Sheet

December 16, 2024

November service center shipments and inventories report

Written by David Schollaert

Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact info@steelmarketupdate.com.

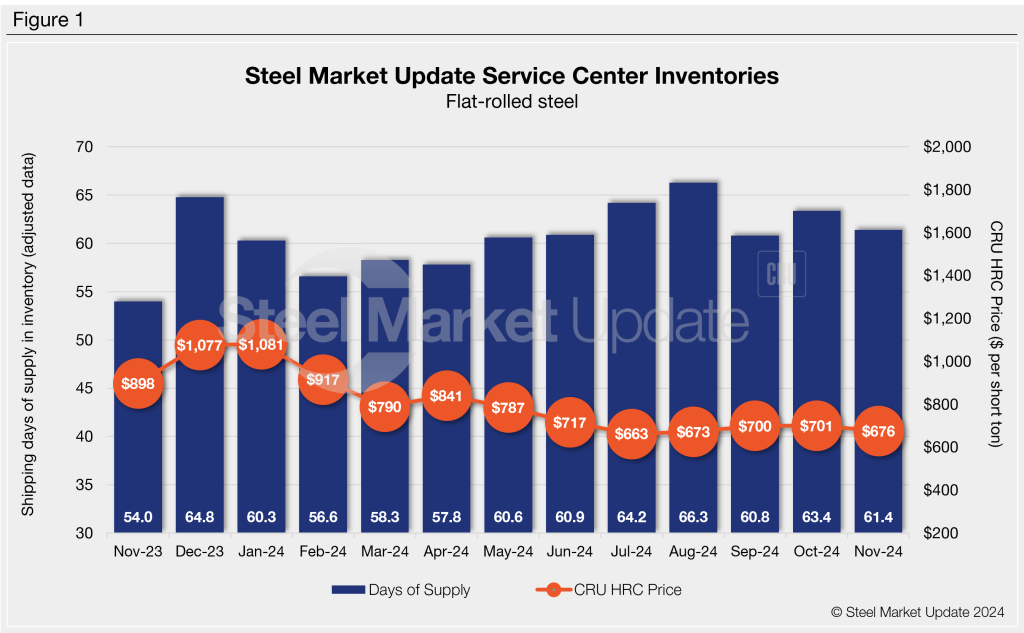

Flat rolled = 61.4 shipping days of supply

Plate = 50.5 shipping days of supply

Flat rolled

Flat-rolled steel supply at US service centers remains seasonally high. November inventories edged down after expanding in October. This dynamic is still being driven by inadequate demand.

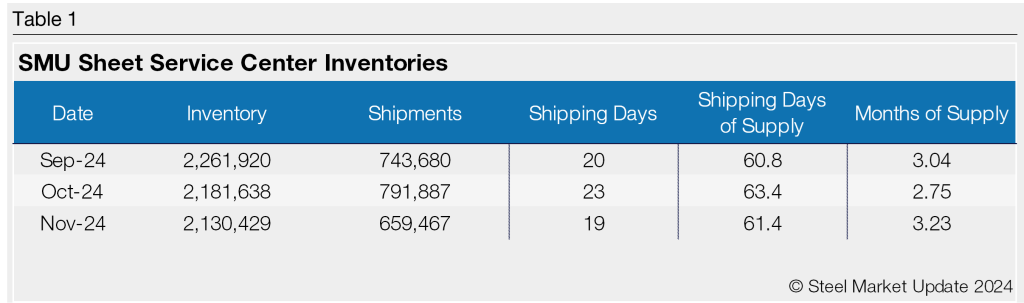

November’s report reflects continued lower demand and slightly shorter lead times that have kept inventory in a surplus and prices in a tight range. At the end of the month, service centers carried 61.4 shipping days of supply on an adjusted basis, according to SMU data.

This is down from 63.4 shipping days of supply in October but up from 54.0 shipping days in November 2023. The result is the highest November since our records began in 2019 and one of the highest monthly figures year to date.

