Plate

October 25, 2024

Plate report: Are prices nearing a bottom?

Written by David Schollaert

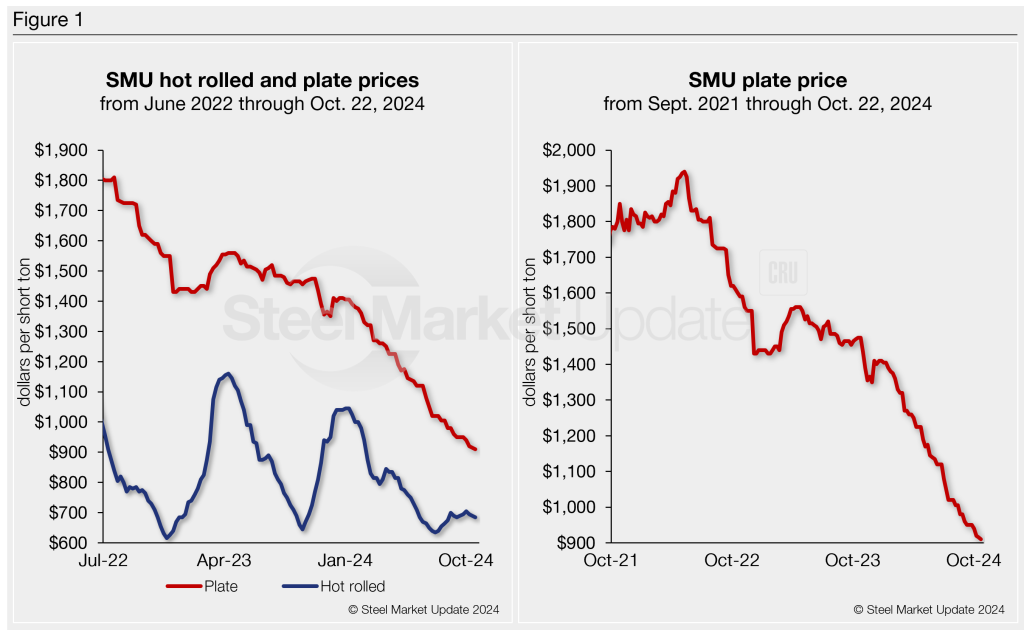

US plate prices are at their lowest level in almost four years and are less than half their all-time high of $1,940 per short ton (st) reached in May 2022.

And mills seem eager to stop the bleeding. Nucor has held its published plate price of $1,075/st flat since slashing it by $125/st back on July 1.

On Thursday, SSAB Americas said it was increasing plate prices by at least $60/st, according to a letter to customers. While SSAB didn’t specify their base prices, it’s their first price increase in nearly a year.

Here’s the latest

SMU’s plate price currently stands at $910/st on average based on our Tuesday, Oct. 23, check of the market (see Figure 1, left-side chart). While some very small spot orders have been reported higher, plate transactions have been in the mid-to-low $800s.

What might be more significant is that smaller volumes are drawing competition amongst mills and sellers. And $1,000/st is far from a competitive number. According to sources, tags have easily been transacting roughly $200/st below Nucor’s published plate price, even for product from the Charlotte, N.C.-based steelmaker itself.

By comparison, our HR price is $685/st. HR tags, while up from July’s lows, are down $360/st since reaching a recent high of $1,045/st at the start of the year.

And even though plate prices have seen fewer volatile swings vs. HR, plate tags have been largely trending down since peaking more than two years ago, especially of late (see Figure 1, right-side chart). Now, they’re at their lowest level since nearly December 2020.

Market reaction

The general sentiment among domestic buyers is that mills are trying to stop the bleeding and set a floor. Some speculate that the move might also help Nucor hold its pricing again when it opens its December order book in a week or so.

“I would have no idea why they would be attempting this increase now,” said a large OEM executive. “Unless they are trying to push Nucor to get their pricing up as well.”

“With Nucor selling well below their published price and having lost their pricing management, it’s like the Wild West,” another source said.

Others note that prices declined even as SSAB took a month-long planned outage at its Montpelier, Iowa, mill in September. Many wonder what might be pushing prices up, especially with distribution centers hurting for demand.

“I don’t see us having any success with customers running it back and letting them know prices are going up,” a plate buyer told SMU. “It’s hard right now to get projects started and off the ground.”

