Market Data

September 1, 2021

Steel Mill Lead Times: Predictions of a Trend Change Premature

Written by Tim Triplett

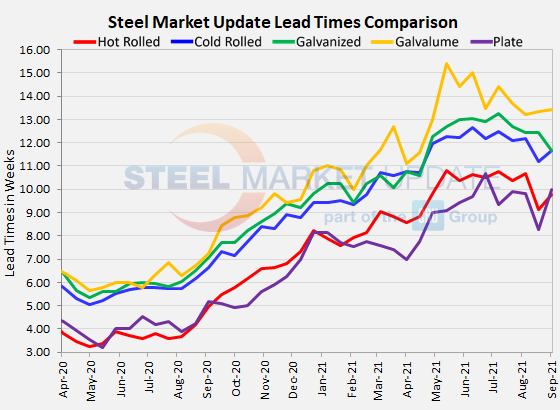

In mid-August, when lead times registered their first significant decline of the year, some interpreted it as a sign the pendulum had finally begun to swing the other way. Lead times have long been expected to shorten as the mills’ ability to supply the market finally catches up with demand. But any predictions of a trend change appear premature, as Steel Market Update’s latest data shows lead times extending again by a half week or more on hot rolled, cold rolled and plate. Lead times on coated products were the exception.

Until last month, lead times for spot orders of steel had extended continuously since the spring of 2020 when the market hit bottom due to the pandemic. The average lead time for hot rolled was a quick 3.25 weeks in late April 2020.

SMU’s check of the market this week shows the average lead time for spot orders of hot rolled at 9.79 weeks, extending from 9.15 weeks in the Aug. 19 survey. Cold rolled lead times moved out to 11.67 from 11.17 weeks in the same period. The average Galvalume lead time inched up to 13.44 weeks.

Average plate lead times also extended significantly in the latest data to 10.00 weeks from 8.29 weeks last month.

Galvanized lead times did not follow the same pattern. At an average of 11.67 weeks, lead times for delivery of galvanized products declined from 12.43 weeks.

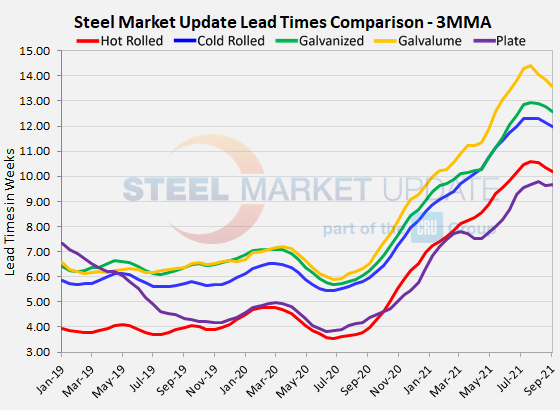

Three-month moving averages, which smooth out the weekly volatility of the lead times data, shortened for all products despite the small increase seen this week. The 3MMA for hot rolled lead times now averages 10.20 weeks, cold rolled 11.96 weeks, galvanized 12579 weeks, and Galvalume 13.59 weeks. Plate’s 3MMA was about the same at 9.67 weeks.

Lead times tend to be a leading indicator of steel prices. The shorter the lead times, the less busy the mills and the more likely they are to discount prices to win orders. SMU’s latest data shows no clear trend for lead times, which remain highly extended compared with historical averages.

