Prices

October 12, 2023

HRC Futures: Addressing Risk in Uncertain Times

Written by Josh Pankratz & Logan Davis

If the last few years have taught us anything, it is that nothing is certain. This past weekend we saw yet another unexpected event begin to unfold in the Middle East. In the aftermath, we lack clarity in the responses of many global actors, and ultimately where and how this will percolate throughout the world. The human and geopolitical consequences are well documented and speculated on in other publications and media outlets. Thus, I encourage you to seek other sources if you are interested in those theories.

For those of us who make our living in the steel industry, we eventually need to think about how this may impact our markets and our companies.

The hot-rolled coil (HRC) futures market is currently navigating through a period of exceptional volatility and uncertainty. The United Auto Workers (UAW) strike’s impact (including the expansion to the Ford Kentucky plant on Oct. 11), speculator behavior, market activity, and the situation abroad are all contributing to a complex pricing environment. As the industry watches for further developments, it remains clear that the steel market’s resilience and capacity for surprises continue to define its character.

What can be done to address risk in times where market clarity is virtually non-existent?

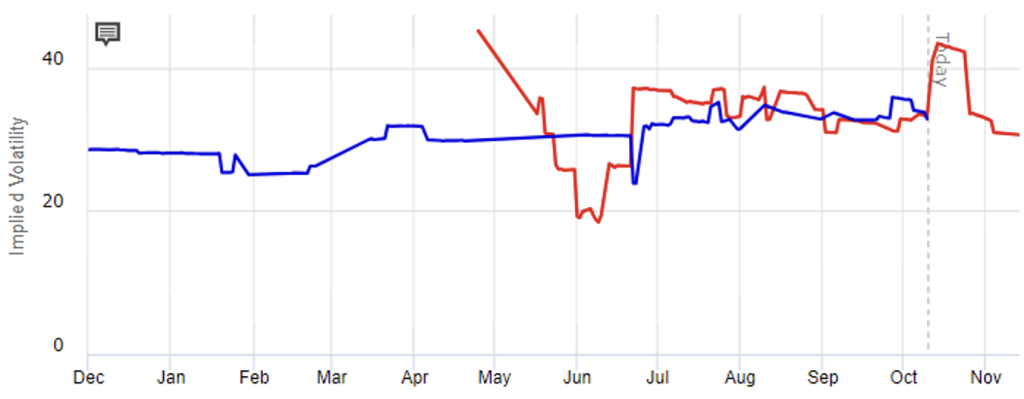

Options can be thought of as insurance in many cases. Just like with insurance premiums, if the insured carries an elevated risk, the premiums can be expected to be more expensive. Given the market conditions described above, it is no surprise that option premiums are historically high. Implied volatility, the measure of what options markets think volatility will be over a given period of time, is a good indication of how cheap or expensive options are. You can see that December HRC implied volatility has risen over the past few months, although it is about even with year-ago levels. The blue line in 2023 implied volatility and the red line is 2022.

If money was no issue, buying an option (call protects against upside risk, put for downside) would always be the best risk management tool as they provide unlimited protection and unlimited participation. Money doesn’t grow on trees, so the cost of premium must be considered. The options market allows participants to sell “insurance” around their owned options. This can be a great way to reduce the cost of your protection.

It is also prudent to evaluate a range of protection a hedger needs. A trader can produce a strategy at no cost, or even a credit, but will generally have to give something up to accomplish this. Currently, strategies with a ranges of $100 per ton on either side are costing around $20-25/ton.

For Buyers

Steel buyers can buy a $825 call option for ~$45 per ton. They could also sell a $600 put option and a $950 call option, collecting a total of ~$22 ($10 and $12, respectively). Net, the strategy would cost about $23 per ton and provide protection from $825 to the contract highs we saw last spring. The hedger would participate in lower prices until $700.

For Sellers

Steel sellers can implement a three-way strategy by purchasing a $800 put for ~$43.00 per ton, and simultaneously selling both the $700 put and $925 call. The resulting strategy would carry a net cost of ~$24.00 per ton ($10.50 and $13.50 respectively). Leaving the hedger with protection down to $700 and participation all the way to $925, last seen in March of this year.

There is risk in futures and options trading.

- Both strategies would carry potential margin risk (capital call).

- Both strategies involve limitations to protection and participation.

- Offsetting either strategy before expiration will change the cost and P/L.

When trading options, positions should be managed as the market changes and time passes.

Options pricing above based on theoretical values. There is a risk of loss in futures trading. Past performance is not indicative of future results.

© 2023 Commodity & Ingredient Hedging, LLC. All rights reserved.

Josh Pankratz

Read more from Josh Pankratz