Market Data

July 27, 2020

Global Steel Production Through June

Written by Peter Wright

In 12 months through June, China’s steel production exceeded one billion metric tons for the first time.

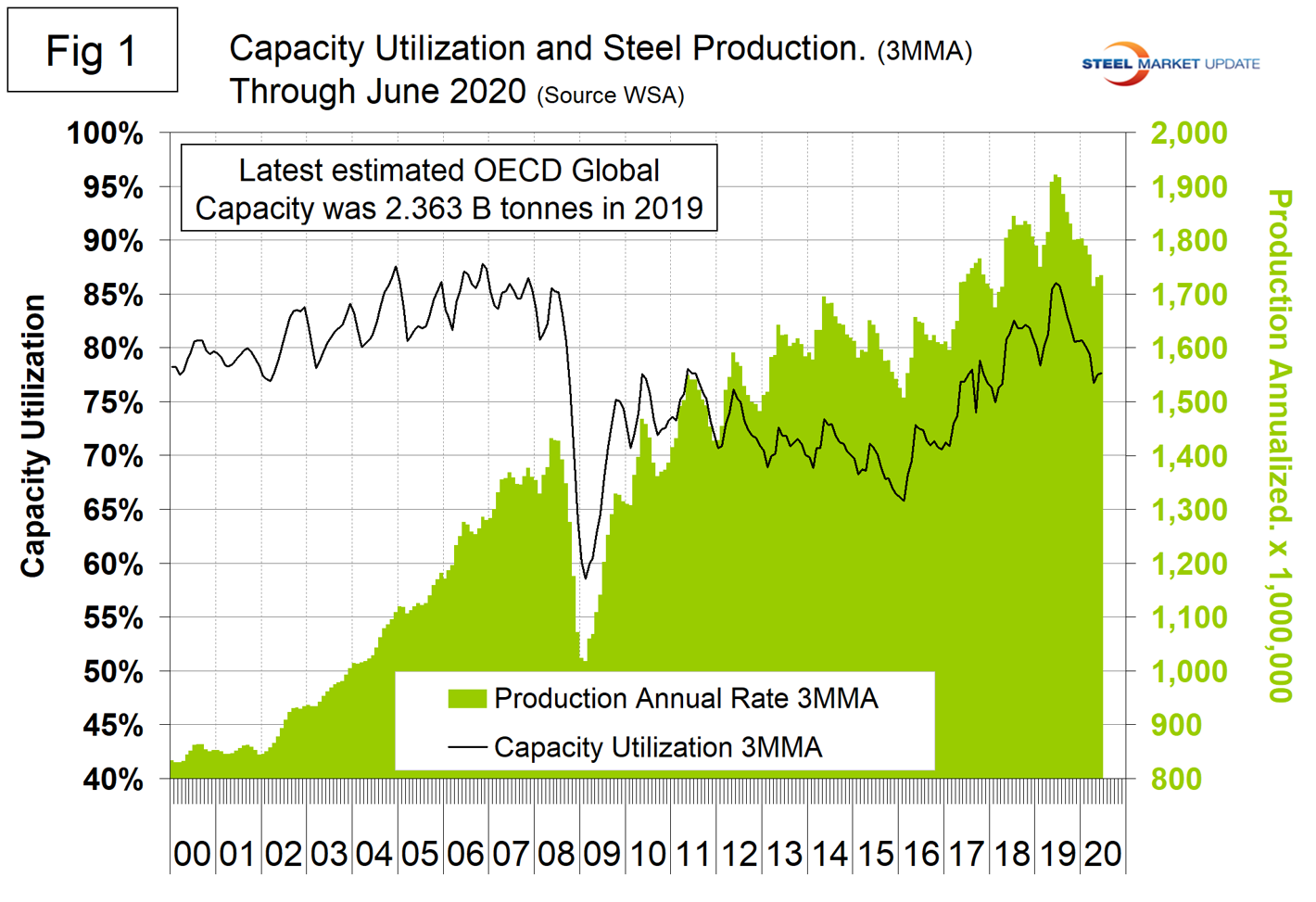

Figure 1 shows annualized monthly global steel production on a three-month moving average (3MMA) basis and capacity utilization since January 2000 based on the updated OECD capacity data. Capacity utilization in June on a 3MMA basis was 75.3 percent. On a tons-per-day basis, production in June was 4.943 million metric tons, down from June 2019’s all-time high of 5.318 million metric tons.