More familiar spreads

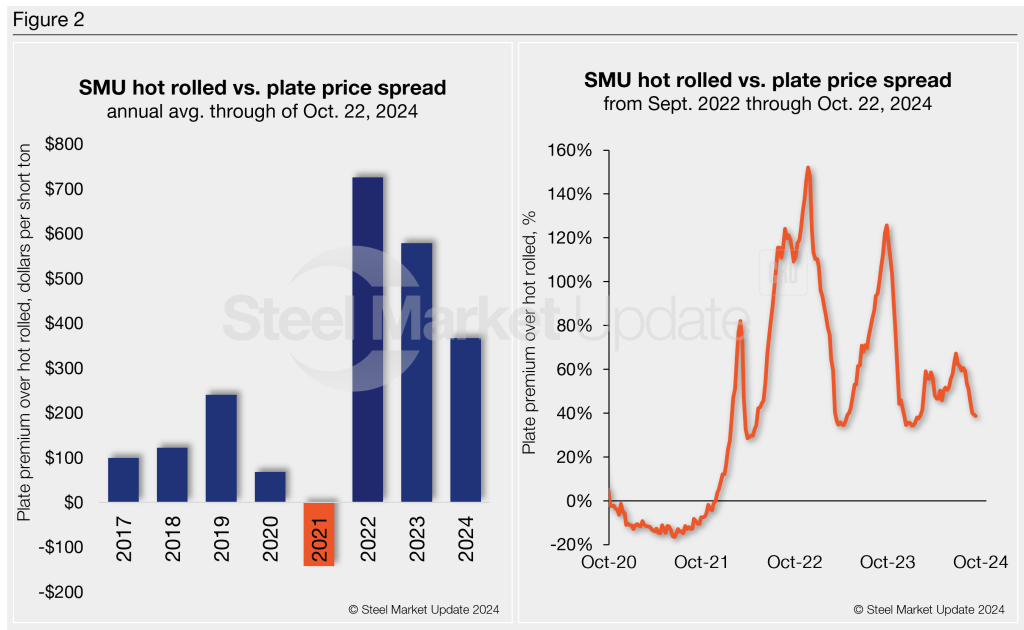

The average spread, or premium, plate had over HR between 2017-20 was $132/st. Volatility took hold in the aftermath of Covid-19, and the spread was all over the place. It reached as high as $970/st in the summer of 2022, but currently sits at almost a three-year low of $225 per ton – closer to a more historical level (see Figure 2, left-side chart).

On a percentage basis, plate’s premium over HRC ballooned to 126% in late September 2023 (Figure 2, right-side chart), reaching a 10-month high. It was also not far from the all-time high of 152% in November 2022. However, with HR prices near recent lows and plate tags declining, the premium is down to just 33%, one of the lowest in recent years.

What’s currently at play

The US plate market has been largely quiet, with demand trending down. The trickle, or even lack thereof, of infrastructure spending and the cancellation of wind farm projects have really cut back on demand for much of the year. Some projects are coming online, and greater demand could be on the horizon. For example, there have been recent reports of plate sales for rebuilding the collapsed Francis Scott Key Bridge in Baltimore.

Also, keep an eye on discrete plate lead times. They have been averaging four weeks, but in many cases, sources note that a three- or even two-week turnaround is possible.

What to watch for

The market is working to find the bottom, and SSAB’s recent pricing notice could indicate a bottom is in sight. The timing, in some ways, makes sense. There’s only about five-to-seven weeks’ worth of business left in 2024. So, there might not be enough time to really gauge if the increase takes hold or has legs.

But also keep an eye on service center inventories. Plate inventories were a bit bloated in July, but they have mostly been worked off through September’s report. We’ve seen shipping days of supply come down steadily, coinciding with daily shipping rates creeping up and material on order leveling off. It might not take much of a demand boost to push prices back up.

We’ll be closely monitoring October’s report due next month. Our flash report should be out in the first week of November, and the final report will be available to SMU premium subscribers on Nov. 15.

Editor’s note: If you’d like to become a data provider for our service center inventory report, please contact David Schollaert at david.schollaert@crugroup.com. If you would like to upgrade your executive account to premium, please contact Luis Corona at luis.corona@crugroup.com.