Market Data

September 17, 2024

August service center shipments and inventories report

Written by David Schollaert

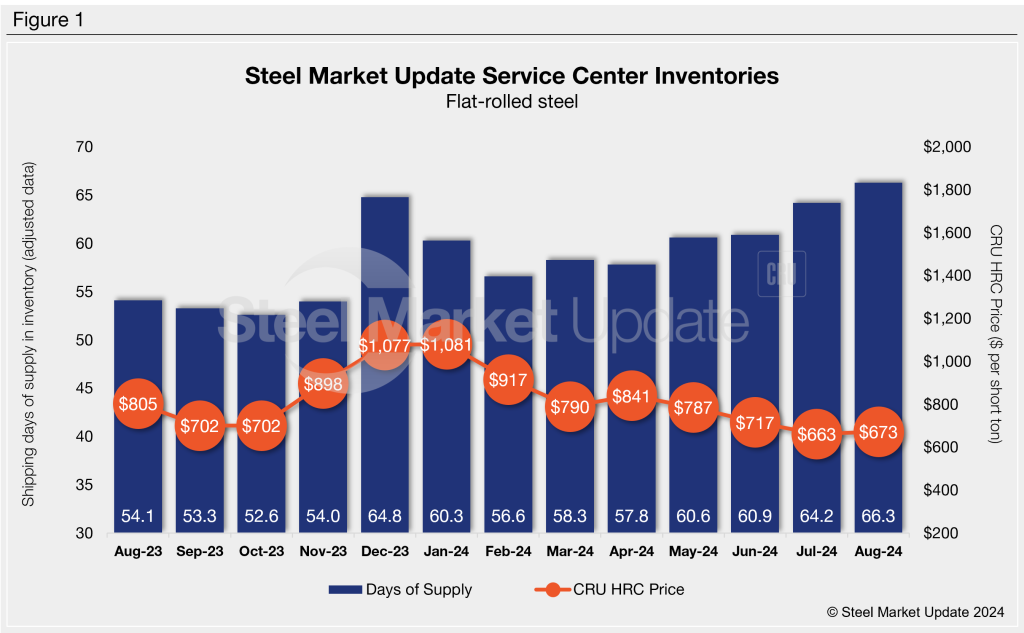

Flat rolled = 66.3 shipping days of supply

Plate = 57.0 shipping days of supply

Flat rolled

Flat-rolled steel supply at US service centers grew further in August. The dynamic resulted from some Q3 restocking efforts at a perceived market bottom, met with shorter lead times and weaker demand. At the end of August, service centers carried 66.3 shipping days of supply on an adjusted basis, according to SMU data.

This is up from 64.2 shipping days of supply in July and 54.1 shipping days in August 2023. It is also the highest total since May 2020, when shipping days of supply reached 67.6 as Covid-19 battered the market.

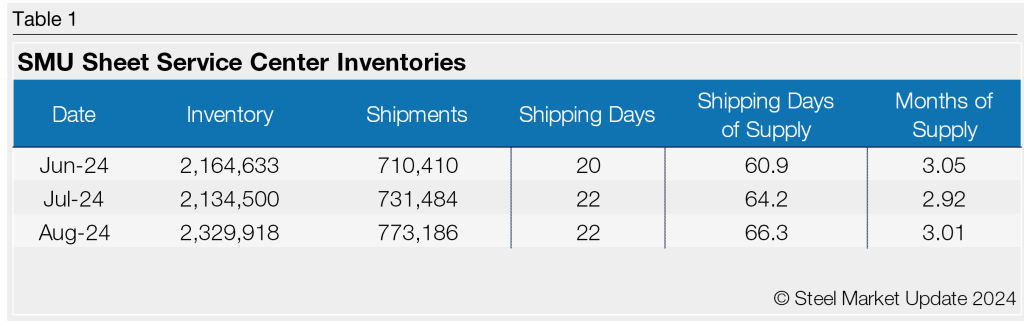

Flat-rolled steel supply in August represented 3.0 months of supply, up from 2.9 months in July. August had 22 shipping days, mirroring July’s total. Sheet steel shipments typically hit a lull in July. The drop-off in shipments was more pronounced this year, and the trend appears to have continued in August.

The SMU survey with data through Aug. 28 reported that 80% of service centers said they were releasing less steel compared to a year ago, while 13% said they were releasing the same amount, and just 7% said they were releasing more steel.

Flat-rolled steel prices edged up some in August but have been largely stable, seeing just moderate gains over the past four weeks. Mills have been publicizing higher prices but lead times have been slow to react. The Aug. 28 SMU survey pegged hot-rolled coil lead times at 5.19 weeks, up from 4.9 weeks two weeks earlier and from 4.54 weeks on July 31.

Similarly, the SMU survey also found that 8% of service centers described mill lead times for new orders as “extremely short” and 36% said lead times were “shorter than normal.” Still, another 50% saw them as “normal.” Service center inventories ballooned at the end of July, with little relief in August.

The perception that prices were at or near the bottom at the end of July drove many service centers to buy heavily toward the end of the month. Because of the spike in flat-rolled steel on order and the lackluster demand outlook, inventories increased further in August. Even with the slew of planned mill outages in September and October, the market seems to be oversupplied relative to demand.

Plate

US service center plate supply ticked down in August due to tighter buying patterns on sluggish demand. At the end of August, service centers carried 57.0 shipping days of plate supply on an adjusted basis, down from 60.9 shipping days of supply for July. Plate inventories represented 2.6 months of supply in August, down from 2.8 months of supply in July. In August 2023, service centers carried 61.2 shipping days of plate supply, representing 2.66 months of supply.

Plate mill lead times are much shorter this year; however, nearly half what they were a year ago. The SMU survey from Aug. 28 found plate mill lead times at 3.93 weeks, flat from a month prior. The survey a year ago reported plate mill lead times at 5.25 weeks. Ramped-up capacity this year and weaker-than-expected demand have kept the US plate market oversupplied.

With prices falling and weak demand, service centers have been trying to destock for months. There has been little incentive to restock, though, with lead times being so short. As a result, material on order remains extremely low for plate.

While inventories appear more than sufficient to meet immediate demand, the lower material on order could suggest a further drop in inventories in September.

Keep in mind that plate on-order was down 3.8% m/m and 28.1% y/y in August. Inventories were down 6.4% vs. August 2023. So, while the daily shipping rate was 4.3% higher m/m, it was 5.3% lower year to date and 0.5% lower than August 2023.

This, combined with SSAB’s pulled-forward outage, could allow plate price decreases to reach a bottom. However, this could also cause supplies to tighten quickly if service center shipments pick up in the slightest, especially with SSAB’s outage, as inventories and material on order are down from normal levels.