Market Segment

September 17, 2021

CRU Explains: China's Steel Production Cuts and How They Work

Written by CRU Americas

By CRU Analysts Kevin Bai and Zhenzhen Jiang, from CRU’s Steelmaking Raw Materials Monitor

(Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on upgrading to a Premium-level subscription, email Info@SteelMarketUpdate.com.)

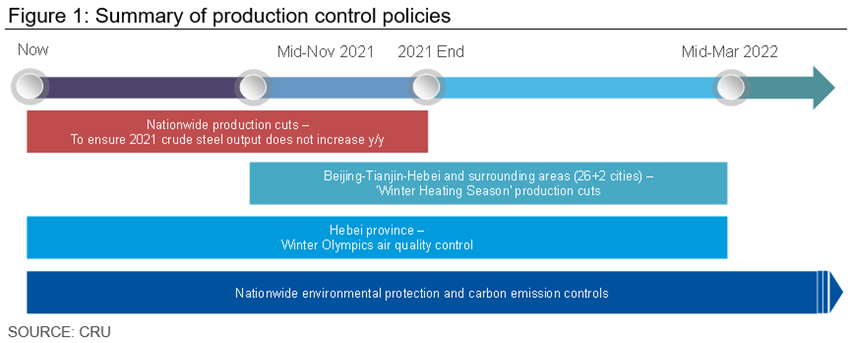

China’s steel production control measures have been heatedly discussed in the past few months. With the target of achieving flat crude steel production y/y for 2021 as a whole, provincial governments have designed regional steel production cuts through methods including electricity and energy consumption controls as well as environmental inspections to help achieve air quality improvement. Besides these cuts, new guidance has also been issued to limit steel production during the “traditional” winter heating season and during the Winter Olympics in Beijing, starting on Feb. 4. Production cut policy has also been announced by the Ministry of Environment and Ecology, the Ministry of Industry and Information Technology, and by local governments.

The underlying steel demand conditions have turned weak since the start of Q3. In order to get a better understanding of the Chinese steel market balance for the rest of this year and the start of 2022, it is crucial to understand these new production controls and estimate the impact on crude steel production as it will help not only to forecast domestic prices, but it also forms our view on prices in the wider Asian region.

There are Four Types of Production Controls

Discussion over China’s production control measures has become heated since June, but the various measures, their magnitude and timing of implementation have been confusing to many people in the market. So let’s start with some useful background of these measures:

- The nationwide 2021 production cuts (now-end 2021) were first announced by the Ministry of Industry and Information Technology at end-2020 as part of China’s new decarbonization policy. But actually, this target was only brought into focus in mid-June this year, which is one reason Chinese crude steel production increased enough to reach new record levels in Q2. Provincial governments started to outline detailed implementation plans following Beijing’s order, to ensure that crude steel production in H2 would be lower than in the second half of 2020.

- The Winter Heating Season (WHS) production cuts (Nov 15, 2021-March 15, 2022) are returning this year. The central government started this policy in 2017 in a bid to fight pollution during the six-month winter period in “2+26 cities” (located in Beijing-Tianjin-Hebei surrounding areas, Yangtze River Delta and Fenwei Plain with heavy pollution problems.) The restrictions initially forced steelmakers to reduce production to certain target levels, but then shifted to focusing on reducing emissions rather than production. With more mills meeting the ultra-low emission standards, air quality has improved significantly in China in recent years.

- The Winter Olympic Games are going to be held in Beijing from Feb. 4 to Feb. 20 while the production restrictions will last from this August until next mid-March. Given past experiences for such important events, people have expected some further production restrictions to take place in the areas surrounding Beijing, mostly Hebei, during this period in order to improve air quality. As expected, we have already gotten some details of the policy. Please read on for more details.

- Lastly, we still have general national environmental protection and carbon emission controls in place, in order to help achieve a carbon emissions peak for the steel industry in 2025. It is clearly not an easy task. We expect ongoing measures to take place in the medium term to ensure such a goal can be met.

To sum up, the infographic below briefly demonstrates the timeline of the above-mentioned measures and tries to answer three key questions:

- What is the duration of these policies?

- What are the targets of these policies?

- Which regions will these policies cover?

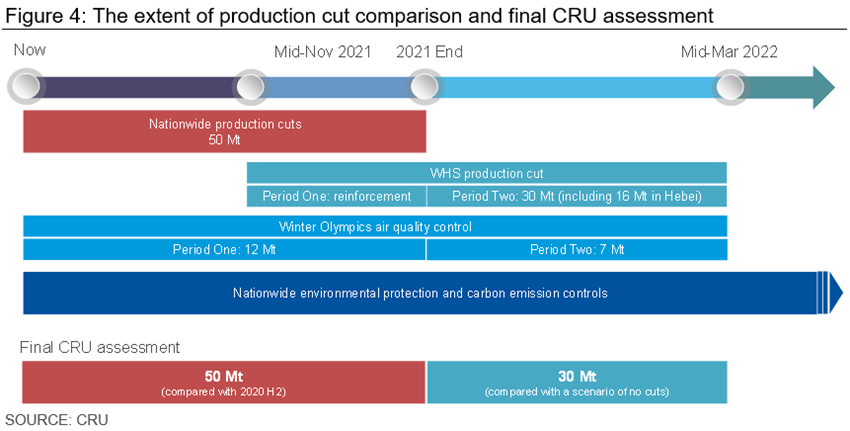

Various production restrictions have tightened the steel supply. Below is some of the information we collected from market sources, which helped us quantitatively understand the extent of the supply tightness.

