Market Data

May 11, 2023

Buyers Find More Sheet Mills Willing to Negotiate Lower Prices

Steel sheet buyers find mills more willing to negotiate lower spot pricing now than at any time since late November, according to SMU data.

All the sheet products SMU tracks saw mills more willing to talk price this week. Plate bucked that trend.

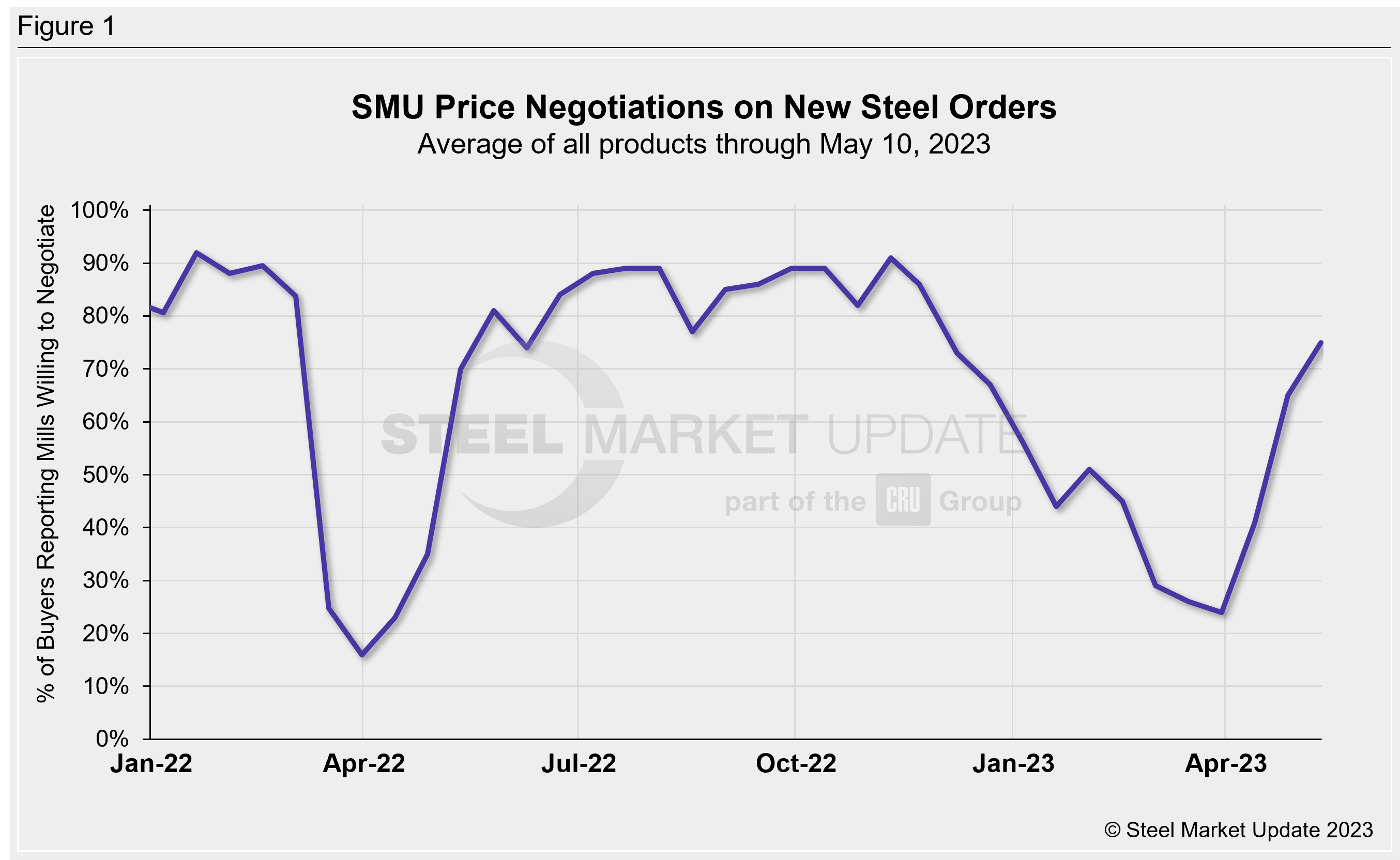

Every two weeks, SMU asks steel buyers whether domestic mills are willing to negotiate lower spot pricing on new orders. This week, 75% of steel buyers (Figure 1) across both sheet and plate markets reported that mills were willing to negotiate cheaper tags on new orders, a 10-percentage point increase from 65% two weeks ago. This is the highest level since around the Thanksgiving holiday, when it stood at 86%. Late November was also when SMU’s hot-rolled price hit a 2022 low, falling to an average of $615 per ton during the week of Nov. 22.

