Plate

January 30, 2025

Plate report: Mills pushing price up, but still willing to talk

Written by David Schollaert

US plate prices just last week hit their lowest level in more than four years, and a fraction of their all-time high of $1,940 per short ton (st) in May 2022. But repeated mill price hikes this week may have stopped the bleeding and could signal a rebound.

Nucor kicked things off, notifying customers Monday morning of a $60/st price bump on plate products. Evraz North America and SSAB Americas both followed the Charlotte, N.C.-based steelmaker with $60/st increases of their own.

But while there was a clear kneejerk response in the market, it’s not clear if the $60/st bump is off recent mill transactions ranging between $820-860/st as recent as last week, or off the last “official” mill price of $950-975/st in October. One thing is for certain; however, tags have edged up in response to the unified mill pricing blitz.

Here’s the latest

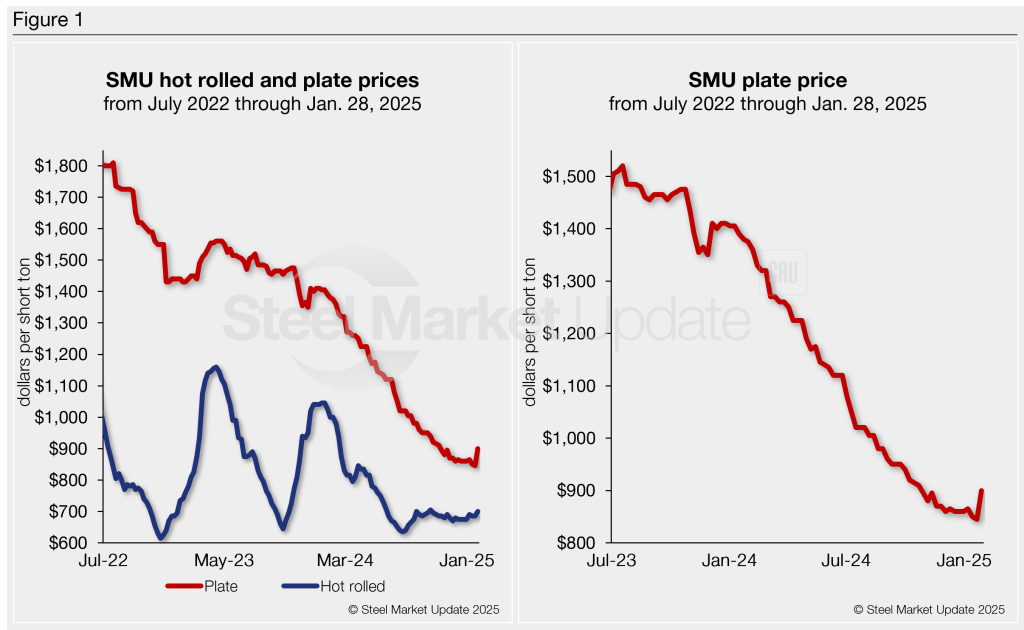

SMU’s plate price stands at $900/st on average based on our Tuesday, Jan. 28, check of the market (see Figure 1, left-side chart), up by $55/st from last week. That marks the highest level for plate prices since late October. It also marks the sharpest week-over-week (w/w) gain for plate since December 2023, according to our pricing archives.

But while some sources have pointed to mill pricing letters as an indicator, most confirmed spot orders between the mid-to-upper $800s and low $900s. And what might be more significant is that buyers are still finding mills willing to talk price, drawing competition among mills and sellers.

By comparison, our HR price is $700/st. HR tags, while up from July’s lows, are roughly just $65/st above 2024’s low and are down $345/st from a recent high of $1,045/st at the start of 2024.

Even though plate prices have seen fewer volatile swings vs. HR, plate tags have been largely trending down since peaking more than two years ago (see Figure 1, right-side chart). Despite this week’s bump, they’re still at some of their lowest levels since December 2020.

Market reaction

The general sentiment among domestic buyers is that mills are still doing what they can, trying to stop the bleeding and set a floor – something that’s been largely elusive for nearly a year. While there is varying sentiment and indicators that plate demand will recover from a slow 2024, most sources are skeptical and question whether the mill push is a bit premature.

