Distributors/Service Centers

November 15, 2024

October service center shipments and inventories report

Written by David Schollaert

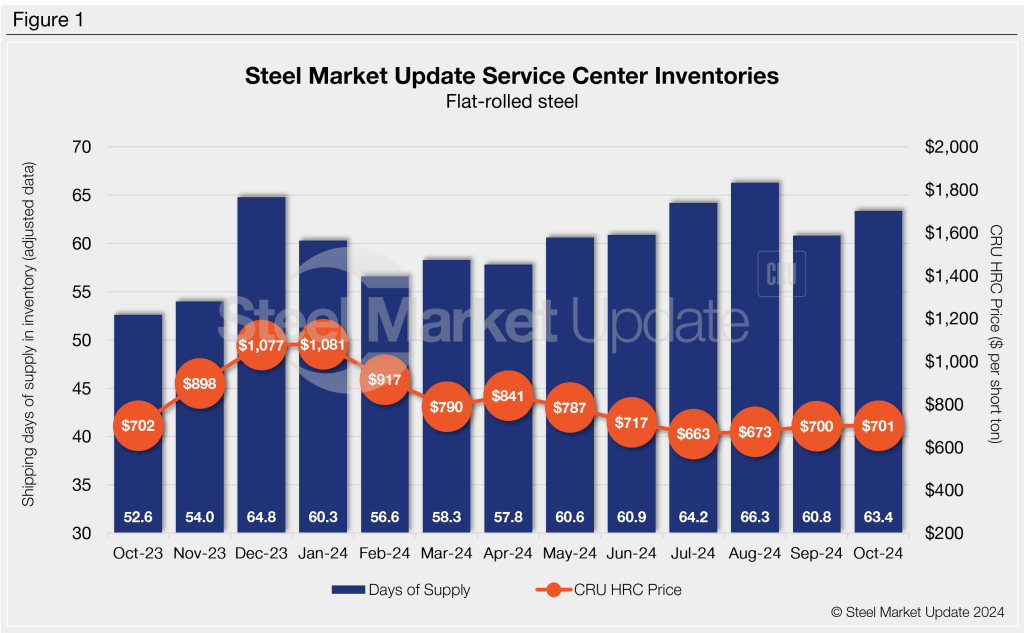

Flat rolled = 63.4 shipping days of supply

Plate = 52.4 shipping days of supply

Flat rolled shipments and inventories

Flat-rolled steel supply at US service centers remains seasonally high. October inventories increased after edging lower in September – a dynamic driven largely by disappointing demand.

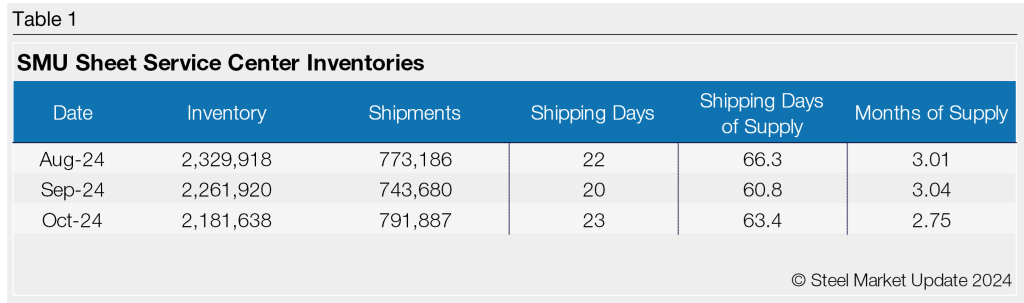

October’s report reflects lower demand and stable lead times that have kept inventory in a surplus and pressured prices lower. At the end of the month, service centers carried 63.4 shipping days of supply on an adjusted basis, according to SMU data.

This is up from 60.8 shipping days of supply in September and up from 52.6 shipping days in October 2023. The result is the highest October since our records began in 2019 and one of the highest monthly figures year-to-date.

Flat-rolled steel supply in October represented 2.75 months of supply, down from 3.04 months in September. October had 23 shipping days, three more than September. Sheet steel shipments aren’t unusually low. The real story might be the daily shipping rate, which fell 7.4% vs. September, and is the largest month-on-month (m/m) percentage drop since July 2019 (excluding the pandemic).

