CRU

December 13, 2024

CRU: Buying interest for scrap remains weak across major regions

Written by Puneet Paliwal

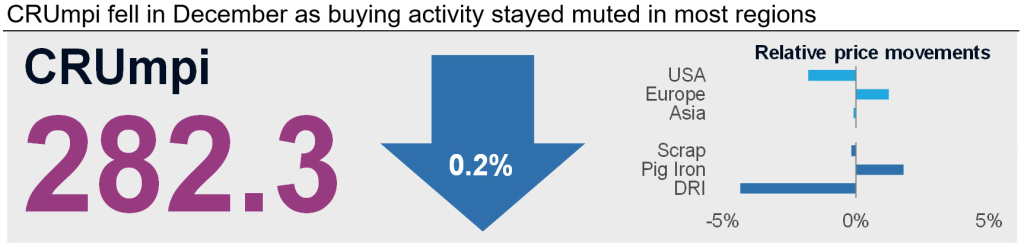

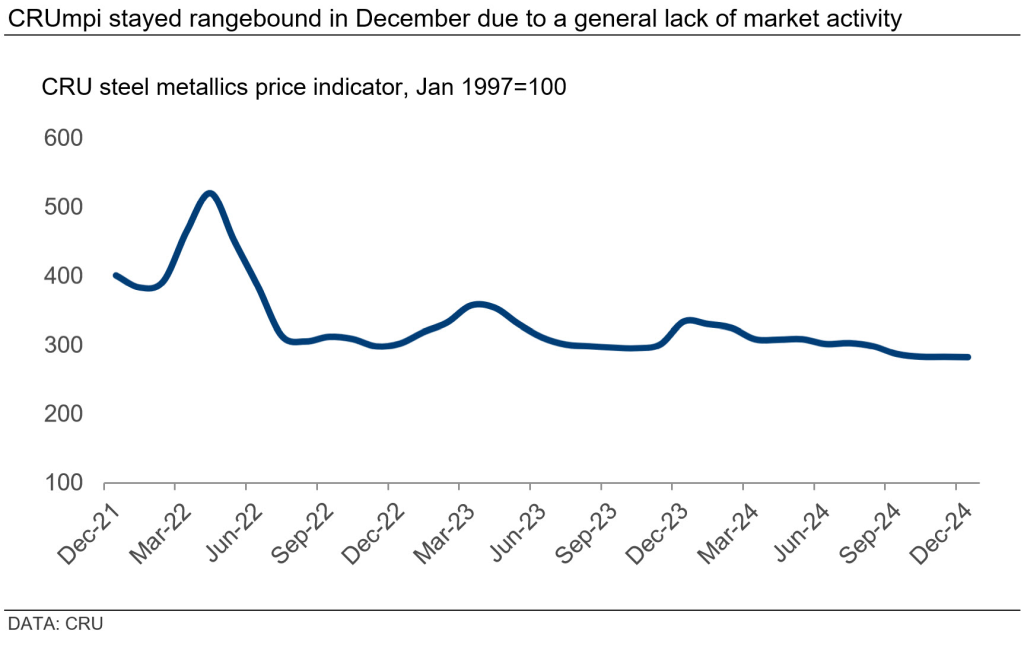

Scrap prices were stable to down in most regions as demand weakness offset seasonal supply tightness. Consequently, CRUmpi fell by 0.2% to 282.3 in December. Mills in Europe and the US are buying scrap sparingly as steel margins remain weak. In Asia, scrap availability and prices are being impacted by Turkish market weakness.

US

In the US, prices for scrap were flat to down across major scrap trading markets, bucking the usual upward trend for December. Buy programs for the month continued to be lackluster due to continued weakness in the finished steel sector. While scrap consumption was down month over month (m/m), dealer inventories are tighter as cold and wet weather reduced traffic to scrapyards. This has bolstered expectations moving into 2025, as restocking in the region could bring with it higher prices. Accordingly, some dealers decided to withhold volumes for future sales.

Nevertheless, scrap prices for this month fell by $10–20 per long ton as demand has been much weaker than supply.

Europe

Meanwhile, European scrap prices rose slightly in December. Obsolete and shredded prices increased marginally up to $5 per metric ton (mt) across European countries as scrap suppliers tried to push for higher prices after months of declining margins. However, Europe is still facing a steel market downtrend as demand from end-users has been in decline in the last weeks in sectors like construction and automotive.

In addition, European steel mills have faced high energy costs and have made attempts to lower production levels to remain afloat, with the Q4 shutdown period expected to last longer than previous years. As finished steel products supply remains adequate and scrap availability is ample, buying interest for scrap remains low in the region. Meanwhile, the Russian government increased the scrap export tariff quota by 100,000 mt to 650,000 mt effective from H2’24 to raise export sales given weak domestic offtake.

Asia

In the Asian market, domestic scrap prices in China and Japan remained unchanged m/m but trade prices declined across the region. For instance, the Japanese scrap export price declined by $24/mt m/m while import prices to Vietnam and Bangladesh reduced by $10/mt and $15/mt m/m, respectively. Subdued scrap pricing in Asia stems from weak Turkish demand and prices as offers to Turkey are being made available in the Asian market for better margins. Meanwhile, domestic demand in Asia is yet to witness a meaningful recovery and weaker margins on finished steel is disallowing mills from accepting higher scrap prices.

Pig iron

Meanwhile, pig iron prices declined in all regions aside from Europe. European prices held strong due to the exhaustion of the EU’s quota for Russian pig iron imports for 2024, requiring buyers to import higher priced material from alternative regions. Meanwhile, Brazilian pig iron export prices have remained under pressure as the primary export destination, the US, is experiencing soft demand and receiving lower priced imports from India.

This analysis was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.