Figure 2 shows the year-over-year growth rate of the 3MMA of global production since January 2013. Growth in three months through June on a year-over-year basis was negative 9.7 percent, down from positive 2.3 percent in February.

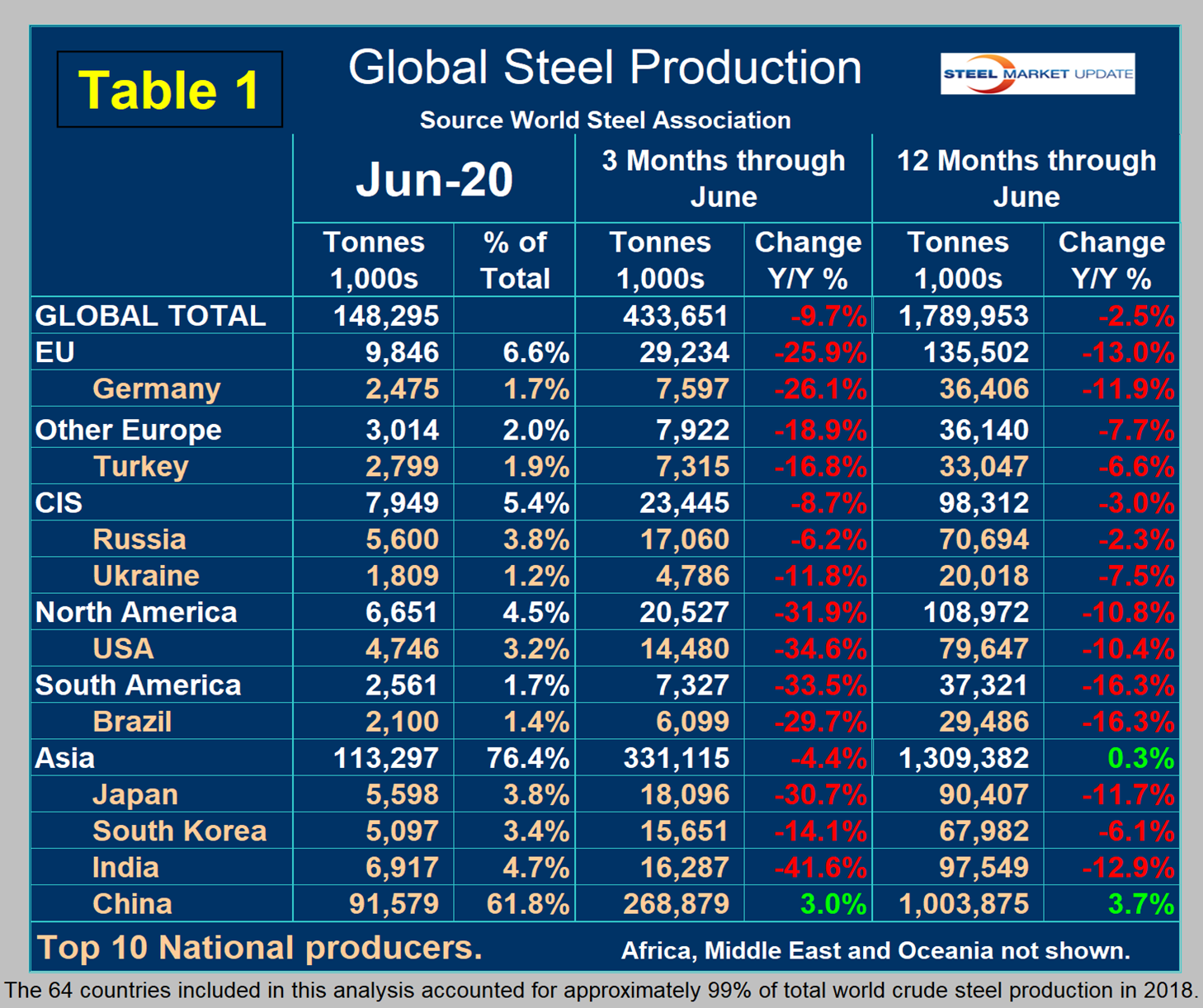

Table 1 shows global production broken down into regions, the production of the top 10 nations in the single month of June, and their share of the global total. It also shows the latest three months and 12 months of production through June with year-over-year growth rates for each period. Regions are shown in white font and individual nations in beige.

The world overall had negative growth of 9.7 percent in three months and negative 2.5 percent in 12 months through June. When the three-month growth rate is lower than the 12-month growth rate, as it was in April, May and June, we interpret this to be a sign of negative momentum. On the same basis in June, China grew by 3.0 percent and 3.7 percent, therefore also had slightly negative momentum. China was the only country to have positive growth in both three months and 12 months through June. All other countries except Russia had double-digit declines in three months, the worst case being India, down 41.6 percent. Table 1 shows that North America was down by 31.9 percent in the three months through June. Within North America, production was down by 34.6 percent in the U.S. down by 24.9 percent in Canada and down by 23.5 percent in Mexico. (Canada and Mexico are not shown in Table 1 and the North American total includes Cuba, El Salvador and Guatemala.)

In the 12 months through June, 108.9 million metric tons were produced in North America, of which 80.0 million tons were produced in the U.S., 12.0 million tons in Canada and 16.9 million tons in Mexico. Based on the new OECD data, U.S. capacity in 2019 was 109.7 million metric tons with a capacity utilization of 80.0 percent.