Flat-rolled steel supply in October represented 3.23 months of supply, up from 2.75 months in October. November had 19 shipping days, four less than October, due to the Thanksgiving break. The daily shipping rate was fractionally higher, 0.8% better than October.

The SMU survey data through Nov. 20 showed that more than two-thirds of service centers said they were releasing less steel than a year ago, while 21% said they were releasing the same amount. The rest noted a small uptick in steel releases vs. year-ago levels.

Flat-rolled steel prices have been stable since bottoming out in July. Mills have been publicizing higher prices, but lead times have not responded to date. The Nov. 20 SMU survey marked hot-rolled coil lead times at 4.62 weeks, flat from two weeks earlier. Lead times have been unusually stable for much of the year.

Similarly, the SMU survey also found that 57% of service centers described mill lead times for new orders as “shorter than normal,” while another 39% saw them as “normal.” Service center inventories ballooned at the end of July. Note that we’re now in the slowest shipping period of the year at the close of Q4.

Large buys were leveraged in July when prices were perceived to have bottomed. Flat-rolled steel on order spiked, and lackluster demand since hasn’t aided in correcting inventory levels. The market still seems oversupplied, especially with down demand. Fall outages and a second round of larger buys did very little to stem the tide.

Plate

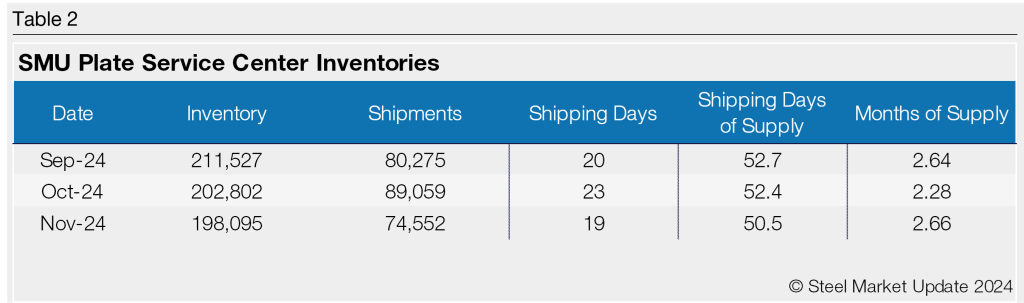

US service center plate supply ticked down again in November as conservative buying patterns prevailed due to ongoing sluggish demand. At the end of November, service centers carried 50.5 shipping days of plate supply on an adjusted basis, down from 52.4 shipping days of supply in October. Plate inventories represented 2.66 months of supply in November, up from 2.28 months of supply in October.

In November 2023, service centers carried 61.7 shipping days of plate supply, representing 3.09 months of supply.

Plate mill lead times are at historic lows (excluding the pandemic), and down roughly 36% from a year ago. Plate lead times averaged 5.86 weeks in 2023. To date, they’ve averaged 4.87 weeks in 2024, remaining at or below the four-week mark since mid-July.

The SMU survey from Nov. 20 found plate mill lead times fell to a historic low of 3.85 weeks. A year ago, a survey reported plate mill lead times of six weeks. Ramped-up new capacity earlier in the year and weaker-than-expected demand have kept the US plate market oversupplied.

With prices falling and weak demand for much of the year, service centers have worked to destock, remaining diligent in managing inventory levels. And with shorter lead times, there has been little incentive to restock. As a result, inventories and material on order remain very low for plate.

While inventories appear more than sufficient to meet immediate demand, the boost of material on order midway through Q4 came even as plate on-order in November was up nearly 38% month over month (m/m), and down nearly 7.8% year over year (y/y). Inventories were down more than 14% vs. October 2023. The daily shipping rate was up 1.3% m/m and 5% y/y, though 2.3% lower year to date.

Lean inventories and a boost of material on order could indicate some positioning for Q1’25 demand. That’s something to track closely if indeed there’s a positive shift in demand. Prices could pop should buyers have to scramble for material.