Market Data

July 23, 2020

Steel Mill Negotiations: Buyers Have Upper Hand

Written by Tim Triplett

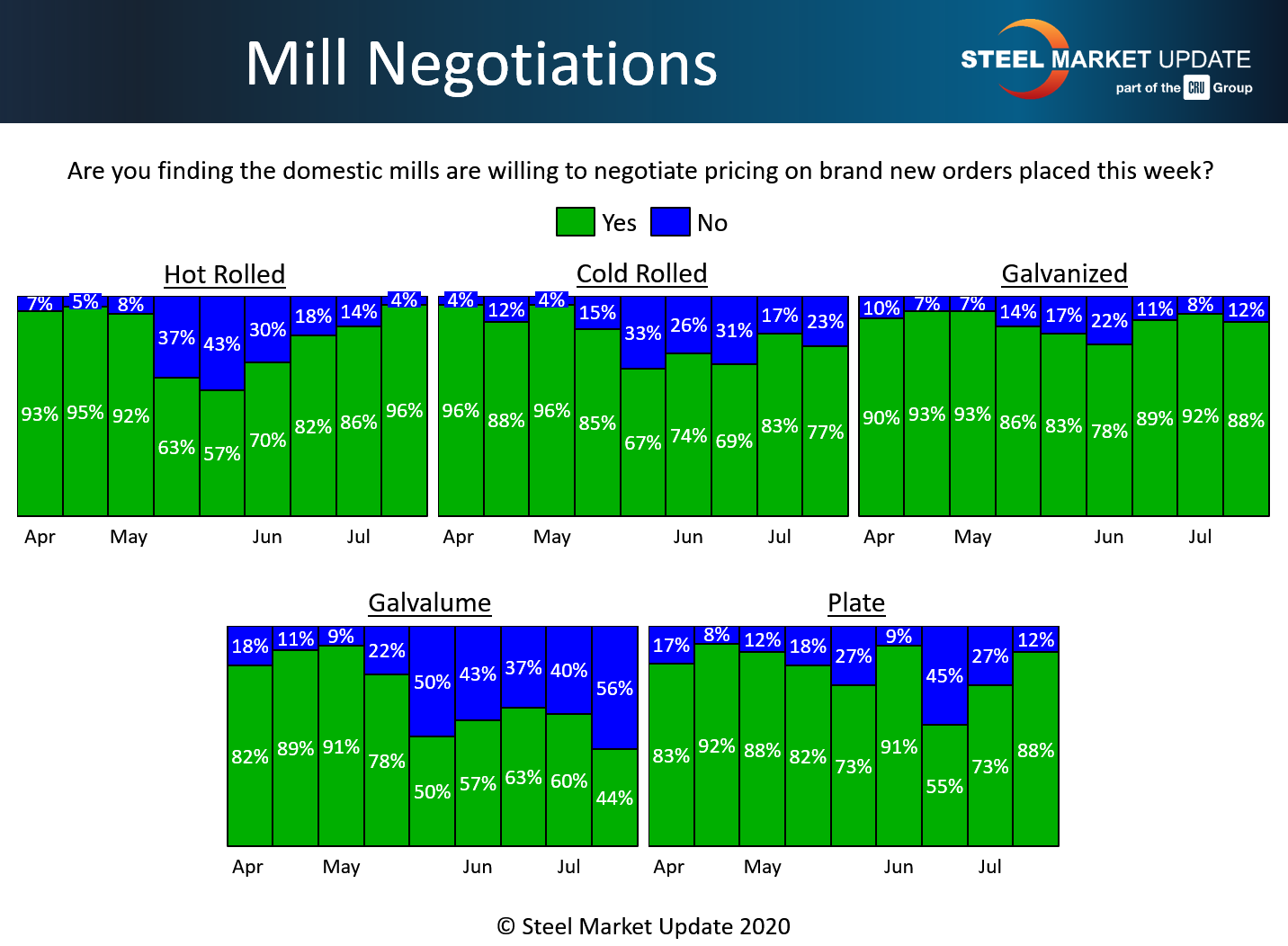

Steel buyers clearly have the upper hand in negotiations with steel makers given the challenging market conditions from the virus, with overwhelming percentages of those responding to Steel Market Update’s questionnaire this week reporting that the mills are open to price negotiations to win orders.

Nearly all the hot rolled buyers (96 percent) said the mills are open to price talks, while just 4 percent said the mills are standing firm on HR prices. That’s up 10 points from just two weeks.

In the cold rolled segment, 77 percent reported the mills willing to talk price, down slightly from 83 percent two weeks ago.

In galvanized, 88 percent reported the mills open to discounting prices, a slight decrease from 92 percent in SMU’s last canvass of the market. About 44 percent found the mills willing to compromise on Galvalume prices this week.

Negotiations are common in the plate market, where 88 percent said the mills are now willing to bargain to capture the sale, while just 12 percent reported the mills saying no to discounts. That’s up from 73 percent who said the mills were talking price two weeks ago.

Benchmark hot rolled steel prices have declined by about $120 per ton since before the coronavirus and now average $460 per ton, based on SMU’s latest canvass of the market. Cold rolled and galvanized prices declined by a further $10 per ton. Integrated mills announced a $40 per ton price increase this week in hopes of bringing the downtrend to an end.

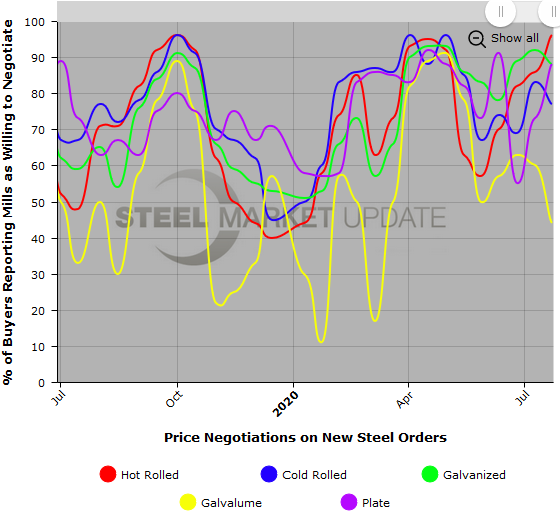

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data (second example below), visit our website here.