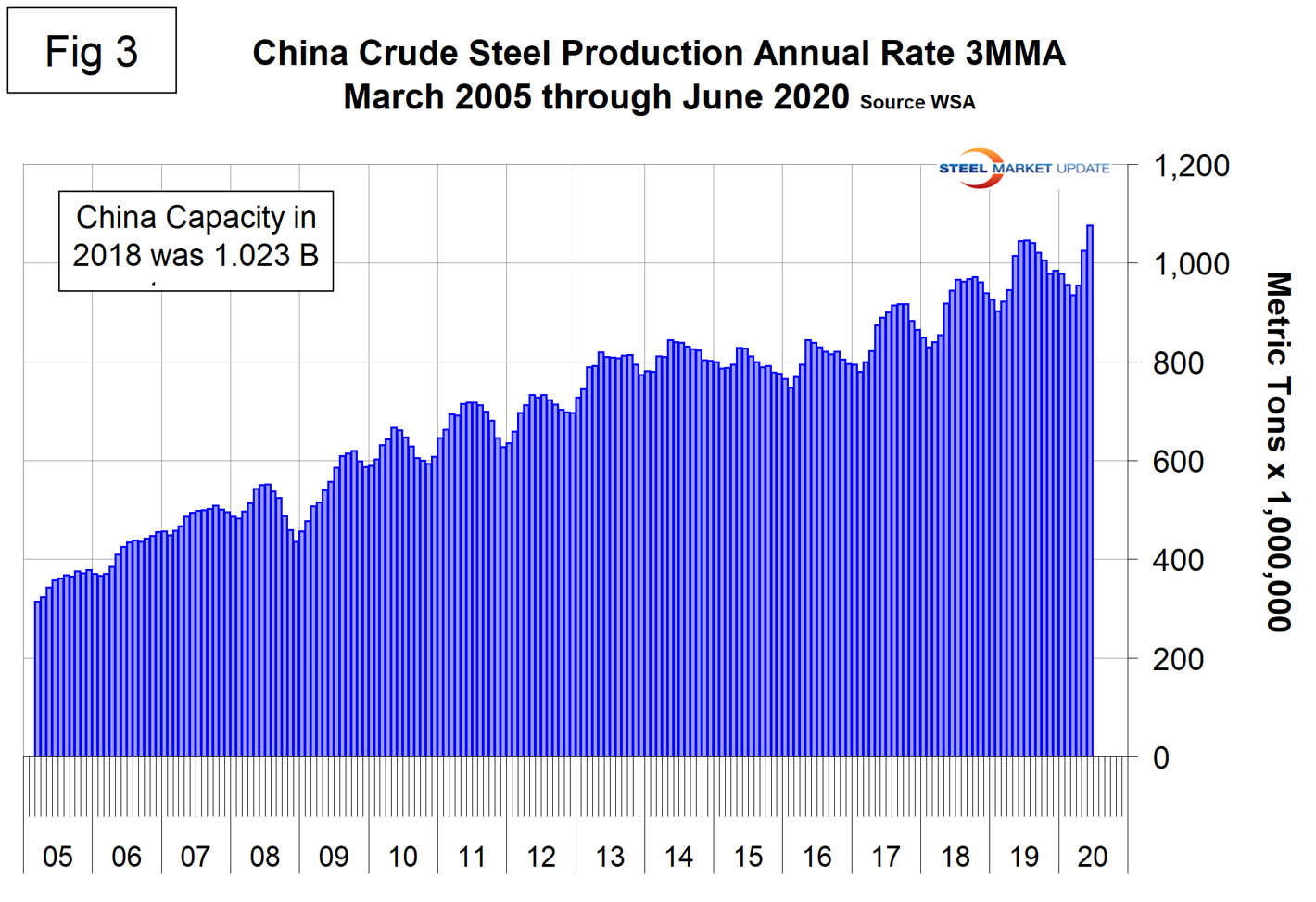

Figure 3 shows China’s production since 2005. In the single month of June, China’s steel production was at an all-time high of 3.05 million tons per day, and June was the first month ever for China’s production to exceed one billion metric tons on a rolling 12-month basis. China’s annual capacity is now 1.152 billion metric tons, a reduction from 1.215 billion tons in January 2015. June capacity utilization was 89.0 percent, which as a result of the capacity reduction and production increases was up from 67.3 percent in January 2015.