Negotiations

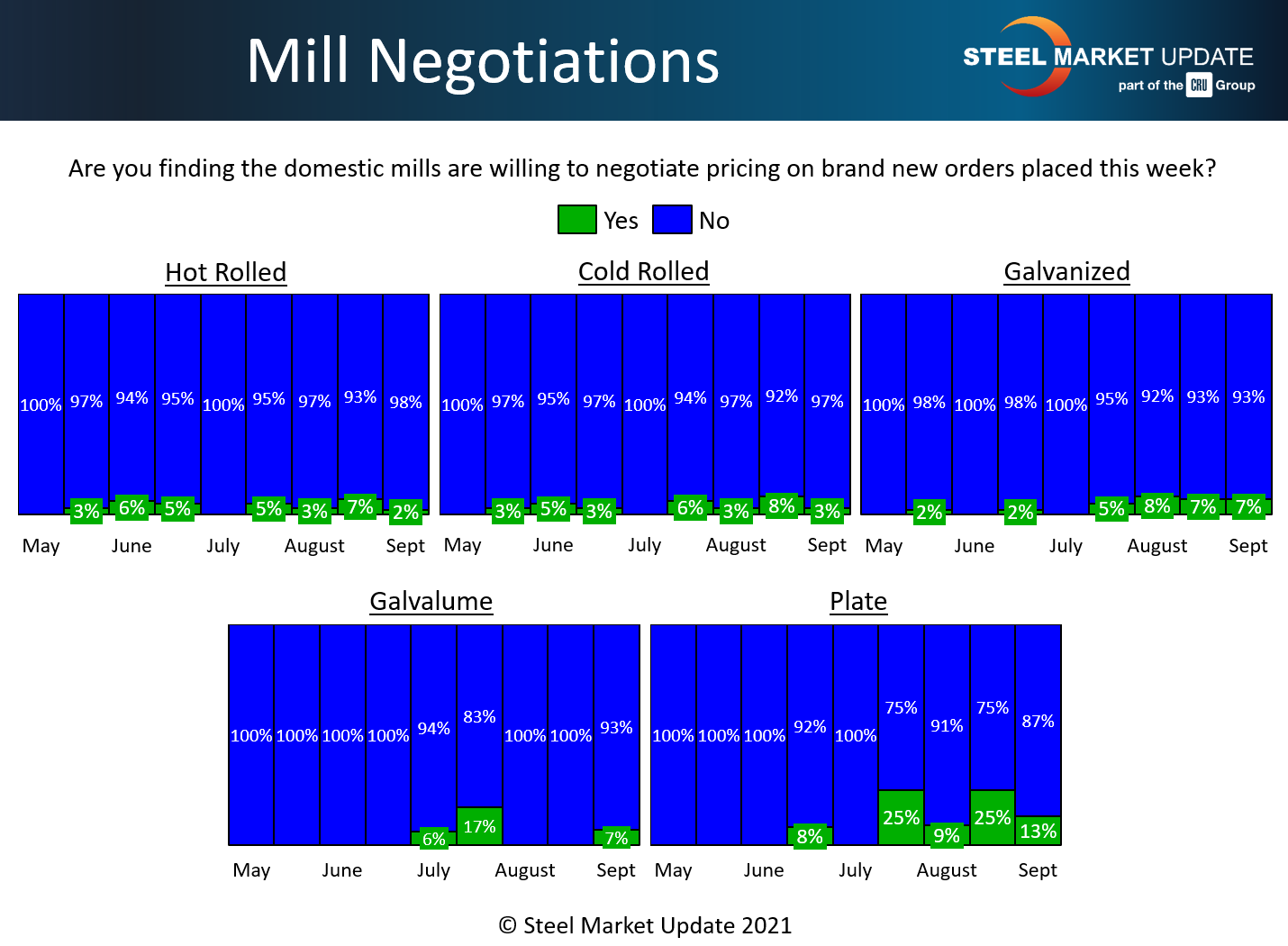

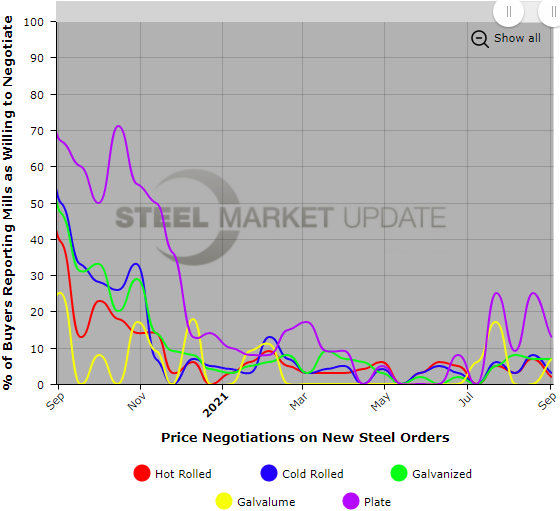

No significant change to report in the tone of negotiations between steelmakers and steel buyers. The mills remain in firm control of price negotiations, as they can easily sell all the spot tons they have to offer at their asking price.

Asked if mills are open to discussing price, from 93-98% of respondents to SMU’s survey said “no,” depending on the flat rolled product. Price talks were slightly more open in the plate market, with 13% of plate buyers reporting some room to negotiate discounts.

As one buyer commented: “Things are still very tight out on the West Coast. The Midwest folks aren’t showing much interest at all in offering spot tonnages.” Added another on the mills’ unwillingness to negotiate: “That’s fine. We’re not giving them any orders anyway, as their price is so much higher than import.”

By Tim Triplett, Tim@SteelMarketUpdate.com