Market Data

February 7, 2024

Consumer confidence accelerated in January

Written by David Schollaert

Consumer confidence in the US rose in January and accelerated to a two-year high, The Conference Board reported. Results came amid slacking inflation and expectations that the Federal Reserve could soon start cutting interest rates.

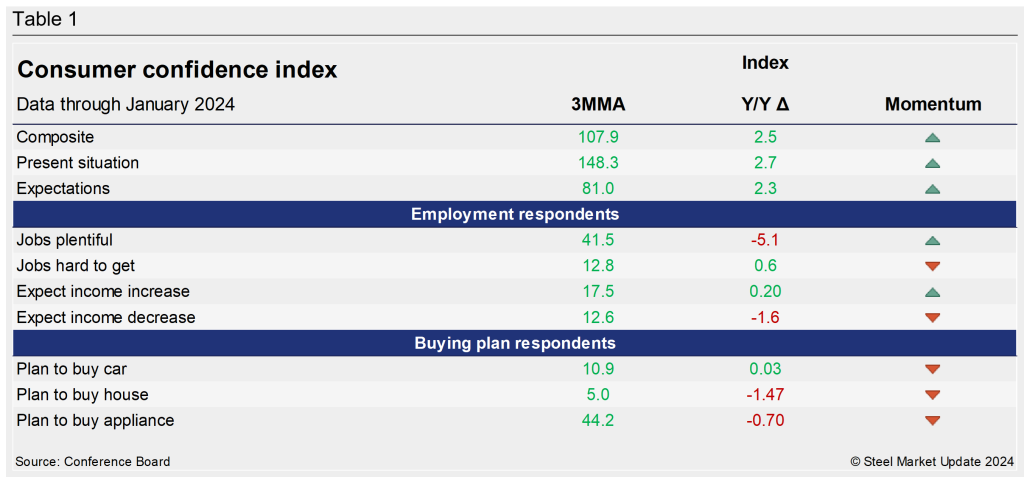

The headline Consumer Confidence Index rose to 114.8 in January from a downwardly revised 108.0 in December. The index, which measures Americans’ assessment of current economic conditions and their outlook for the next six months, was at its highest level since December 2021.

Both the Present Situation and the Expectations indices also improved from December. Despite the uptick in confidence, consumers’ intent to purchase homes, autos, and big-ticket items declined modestly, the report noted.

“January’s increase in consumer confidence likely reflected slower inflation, anticipation of lower interest rates ahead, and generally favorable employment conditions as companies continue to hoard labor,” said Dana Peterson, The Conference Board’s chief economist. “The gain was seen across all age groups, but largest for consumers 55 and over.”

Responses from consumers showed they remain concerned with “rising prices although inflation expectations fell to a three-year low,” Peterson added.

Buying plans dipped last month, though consumers’ perception of a US recession over the next 12 months declined again, consistent with a rising Expectations Index, the report said.

The Present Situation Index, which measures consumer sentiment toward current business and labor market conditions, surged in January, rising 14.1 points to 161.3. The Expectations Index, which assesses the short-term outlook for income, business, and labor market conditions, moved higher to 83.8, up 1.9 points from the prior month’s reading.

Calculated as a three-month moving average (3MMA) to smooth out volatility, The Conference Board’s Composite Index was 107.9, a 5.2-point increase vs. December, marking January as the third straight month to see an increase.

