets and whether they will start to shrink fleet sizes, opting for lower cost for-hire options.

On the macroeconomic front, the new administration’s proposed tariffs apply tax increases on all

products from Canada and Mexico. The stated goal of these tariffs is to address illegal immigration and drug trafficking. For China, an increase in tariffs on all goods is being considered, with potential increases up to 60% on specific products to curb drug flow and trade imbalances. Other Asian countries may incur increases as well. These measures are expected to reshape international trade dynamics and have far-reaching economic consequences.