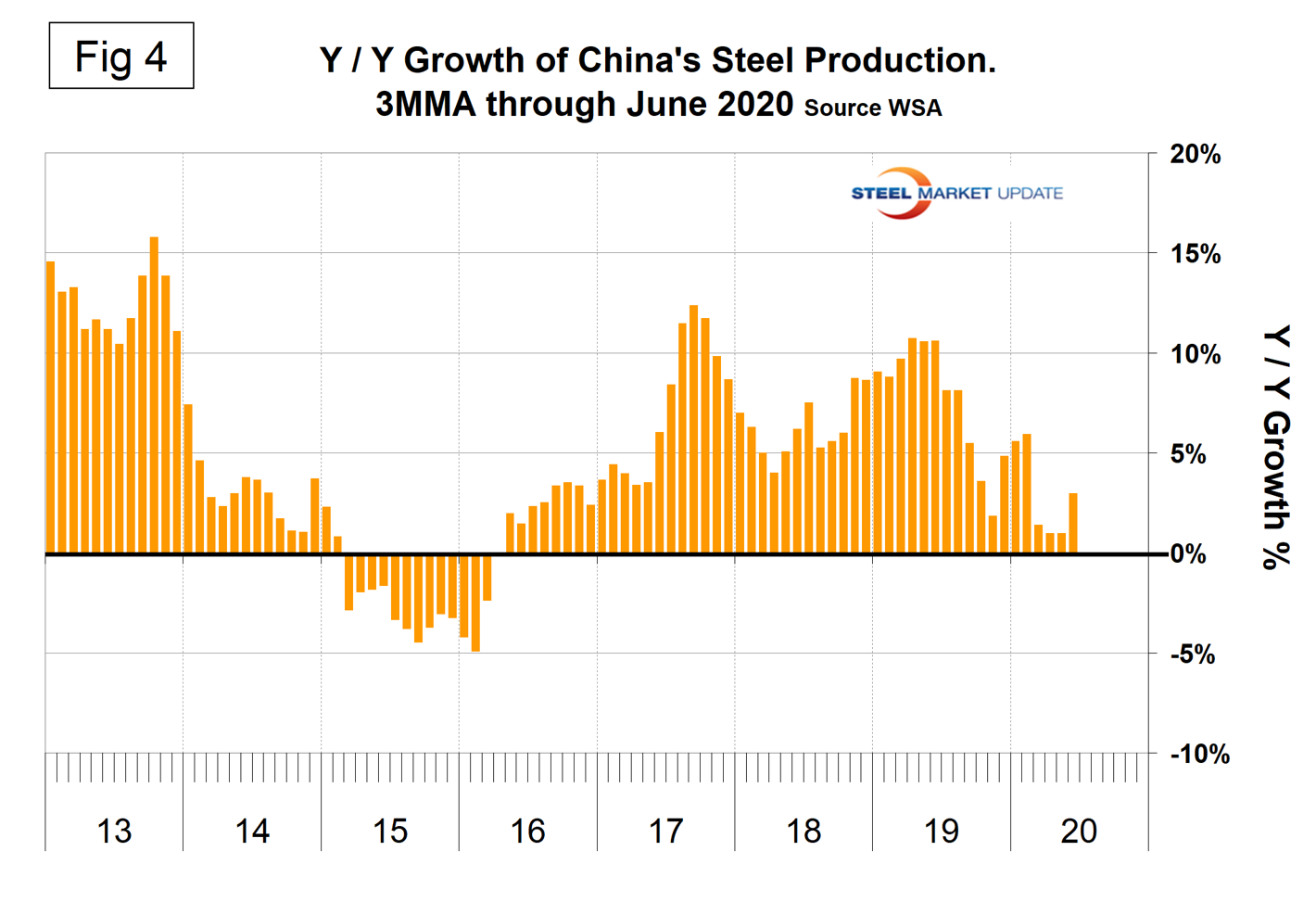

Figure 4 shows the growth of China’s steel production since March 2013 and Figure 5 shows the growth of global steel excluding China on the same scale both on a 3MMA basis. In June, the rest of the world contracted by 21.1 percent as China grew by 3.0 percent.