The SMU survey data through Oct. 23 reported that more than three-quarters of service centers said they were releasing less steel than a year ago, while the remaining 23% said they were releasing the same amount. For a second straight month, no service centers said they were releasing more steel vs. year-ago levels.

Flat-rolled steel prices have been unusually stable since bottoming out in July. After increasing in early August, hot-rolled coil prices have averaged $685 per short ton. Mills have been publicizing higher prices. But lead times have not responded to date. The Oct. 23 SMU survey marked hot-rolled coil lead times at 4.60 weeks, down from 4.95 weeks two weeks earlier. Lead times have been unusually stable for much of the year, averaging 4.89 weeks since dipping below five weeks on average in late February.

Similarly, the SMU survey also found that 60% of service centers described mill lead times for new orders as “shorter than normal,” while another 35% saw them as “normal.” Service center inventories ballooned at the end of July. There is no obvious relief in sight as we enter the two slowest shipping months of the year.

At the end of October, service centers’ shipping days of supply on order rose vs. September, those material on order in inventory percentage was down slightly.

The perception that prices were at or near a bottom at the end of July drove many service centers to buy heavily toward the end of the month. Because of the spike in flat-rolled steel on order and the lackluster demand outlook, inventories haven’t corrected since. It points to an oversupplied market even following planned mill outages in September and October.

Plate shipments and inventories

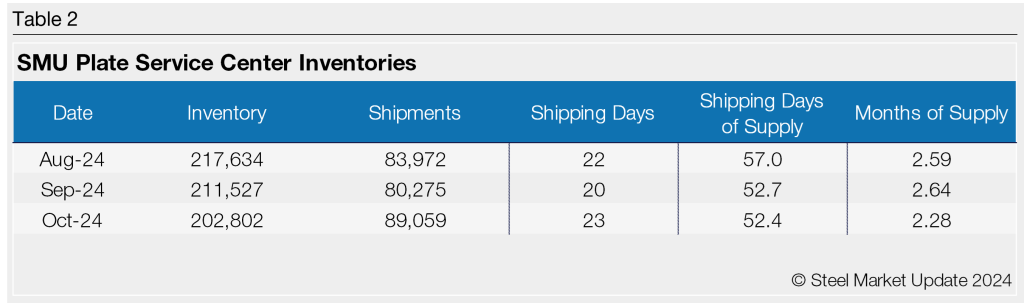

US service center plate supply ticked down again in October as conservative buying patterns continued because of sluggish demand. At the end of October, service centers carried 52.4 shipping days of plate supply on an adjusted basis, down from 52.7 shipping days of supply in September. Plate inventories represented 2.28 months of supply in October, down from 2.64 months of supply in September.

In October 2023, service centers carried 61.8 shipping days of plate supply, representing 3.81 months of supply.

Plate mill lead times are much shorter this year, down roughly 30% from a year ago. Plate lead times averaged 5.86 weeks in 2023. To date, they’ve averaged 4.95 weeks in 2024. And they have been at or below the four-week market since mid-July.

The SMU survey from Oct. 23 found plate mill lead times of four weeks, unchanged from the month prior. The survey a year ago reported plate mill lead times of 6.10 weeks. Ramped-up new capacity earlier in the year and weaker-than-expected demand have kept the US plate market oversupplied.

With prices falling and weak demand for much of the year, service centers have worked to destock, remaining diligent in managing inventory levels. And with shorter lead times, there has been little incentive to restock. As a result, inventories and material on order remain very low for plate.

At the end of October, service centers’ shipping days of plate supply on order was little changed vs. September, but down significantly from October 2023. Plate on order at the end of October as a percentage of inventories was up slightly from September.

While inventories appear more than sufficient to meet immediate demand, the decline of material on order to start Q4 may suggest even tighter inventories in November.

Also, plate on-order in October was up 3.2% m/m and down 30% y/y. Inventories were down nearly 13% vs. October 2023. The daily shipping rate was also down 3.5% m/m and 3.2% y/y, it was below 1.4% lower year to date.

Lean inventories and low material on order should be watched closely. The dynamic could cause pricing to react quickly to even a slightly positive shift in demand. Prices could pop should buyers have to scramble for material.