The Nationwide 2021 Production Cut

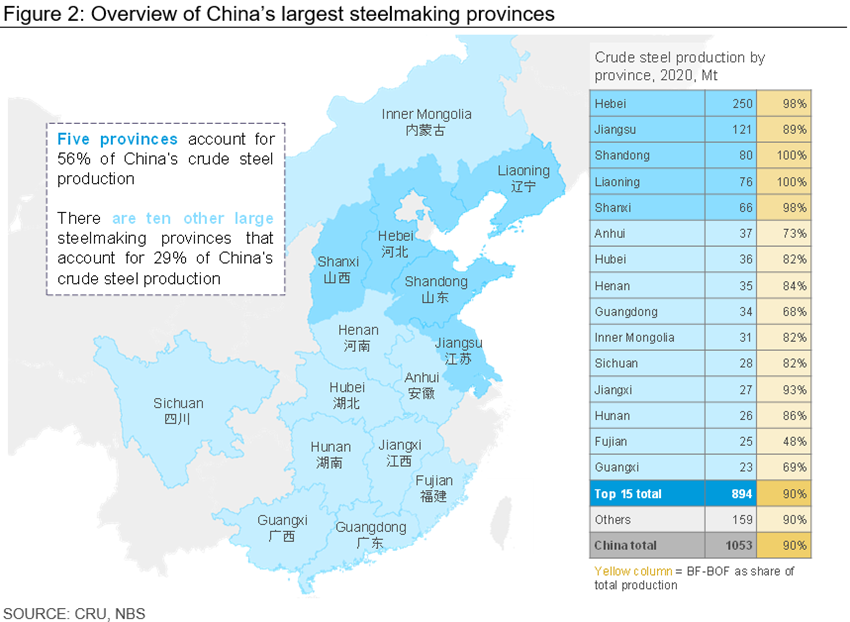

In our previous Insight, we mentioned that provinces including Jiangsu, Shandong, Anhui, Guangdong, Hebei, Liaoning, etc., have joined the group of provinces that need to cut steel production in 2021 to ensure it does not increase y/y. Meanwhile, production cuts have also started or have been under discussion at a few major steelmaking groups including Shougang in Hebei province, Ansteel and Benxi Iron & Steel in Liaoning province, and Baotou Iron & Steel in Inner Mongolia.

In order to ensure compliance by steelmakers, the government has now implemented the following control measures:

- The Ministry of Ecology and Environment has periodically sent environmental inspection groups since 2016 to ensure industrial sectors are following government requirements. A round of inspection will usually last for a month and industrial producers, including steel mills, that cause more pollution, are required to stop operating until pollution control measures are strictly enforced. Four batches of environmental inspectors have been sent out from April to September this year. In 2021, these inspections frequently have been carried out and caused more disruptions at steel mills than in previous years, especially in the past few months.

- Electricity shortage and energy consumption control. Industrial producers, including steel plants, have been required to curtail their power usage, mostly by cutting production, in provinces including Guangdong, Zhejiang, Sichuan, and Guizhou during the summer period to ensure households get enough power supply. Apart from the usual curtailment, this year in particular, local governments in Guangxi and Jiangsu provinces also ordered mills with high energy consumption to cut production to meet the annual energy conservation target.

According to our prior analysis, the estimated total amount of production lost in H2 this year compared with 2020 H2 would be 48 Mt. After collecting more information, we now expect that a total of 50 Mt y/y of production will be lost from provinces excluding Hebei. Hebei’s target of cutting 20 Mt y/y for 2021 H2 looks ambitious, and we currently do not believe it will be successfully achieved because the province would need the cuts to be even stricter than today to reach such a target. If they do manage to reduce production by that amount, the total production cuts in the entire country in 2021 H2 will be as much as 70 Mt y/y, which will more than offset the 64 Mt y/y increase in 2021 H1, meaning that the target of not increasing steel production for the full year 2021 will be met. However, this is not our base case and we still expect China’s crude steel production to rise in 2021 as a whole.

The Winter Heating Season (WHS) Production Cuts

After four WHS production cutback policies implemented since 2017, China’s air quality has improved remarkably. Although the restrictions have been gradually loosening in the past few years with more mills meeting emissions standards, we expect the government to take the 2021/2022 WHS cuts more seriously, mainly because the 2021 Q4 cuts will be crucial to reaching the overarching goal of flat steel production in 2021. According to the recent government policy draft, the WHS cut this year will still include “2+26 cities” surrounding the Beijing-Tianjin-Hebei region while the implementation period is split into two parts:

- Period One starts from mid-November to end-December, requiring related cities to finish their annual reduction in crude steel production. Because this period overlaps with the nationwide production cut policy in 2021, Period One can also be considered as a reinforcement measure for the nationwide policy.