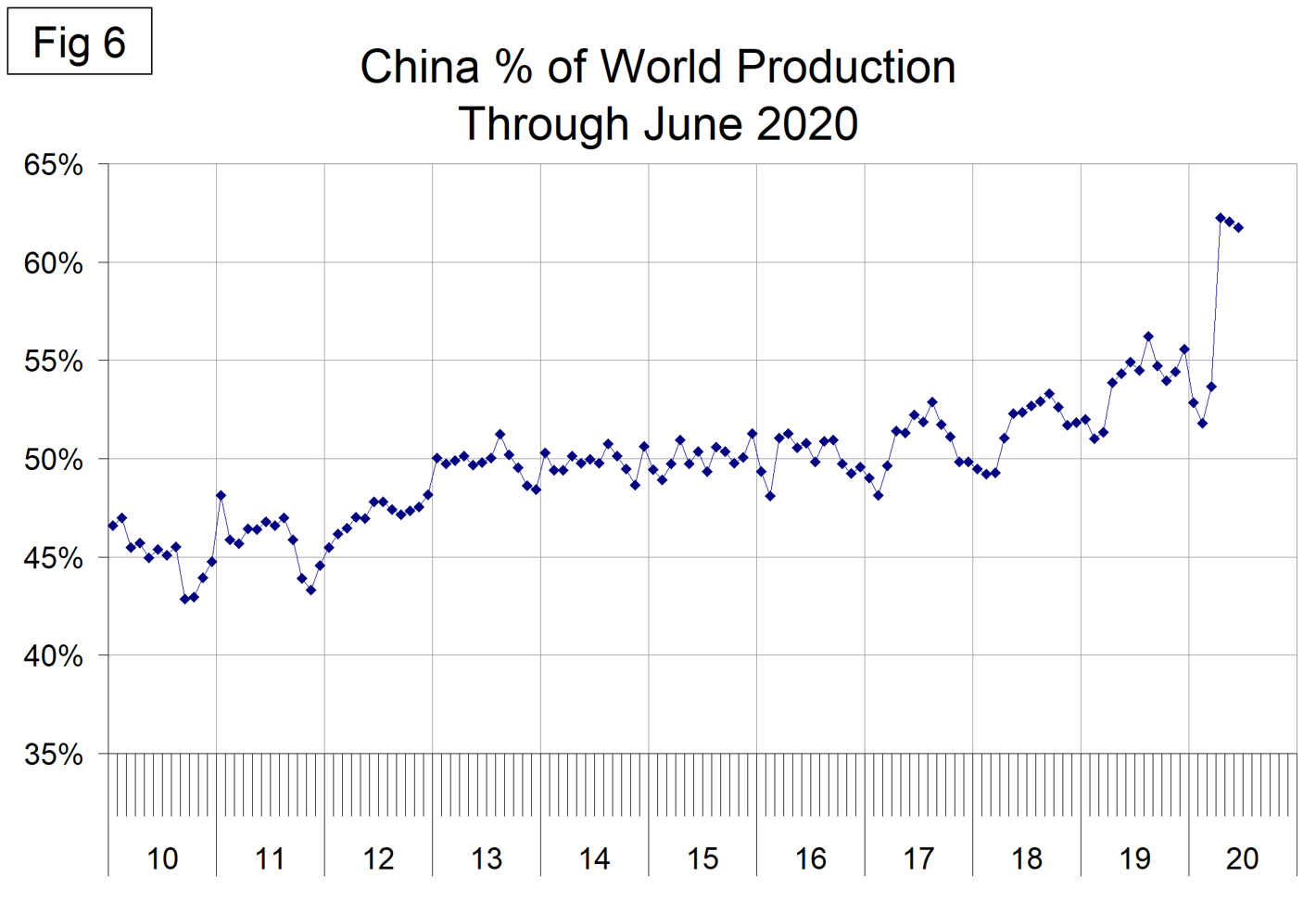

Figure 6 shows the growth of China’s share of global steel production, which in the three months April, May and June has averaged 62.0 percent.

NOTES: On June 24, 2020, the OECD released its updated report of steel production capacity by nation. “Global steelmaking capacity (in nominal crude terms) decreased from 2015 to 2018, but the latest available information (as of December 2019) suggests that capacity increased in 2019 for the first time since 2014. The OECD has revised its 2019 figures for global steelmaking capacity to 2,362.5 million metric tonnes (mmt) to incorporate new information on closures that was not previously available as well as updated information on the status of certain investment projects. Moreover, revisions to the aggregate capacity figures for the People’s Republic of China, the United States, Mexico, Japan, Korea, and several other economies’ data contributed to the upward revision for 2019 and previous years. The net capacity change in 2019, taking into account new capacity additions and closures, represents a 1.5 percent increase from the level at the end of 2018.”

The World Steel Association released their short range forecast on June 4, 2020. They anticipate that global production will be down by 6.4 percent in 2020 and up by 3.8 percent in 2021. On the same basis, North America will be down by 20.0 percent and up by 6.2 percent.

The WSA represents approximately 85 percent of the world’s steel production, including over 160 steel producers, national and regional steel industry associations and steel research institutes. (Note at the bottom of Table 1 WSA says this represents 99 percent of steel production, so presumably there are reports of production by countries that include nonmembers.) The OECD has taken over responsibility for tracking global steel capacity and their latest update was for 2019, released in June 2020.