CRU

August 9, 2024

CRU: Unpacking China’s recent policy agenda

Written by Henry Hao

China’s recent policy shifts are reshaping the economic landscape, with significant implications for the commodity markets. While the government is committed to fostering innovation and boosting domestic demand, a cautious approach to balancing economic growth with long-term structural reforms and the emphasis on state-led development could limit the upside for growth.

While the focus on innovation and infrastructure investment offers potential upside for certain metals, concerns over property market weakness and the evolving regulatory landscape should temper overall optimism – particularly for steelmaking materials. This analysis delves into the key policy changes, their potential impact on commodity-related industries, and the challenges and opportunities that lie ahead.

Reforming the existing model for new productive forces

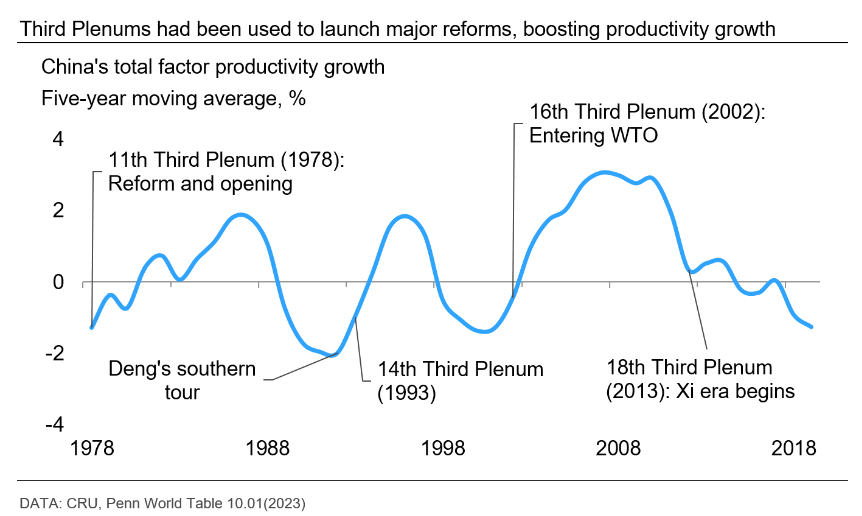

The Third Plenum historically marks a pivotal moment in China’s policy landscape. Deng Xiaoping’s 1978 reforms – launched at a previous plenum – catalyzed decades of rapid growth. While subsequent meetings yielded less dramatic changes, the recent gathering was highly anticipated due to unusual delays and, more importantly, the economy’s challenges.

However, the plenum’s focus on refining rather than overhauling the economic model disappointed markets, but it still aligned with our expectations. The subsequent release of a comprehensive (yet incremental) reform blueprint outlined a five-to-ten-year roadmap to modernize China. Central to this plan is the cultivation of “new productive forces” (NPFs) to drive technological advancement and supply chain resilience – a response to China’s waning productivity growth (see chart below).

While the whole-of-nation approach to developing NPFs promises breakthroughs in strategic sectors such as green tech, it also risks distorting market forces and hindering long-term efficiency. The push for innovation, particularly in high/green-tech manufacturing, is likely to drive demand for specialized metals and rare-earth elements.

However, the state-led innovation push could further risk exacerbating production overcapacity, resource misallocation and deflationary pressures, potentially undermining long-term productivity growth.

Tax reforms to improve local public finance

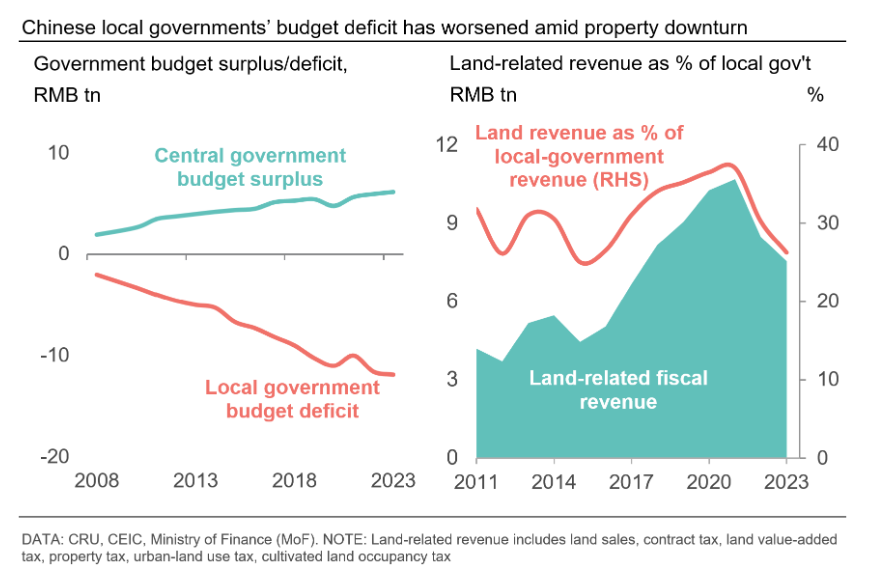

During the Third Plenum, the Chinese authorities addressed fiscal challenges through tax reforms aimed at enhancing local government revenues. The recent resolutions propose increasing the share of tax revenues allocated to local authorities and reducing their spending obligations.