“Price announcements haven’t been an accurate representation of transaction prices,” said a large plate buyer. “I saw the announcements but truthfully, I didn’t pay much attention to them.”

“They’re out there but it’s not something the mills are drawing a red line on yet,” said a second source.

“Business is flat,” said another OEM executive. “Some might just say OK, but you’re heavily negotiating a buy unless you’re an idiot.”

More familiar spreads

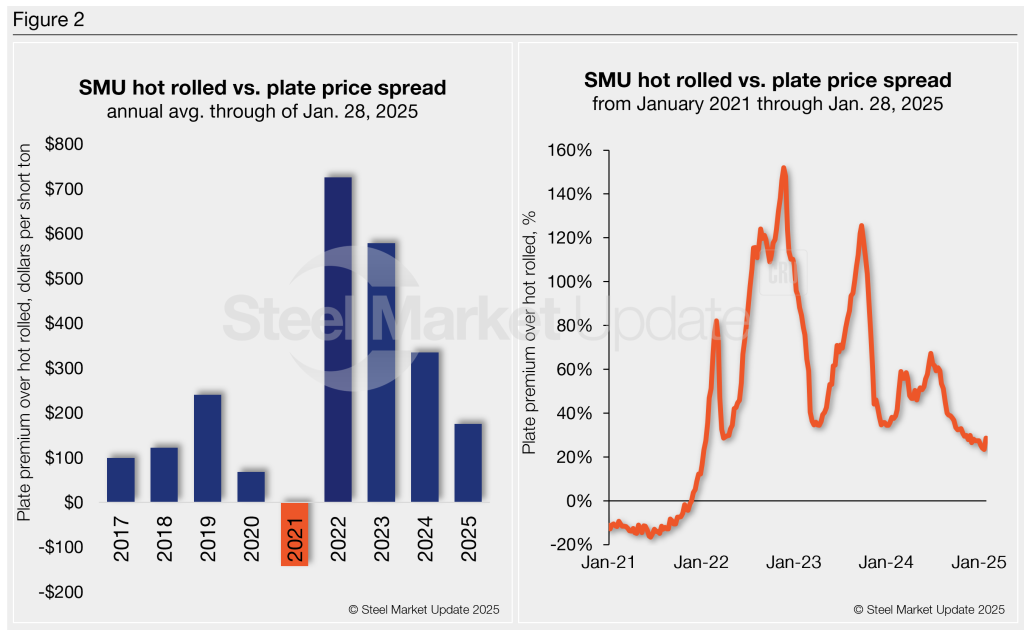

The average spread, or premium, plate had over HR between 2017-20 was $132/st. That all changed after the pandemic. The spread saw major swings before ballooning to $970/st in the summer of 2022. It fell to a three-year low of $160/st last week before jumping to $200/st – still closer to a more historical level (see Figure 2, left-side chart).

On a percentage basis, plate’s premium over HRC skyrocketed to 126% in late September 2023 (Figure 2, right-side chart), reaching a 10-month high. It was also not far from the all-time high of 152% in November 2022. However, with HR and plate prices near recent lows, the premium was as low as 23%, currently at just 28%, and still one of the lowest in nearly two years.

What to watch for

The US plate market has been largely quiet since the second half of 2024. Demand had been driven by inconsistent projects, specifically due to slower-than-expected infrastructure spending. The trend coincided with prices grinding lower and short lead times. It led to an inventory draw down, and service centers running very lean, according to SMU’s December service center inventories analysis.

And mills are aware of that. Nucor said in Tuesday’s earnings call that their plate price increase was driven by improved bookings and backlogs, and lean inventories throughout the supply chain. For them, the “timing was right given those variables.”

Some have suggested that the market is still working to find a bottom, while others believe a bottom was reached. And while Trump has been hating on wind farms – a blow to the plate market – military, transport, and infrastructure spending seems to be picking up.

But the real driver might be that scrap prices could be up between $30-$50 per gross ton (gt) in February due to slow flows and a pick-up in demand, after a $20/gt bump in January.

So, while demand might not be a driving force yet, lean inventories and higher input costs might support slow but improved buying in Q1. It all could push the needle higher, though it might be simply a function of low inventory levels.

Time will tell.