Overseas

July 14, 2020

CRU: Long, Slow Recovery Ahead for Steel Sheet Demand

Written by James Campbell

By CRU Principal Analyst James Campbell, from CRU’s Steel Sheet Products Market Outlook

Sheet demand collapsed in 2020 Q2 to the lowest level in a decade. As lockdowns eased in May, manufacturing activity improved, and prices increased in most regions. Global sheet demand is expected to improve in 2020 Q3 and accelerate in 2021. However, output will be lower than pre-Covid levels. Outside of China, demand destruction caused by the impact of Covid-19 means we have lost four years of growth compared to our forecast a year ago and two years of growth compared to our January forecast. With demand weaker, some of the new crude steel capacity planned during the 2017-2018 boom is unlikely to be needed in the next two to three years, especially as there are significant risks to the downside.

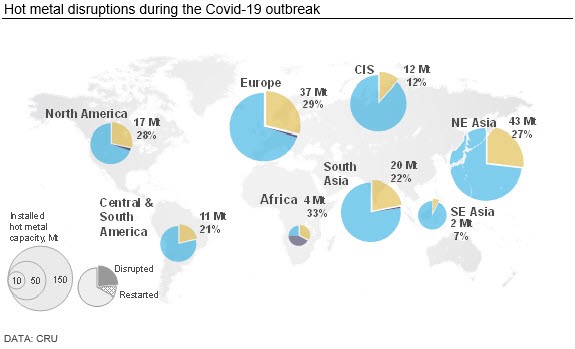

Demand Collapsed in Q2…

Sheet demand collapsed in 2020 Q2 to the lowest level in a decade. With demand for steel poor, prices fell and margins collapsed, forcing producers around the world to cut supply.

Steel sheet demand collapsed by 17 percent q/q in 2020 Q2 as country after country implemented lockdowns to combat Covid-19. Covid-19 wiped out the equivalent of a decade of global growth. This resulted in lower capacity utilization and, as producers competed for what demand remained, they cut prices. Falls were greatest in Asia and the U.S., but drifted down slowly in Europe.

Margins had only just begun to improve from the 2019 Q4 low when Covid-19 hit and reversed this trend. Margins fell in all regions in 2020 H1, with Europe and the U.S. affected more than China. The low margins on offer combined with very limited sales opportunities, forcing producers to idle bast furnaces across the world. Disruptions have been greatest in regions most reliant on automotive demand.

…But as Lockdowns Eased, Activity and Prices Improved

Prices increased in most regions from May as lockdowns eased and manufacturing activity improved, including in the hard-hit auto sector.

After hitting a low in February, Chinese manufacturing activity improved in March. Outside of China, the Covid-19 outbreak accelerated and lockdowns began, driving manufacturing activity to a low in April. As lockdowns eased, activity improved during May in the U.S. and Europe, but at a weaker pace than seen in China. There is clearly no “one size fits all” recovery from the lockdown activity low.

The automotive industry has been one of the sectors hit hardest by the outbreak. Chinese auto production fell by 81 percent y/y in February, but the recovery in China was quick. Output was just -0.7 percent lower y/y in April and grew +9.1 percent y/y in May. Auto output in Europe and the U.S. was hit harder by the lockdown, with cuts of over 95 percent in April. Production outside of China has restarted as lockdowns are eased, but in May was still -70 to -75 percent lower y/y in Europe and the U.S.

Prices began to rise in May as lockdowns outside of China started to ease, though Europe remains an outlier. Euro prices continued to fall throughout June, by which time most markets were around 10 percent lower than the start of 2020.

The Economic Outlook Has Weakened Since April

The economic outlook has weakened as Covid-19 has spread. Global sheet demand is expected to improve in 2020 Q3 and accelerate in 2021, but output will be lower than pre-Covid-19.

We have made further downgrades to IP and GDP in 2020 for Europe and the U.S., but growth in China has been revised up slightly to reflect the economic stimulus. Growth is expected to be stronger y/y in 2021 and 2022, but from a lower base.

Global IP is forecast to fall by -5.7 percent y/y in 2020 and GDP by -4.5 percent y/y. The global auto sector that is so critical to sheet demand in many markets is forecast to fall by around 20 percent y/y in 2020. This compares to a forecast of -9 percent y/y in our previous forecast; the impact of Covid‑19 has been far greater than anyone expected only three months ago. Construction is expected to be less affected, although with some variation between countries and not without risk. There are concerns demand from new projects many not be able to replace demand from existing projects later in 2020.

As the recovery takes hold in 2021, global IP and GDP are set to rise by +6.9 percent y/y and

+6.6 percent y/y, respectively. Even so, there is a loss of output compared to our last pre-Covid forecast in January. Auto production is forecast to be below peak levels in many regions until 2023, and longer in Western Europe and the U.S.

CRU Expects the Recovery to Begin in 2020 Q3

Sheet demand will improve in 2020 Q3, but a recovery will take time and the shape of the recovery is not the same in every region.

The global demand low is expected in 2020 Q2. Quarterly growth is expected in 2020 Q3 and Q4 but global demand will still be weaker y/y. Following a fall of 14 percent in 2020, sheet demand growth is expected to peak in 2021 at around 10 percent y/y. However, returning to the record level of 2019 sheet demand will take time; our current forecast points to this happening in 2022 for HR flat products. Downstream sheet products will take the longest to recover, with 2019 levels not returning until 2022 Q4.

Demand Has Been Permanently Destroyed…

There was a permanent loss of sheet demand outside of China after the global financial crisis. We expect a repeat of this from the “Covid crash.” Our current forecast suggests the level of demand destruction from Covid-19 will be greater than the impact of the GFC. However, some of this may be due to the trade war between the U.S. and China, and there are big variations between regions. The situation in China is different. China has a history of using stimulus to maintain demand momentum. 2020 is no different but growth in the country was already slowing, so any demand borrowed from the future may make life difficult for domestic producers in the medium-term.

…Meaning Some New Capacity Planned is Not Needed

Outside of China, demand destruction caused by the impact of Covid-19 means we have lost four years of growth compared to our forecast a year ago and two years of growth compared to our January forecast. In our July 2019 forecast, we expected sheet demand in 2020 to reach 435 Mt for the world excluding China. This is a similar level of demand to our current forecast for 2024; we have lost four years of growth compared to expectations a year ago.

With demand weaker, some of the new crude steel capacity planned during the 2017-2018 boom is unlikely to be needed in the next two to three years, especially as there are significant risks to the downside.

Demand will be below peak (i.e. 2018) levels of production until 2022. In mid-2019, we identified c.205Mt extra global crude steel capacity to be installed between 2019-2023.

Some of this capacity has already been built, including plants in the U.S. and Southeast Asia. While some capacity is still planned to come online, Covid-19 is likely to lead to delays. However, projects still at the planning stage may be cancelled. Investments are less likely in regions already suffering from excess capacity.

Further Covid-19 Demand Destruction is a Downside Risk

We have developed three scenarios based on the impact Covid-19 could have on the economic recovery. This outlook is aligned to the base case. Our downside scenario is based on “multiple waves” of Covid-19. In this case, demand destruction is likely to be higher, leading to a greater contraction of flat products demand in 2020 and a further reduction in 2021.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com