Market Data

August 20, 2021

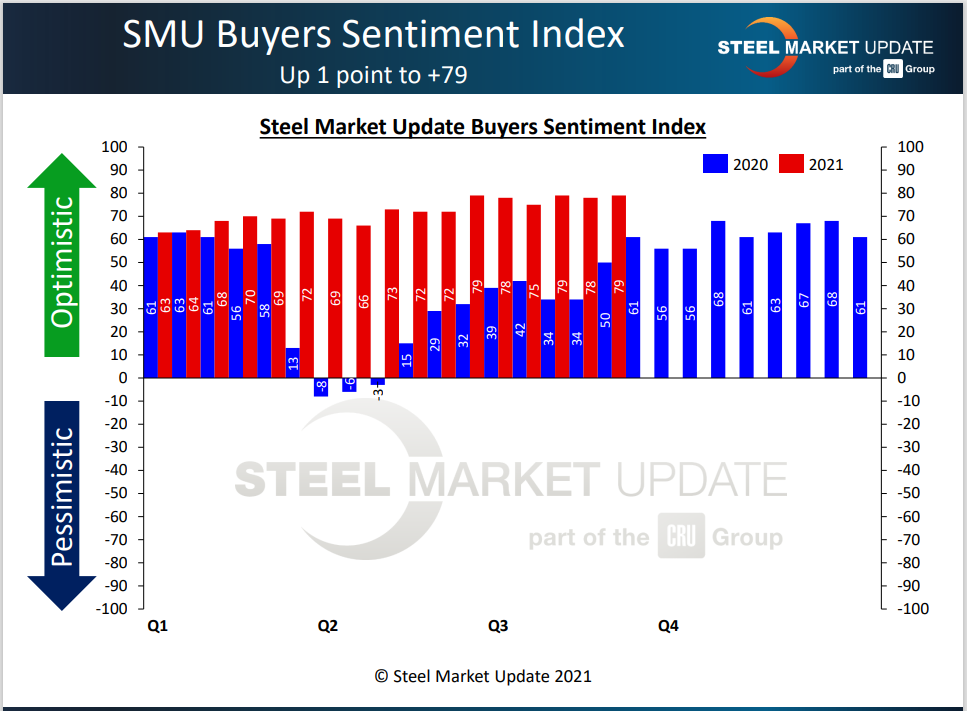

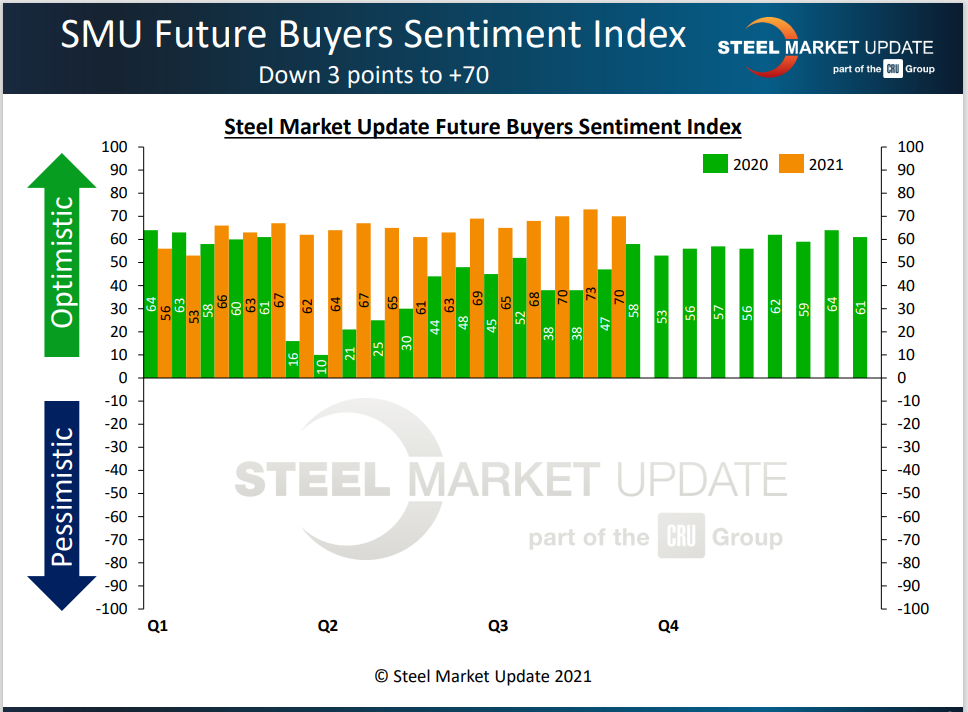

SMU Steel Buyers Sentiment: Never Been Higher

Written by Tim Triplett

If steel buyers are concerned about lead times that are beginning to shorten and price increases that are beginning to slow, there is no sign of it in this week’s Steel Buyers Sentiment readings. The Current and Future Sentiment indexes remain at or near record highs as steel producers and distributors continue to enjoy record revenues and profits.

At a reading of +79, the Current Sentiment Index is tied with the all-time high seen in mid-June and mid-July. Future Sentiment registered +70 this week, down three points from earlier this month but still not far from the historical high of +77 seen in February 2018.

Measured as a three-month moving average (3MMA) to smooth out the variability, Current Sentiment stood at +78.00 this week, the highest on record. The Future Sentiment 3MMA moved up to +69.17, its highest since February 2018.

SMU asks steel buyers every two weeks how they view their company’s chances for success in the current environment and how they view their prospects three to six months in the future. Their outlook has never been more upbeat, reflecting steel prices that have never been more elevated. The benchmark price for hot rolled steel hit a new all-time high of $1,915 per ton this week, according to SMU data.

Steel buyers’ sentiment tends to track up and down with steel prices. When steel prices take a turn – and they will at some point, say the experts, perhaps even this year – look for industry sentiment to follow suit.

What Respondents Had to Say

“Record profits month-after-month and August should be our best yet. At some point the party will be over, but not for a while longer.”

“We are virtually sold out of the inventory we have for the year at nice margins. We are concerned going into 2022 with no domestic contracts so far and a large amount of import on order for January and February to restock and start the year.”

