Market Data

January 27, 2025

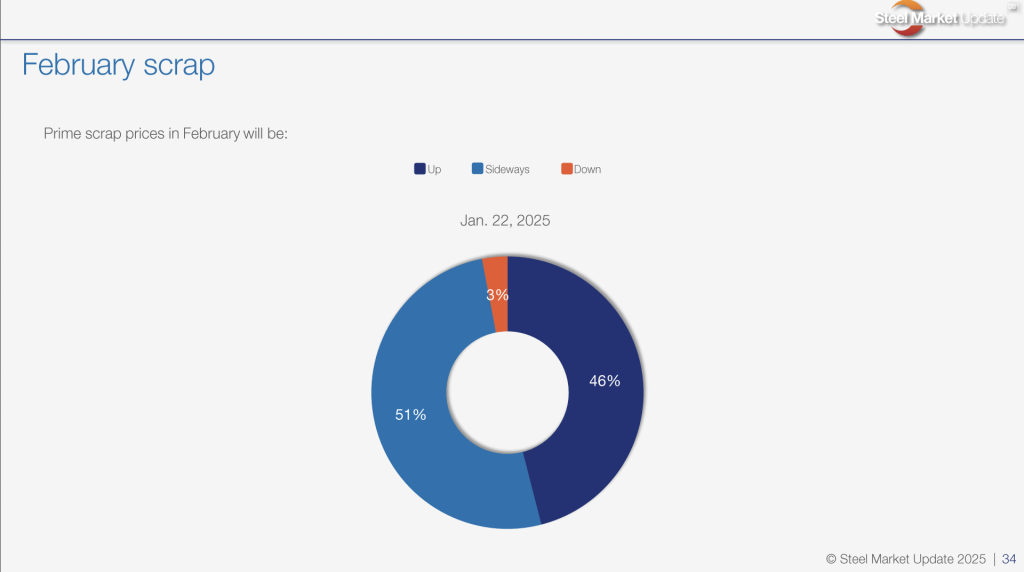

SMU Survey: Majority sees February prime scrap tags flat to up slightly

Written by Ethan Bernard

A majority of SMU survey respondents expect US prime scrap tags to land sideways in February.

In our most recent survey last week, 51% said US prime scrap prices would be flat next month, and 46% anticipate rising prices; the small remainder think prices will fall.

Recall that the January ferrous scrap market settled before President Trump’s inauguration. Therefore, February will mark the first month when the market settles with him in office.

One survey respondent commented on the “Trump effect” as to where prime scrap prices will be in February. While that response is a bit cryptic, it’s hard to deny Trump could impact the market.

We saw within the space of a few hours yesterday that Trump placed tariffs on a country, Colombia, and then, just as abruptly, he removed them when the Colombian government bent to his will.

While Colombia is not a big player in terms of steel shipments to the US, both USMCA partners, Canada and Mexico, are significant trading partners. Let’s not forget that Trump has threatened 25% tariffs on each of them, respectively, as soon as Feb. 1.

With that date just a few days away, the domestic scrap market could be rocked by the impact of tariffs materializing in one or both nations.

Meanwhile, with some responses citing merely seasonal winter activity coming up, we will let the responses speak for themselves.

Here’s what our respondents are saying:

“Scrap increase through Q1/April.”

“Trump effect.”

“Our leading indicators are suggesting scrap has bottomed out and will slightly increase in February and March.”

“Estimate of +$20 per gross ton.”

“Seems like the mills needed more in January, which should bleed into February.”

“Increased steel mill demand will push up prices.”

“Typical winter impacts and resuming of demand.”

“It was a nice bump in January (especially after December), so maybe ‘strong sideways.’”

“Slightly (up) after the present increase.”

“Cold weather will help.”

Just days away…

So, with less than a week to go before the arrival of February, we’ll keep our finger on the pulse of the market. And then it won’t be long before trading picks up and deals are made. As soon as we hear if anything is looking to be beyond ‘normal seasonal activity,’ we’ll be sure to let you know.