This approach includes reallocating consumption tax revenue to local levels and exploring new revenue streams from digital economy sectors. These measures are crucial in light of weakened revenue collection capacities and declining land sales, necessitating a robust framework to ensure fiscal sustainability at both local and national levels (see chart below).

Looking ahead, we expect fiscal reforms to enhance public finance sustainability, particularly at local levels. The central government will increase spending and borrowing to counteract local governments’ fiscal cutbacks, constrained by off-budget debt clean-up and reduced land sale revenue due to the property downturn. Authorities might allocate more tax revenue to lower government levels or transfer some local responsibilities to the central government.

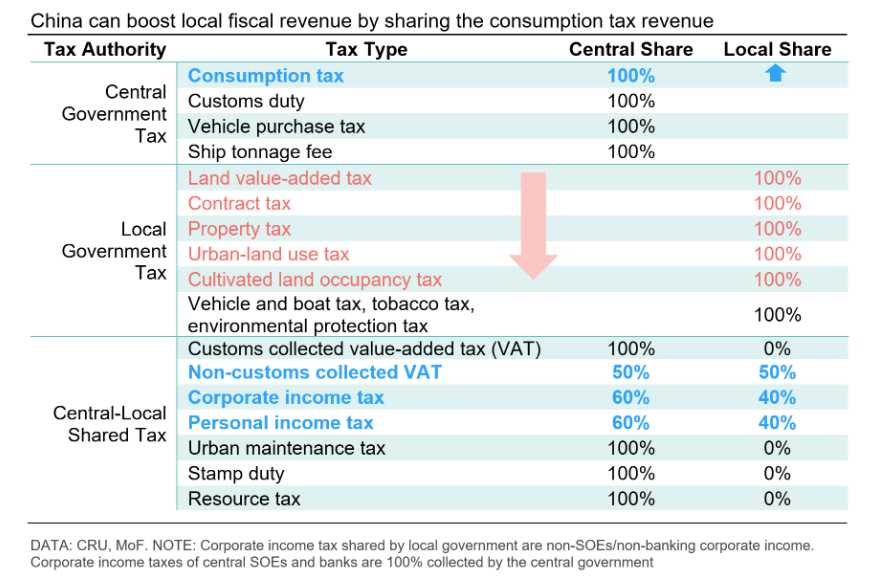

Efforts to boost local fiscal revenue are anticipated. The tax authorities will be shifted downward to expand local tax bases and develop local tax types. Among China’s four major taxes, value-added tax, corporate income tax, and personal income tax are shared between central and local governments, while the consumption tax is currently central only (see table below).

If the consumption tax is partially shared, local governments’ tax bases would broaden, increasing their incentive to promote consumption and shift the economic structure towards consumption. Otherwise, the heavy reliance on land sales and VAT in local revenue could push local governments to keep expanding production tax bases, resulting in overcapacity and redundant construction.

New urban push drives housing and infrastructure demand

A few days after the Third Plenum, China unveiled its new urbanization action plan to accelerate urban development while improving living standards. By easing restrictions on rural-to-urban migration, fostering industrial clusters, enhancing infrastructure, and improving urban resilience to natural disasters, the plan emphasizes the importance of people-centered urbanization. This ensures that all residents – particularly migrant workers and their families – have access to public services and opportunities.