- Period Two starts from January to mid-March of 2022, requiring the “2+26 cities” to cut their steel production by 30% to reduce emissions and pollution. We expect a steel production to be 30 Mt lower compared with a scenario where there is no WHS policy in place. The production losses during Period Two are split into 16 Mt and 14 Mt reductions in Hebei province and the other regions, respectively.

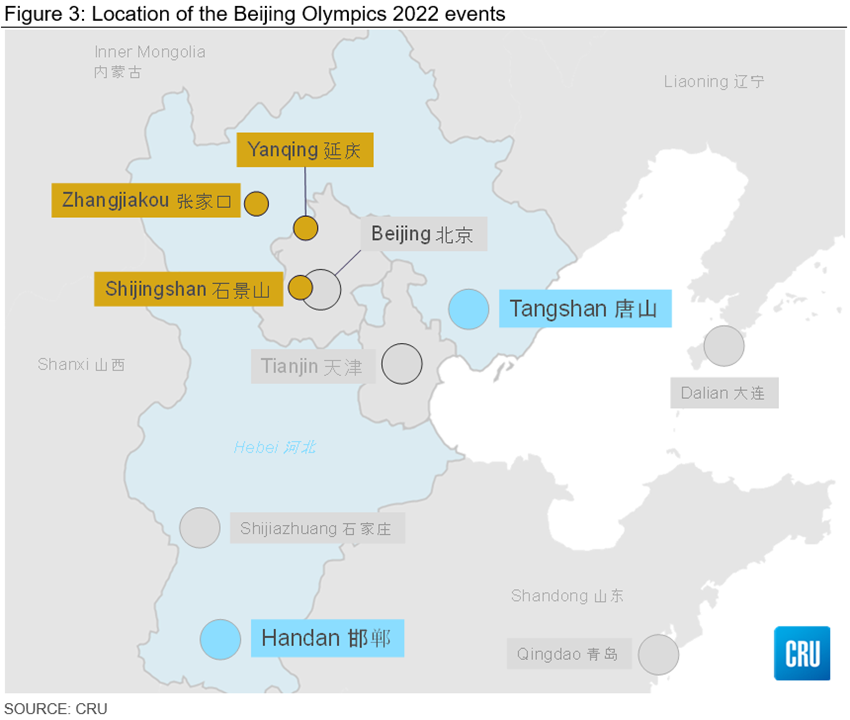

The Production Cut for the 2022 Winter Olympic Games in Beijing

The 2022 Winter Olympics Games in Beijing are expected to take place in three regions, Shijingshan and Yanqing Districts in Beijing and Zhangjiakou District in Hebei Province. While we do not expect steel demand to be significantly reduced as most construction works have already been finished, the local government of Hebei has required local industrial plants to cut output in order to ensure air quality during the global event.

This restriction also has two periods. Period One started already on Aug. 1 and lasts until Jan. 27. Period Two starts on Jan. 28 and is expected to remain until mid-March. This policy reiterated the short-term goal to cut crude steel production by 20 Mt in Hebei, including 12 Mt in Tangshan City alone, for 2021 H2. Moreover, steel mills in Tangshan are categorised into four groups and mills in each category are subject to 0%, 30%, 50% and 100% cuts in terms of blast furnace production, respectively. According to the policy released by the Tangshan government, we estimate that 12 Mt and 7 Mt of crude steel production will be lost in 2021 H2 and 2022 Q1, respectively. Interestingly, the 12 Mt cut for Tangshan in 2021 H2 is in line with the target mentioned earlier.

What Will the Impact be on Crude Steel Production?

The figure below summarizes the impact of the above-mentioned production restrictions.

Comparing production in 2021 with 2020, a 70 Mt y/y reduction in H2 will be challenging to meet, though we believe a 50 Mt cut is more realistic considering Hebei’s 20 Mt cut being difficult to achieve. Besides, higher cuts could lead to a supply shortage and rising steel prices, which are not part of the government’s targets. Thus, our base case remains at 50 Mt y/y reduction in 2021 H2. For 2022 Q1, the strictest restriction is the WHS cut, with wider coverage and larger impact, that will total 30 Mt of production loss.

Much tighter supply until mid-March 2022 can provide strength to mills’ profitability, especially in seasonally strong demand months such as September and October. However, prices and margins may be exposed to downside risks as demand slows during the winter and the Chinese New Year holidays. Expected falls in production costs may also point to a lower base even with profitability staying healthy. One key commodity to watch here is Chinese domestic coking coal, for which prices have skyrocketed in the past few weeks. However, prices are unlikely to remain at these high levels, bringing down the costs of steel production towards year-end.

Further ahead, we expect the supply control to continue and become a new normal in the medium-term on the back of the decarbonization path for the Chinese steel industry. Our analysis shows that the extent of the cuts we have highlighted here will lead to a sharp fall in crude steel production in 2021 H2. It is possible that production drops to the level that results in Chinese crude steel production falling in 2021 as a whole, but this is not our base case. The most likely scenario is that China’s crude steel production in 2021 will end up rising by 14 Mt compared with 2020, a 1% increase y/y.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com