Market Data

October 1, 2020

Steel Mill Lead Times: Mixed Messages

Written by Tim Triplett

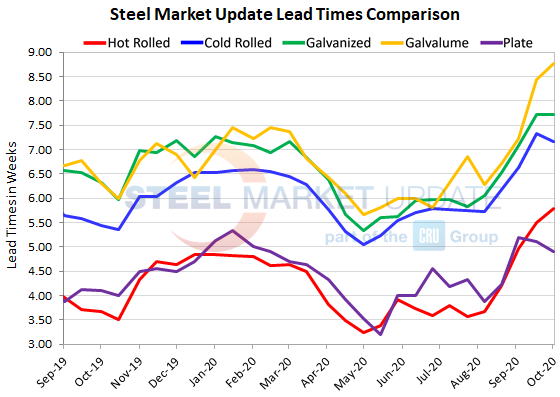

Lead times for spot orders of hot rolled and Galvalume steels continued to lengthen a bit over the past two weeks, while lead times for cold rolled, galvanized and plate products were flat to slightly lower. Lead times for hot rolled now average more than five and a half weeks, cold rolled more than seven weeks, galvanized nearly eight weeks, and Galvalume more than eight weeks. The average plate lead time has dipped below five weeks. Lead times are an indicator of steel demand—longer lead times indicate the mills have more orders to process and are less likely to negotiate on prices. The mills raised prices on both flat rolled and plate products this week, which may have an effect on lead times in the coming weeks.

According to Steel Market Update’s check of the market this week, hot rolled lead times now average 5.78 weeks, up from 5.50 two weeks ago and 4.97 weeks at this time last month. HR lead times have stretched by two and a half weeks since hitting 3.25 weeks at the low point in April.

Cold rolled lead times are at 7.17 weeks, down slightly from 7.32 in SMU’s last check of the market, but still a half week longer than at this time in early September. Cold rolled lead times are more than two weeks longer than in April.

Galvanized lead times are unchanged over the past two weeks at 7.73 weeks, up from 7.08 weeks in early September. The current average Galvalume lead time is up to 8.77 weeks, and has extended by a week and a half in just the past month as Galvalume supplies have tightened.

Plate lead times have shortened slightly in the past month to the current average of 4.91 weeks.

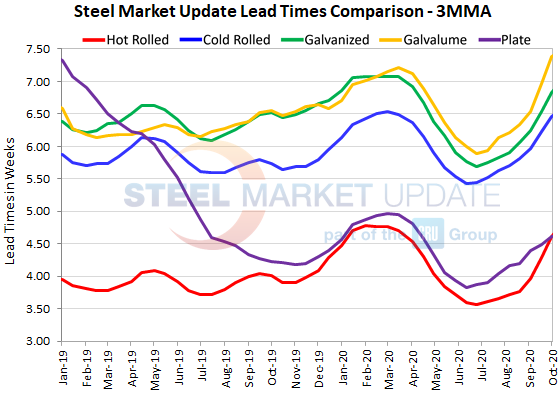

Looking at three-month moving averages, which smooth out the variability in the biweekly readings, lead times for flat rolled and plate have continued moving outward since late June. The current 3MMA for hot rolled is 4.62 weeks, cold rolled is 6.46 weeks, galvanized is 6.83 weeks, Galvalume is 7.38 weeks and plate is 4.61 weeks.

Said one respondent: “Right now some of the steel mills do not have spot tons available. Hopefully more spot tons will be available after Phase 2 at BRS is completed and the other steel mills are done with outages. Added another: “I believe Q1 will see things retrench.”

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. Our lead times are meant only to identify trends and changes in the marketplace. To see an interactive history of our Steel Mill Lead Times data, visit our website here.