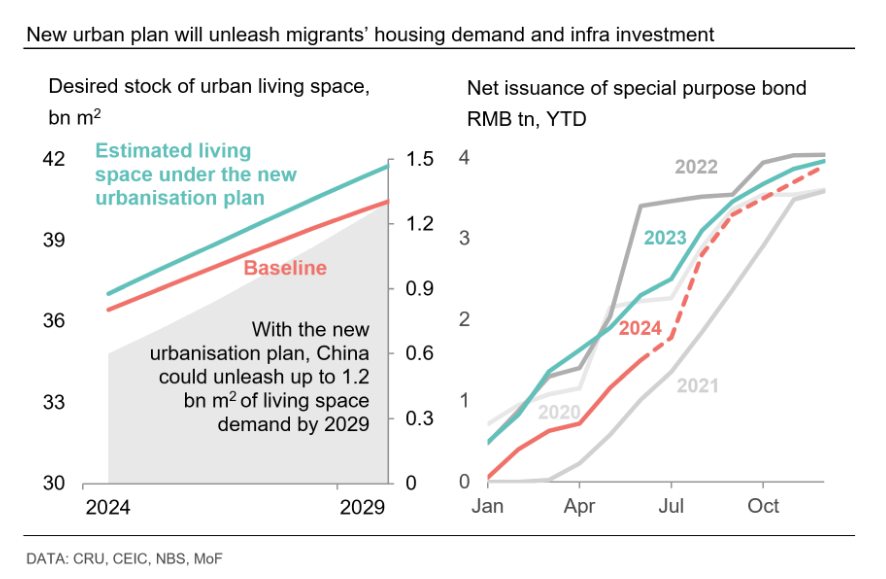

This new urbanization plan is set to impact China’s real estate and infrastructure sectors. The increased demand for housing, driven by granting migrant workers urban resident status (i.e., “Hukou”) and improved living standards, will likely digest the housing inventory in the property market.

By 2029, the plan could unleash an additional 1.2 billion square meters of living space demand compared to our baseline scenario (see left-hand side of the chart below). Meanwhile, the infrastructure sector stands to benefit from the planned investments in transportation, utilities, and public facilities as local governments accelerate the issuance of local-government special purpose bonds (see right-hand side of the chart below).

Enhanced plans to boost investment and consumption

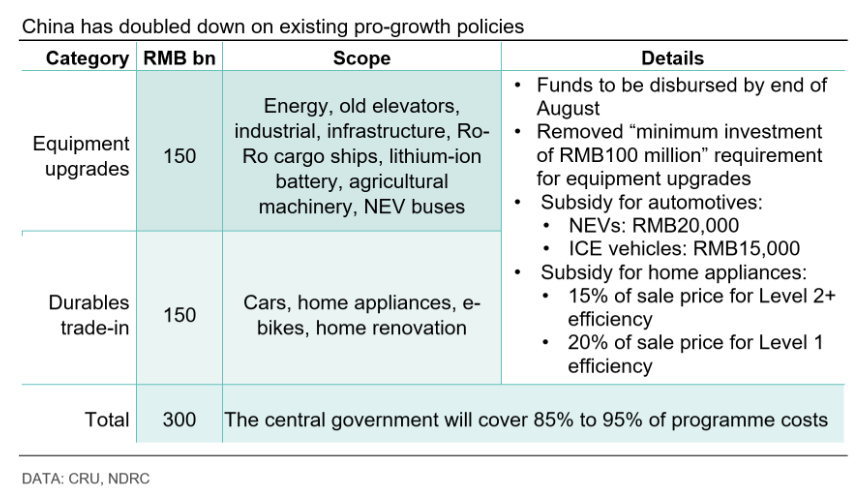

China is also expanding its equipment upgrade and durables trade-in program. Initially rolled out in March, the program faced challenges due to insufficient funding and lack of local incentives. However, the revised program will repurpose 30% of the RMB1 trillion (~US$140 billion) in special treasury bonds for this initiative, significantly increasing fiscal support.

Doubling subsidies for passenger cars and expanding incentives for commercial vehicles and home appliances are expected to drive consumption and investment (see table below). This demand-side policy, though limited in scope, represents a crucial effort to invigorate economic activity amid subdued consumer sentiment.

Incremental policy changes limit the upside to growth

China’s recent policy decisions underscore an incremental approach. On one hand, a strong emphasis on supply-side reforms, technological innovation, and industrial policy aims to address structural economic challenges and foster long-term growth. While these initiatives are crucial, the absence of substantial demand-side measures – particularly in the real estate sector – remains a significant concern. The property market, a key economic driver, continues to face headwinds, and the government’s cautious approach to policy adjustments has limited its recovery potential.

The push for industrial upgrading and infrastructure development could drive demand for certain metals such as copper and steel. However, broader market sentiment remains subdued due to concerns over economic growth, policy uncertainty, and potential market distortions arising from state-led initiatives. The effectiveness of the government’s policies in stimulating sustained economic growth and improving market confidence will be crucial in determining the future trajectory of China’s economic outlook.

If you are keen to hear more about our views on China and the global economy, please refer to our Global Economic Outlook and/or get in touch with CRU economists:

Henry Hao: Hangwei.Hao@crugroup.com

Alex Tuckett: Alex.Tuckett@crugroup.com

Further contribution from intern Brian Tan.

This analysis was first published by CRU. To learn more about CRU’s services, visit www.crugroup.com.