“I am more confident that we won’t see a crash in either demand or pricing (like we did after the rallies of 2008 and 2018). That’ll keep the good times rolling well into 2022.”

“I think the year will be capped off nicely.”

“Credit and inventory costs are our biggest concerns now.”

“Will the Delta variant slow the economy? I am starting to get concerned about that now.”

“Market dynamics are changing rapidly. There’s still too much uncertainty.”

“We need the constant market manipulation to end.”

About the SMU Steel Buyers Sentiment Index

SMU Steel Buyers Sentiment Index is a measurement of the current attitude of buyers and sellers of flat-rolled steel products in North America regarding how they feel about their company’s opportunity for success in today’s market. It is a proprietary product developed by Steel Market Update for the North American steel industry.

Positive readings run from +10 to +100. A positive reading means the meter on the right-hand side of our home page will fall in the green area indicating optimistic sentiment. Negative readings run from -10 to -100. They result in the meter on our homepage trending into the red, indicating pessimistic sentiment. A reading of “0” (+/- 10) indicates a neutral sentiment (or slightly optimistic or pessimistic), which is most likely an indicator of a shift occurring in the marketplace. Sentiment is measured via Steel Market Update surveys that are conducted twice per month. We display the meter on our home page for all to see.

We currently send invitations to participate in our survey to more than 600 North American companies. Our normal response rate is 100-150 companies. Approximately 40 percent are manufacturers, 45 percent are service centers/distributors, and 15 percent are steel mills, trading companies or toll processors involved in the steel business.

Click here to view an interactive graphic of the SMU Steel Buyers Sentiment Index or the SMU Future Steel Buyers Sentiment Index.

By Tim Triplett, Tim@SteelMarketUpdate.com