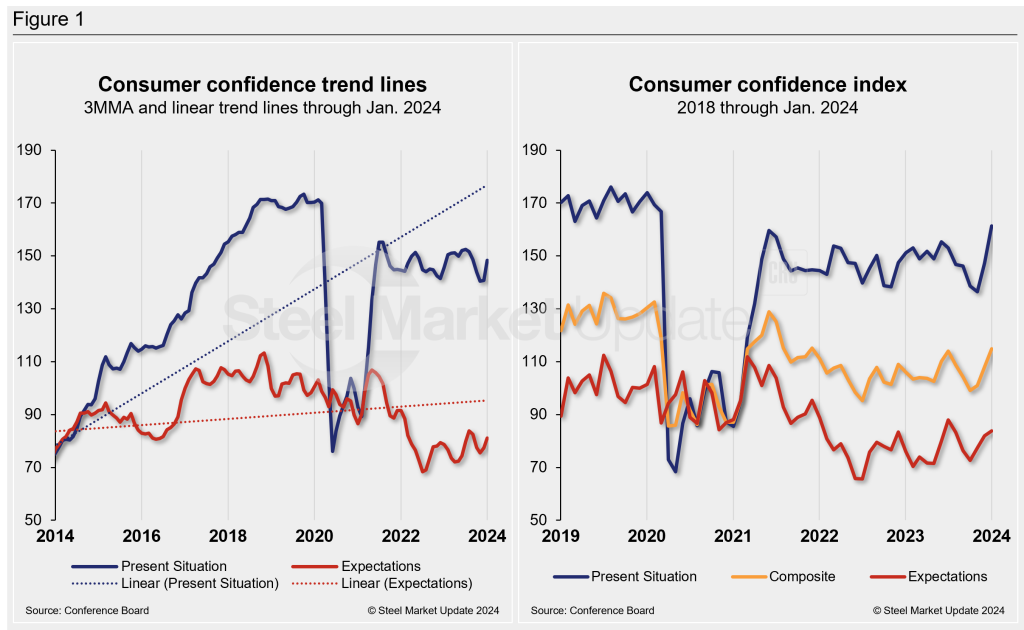

The Composite Index is made up of two sub-indexes: Consumers’ view of the present situation and their expectations for the future. Figure 1 below notes the 3MMA linear trend lines from January 2014 through January 2024 vs. the trend lines of all three subcomponents of the index: Present Situation, Composite, and Future Expectations. All three were above the average composite line of 94.5 before the pandemic, then fell consecutively through February 2021. A surge from March through June of 2021 pulled all three indexes above the composite line once again. However, economic uncertainty continues to weigh on expectations, keeping them below the average.

The table below compares January 2024 with January 2023 on a 3MMA basis. The headline index and both of its two sub-indexes have been on the rise on a year-over-year (y/y) basis. All three indexes have seen tempered gains, with the Present Situation leading the way by a small margin.

When compared to the same 2019 pre-pandemic period, the Composite Index is still behind by more than 20 points on a 3MMA basis. The Present Situation is down nearly 23 points, while the Expectations reading is down roughly 19 points this month when compared to the same period in 2019. The Consumer Confidence report includes employment data and purchase plans. These are summarized in the table below.

The present situation jumped in January “buoyed by more positive views of business conditions and the employment situation,” according to the report, as family financial conditions were reportedly improved, suggesting “consumers are starting off the year in good spirits about their current finances.”

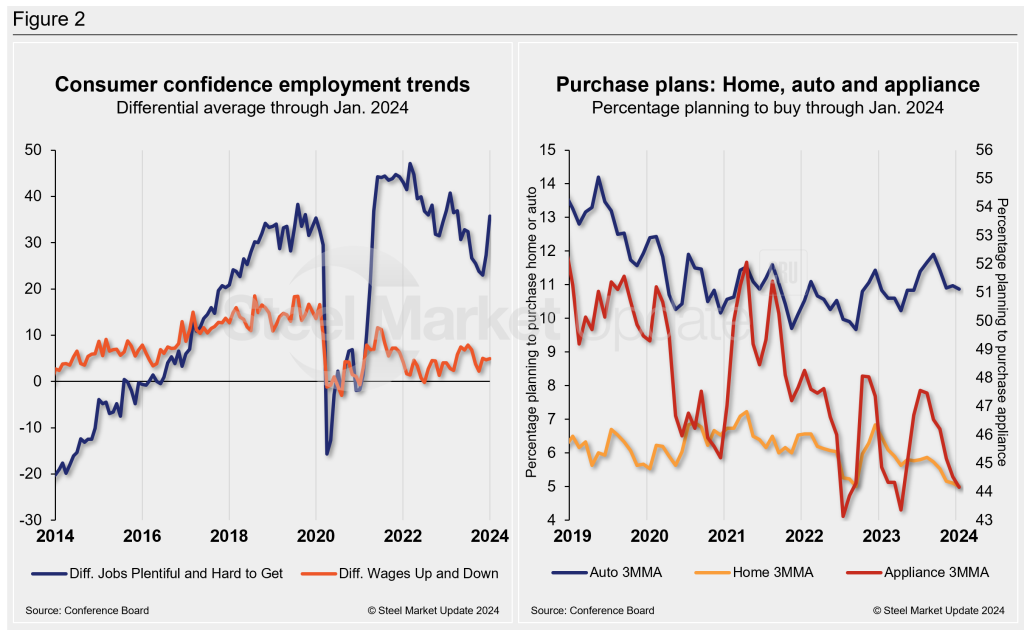

The differential between those finding jobs and those having difficulty was 35.7 in January, up from 27.5 in December. The measure is at its highest level since April 2023 but still a ways away from the most recent high of 47.1 set in March 2022. The difference between those expecting wages to rise vs. those expecting wages to decine moved up to 4.9 in January from 4.7 the month prior and was well removed from the recent high of 11.6 in June 2021.

Buying intentions for big-ticket items — cars, homes, and major appliances — were all down slightly in January, and have been mostly trending lower over the past few months.

The share of consumers planning to buy motor vehicles, homes and appliances such as refrigerators and washing machines all declined m/m.

These recent dynamics and historical movements are illustrated below in Figure 2.

Note: The Conference Board is a global, independent business membership and research association working in the public interest. The monthly Consumer Confidence Survey®, based on a probability-design random sample, is conducted for The Conference Board by Nielsen. The index is based on 1985 = 100. The composite value of consumer confidence combines the view of the present situation and of expectations for the next six months.