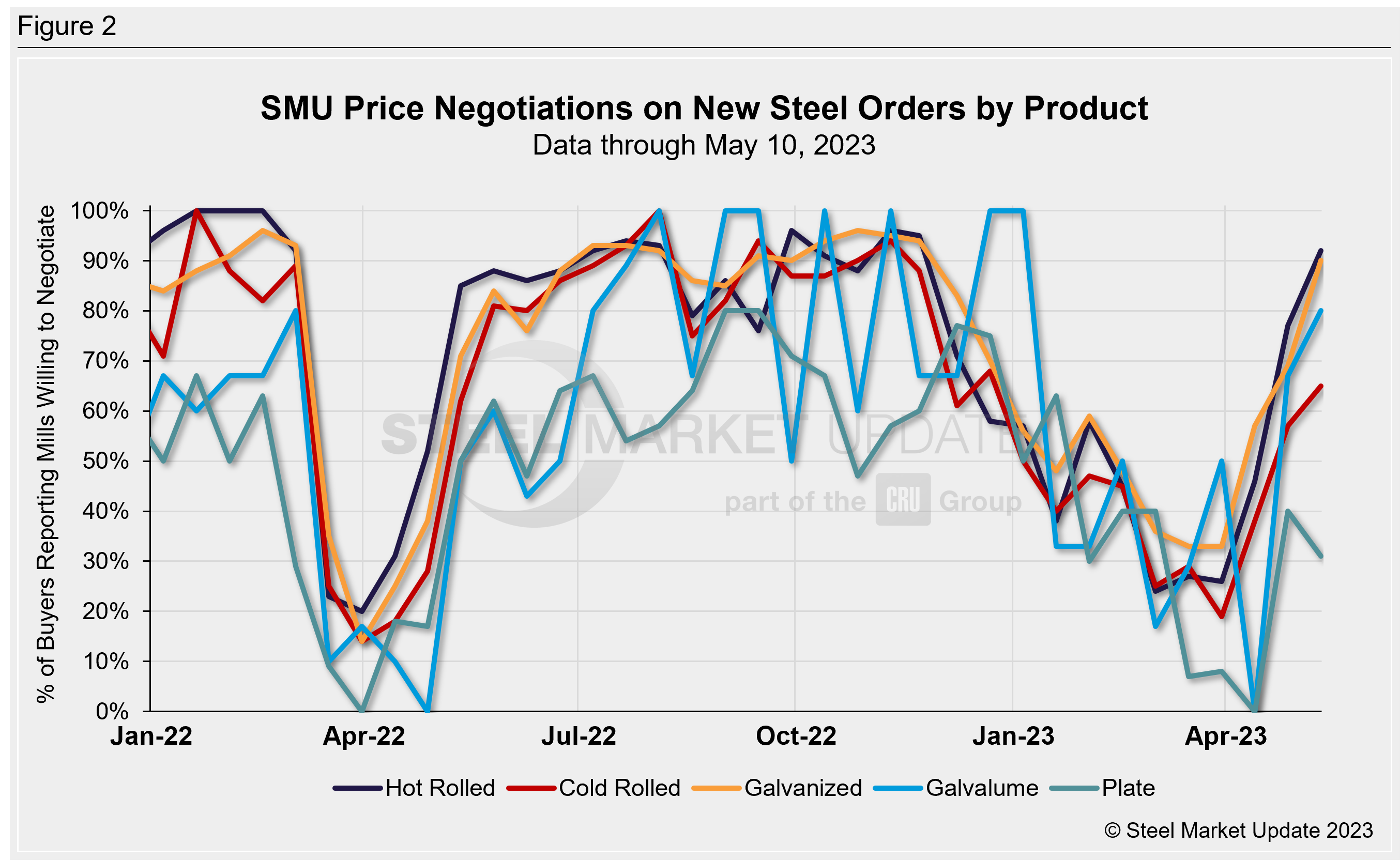

Figure 2 below shows negotiation rates by product. Hot rolled jumped to 92% of buyers reporting mills more willing to negotiate lower, up 15 percentage points from our last market check two weeks ago. Value-added sheet products trended in the same direction as HR. Cold rolled stood at 65%, up 8 percentage points; galvanized at 90% (+21); and Galvalume at 80% (+13). Recall that Galvalume can be more volatile because we have fewer survey participants there.

Plate did not follow sheet’s lead. Only 31% of survey respondents said plate mills were negotiating lower prices, down 9 percentage points vs. two weeks earlier.

Note: SMU surveys active steel buyers every other week to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.

By Ethan Bernard, ethan@steelmarketupdate.com