Market Data

June 3, 2019

Global Steel Production: China's Share Tops 54 Percent

Written by Peter Wright

China’s crude steel production in April exceeded an annualized rate of one billion tons for the first time as the Asian giant continues to grow its global market share, according to Steel Market Update’s analysis of the latest World Steel Association data.

On March 27, the OECD Steel Committee reported: “Low growth prospects for the global economy, slowing demand for steel and virtually unchanged steelmaking capacity are driving severe and persistent excess capacity in the steel sector. The Committee reiterated the need for capacity reductions in relevant economies and for the removal of subsidies and other support measures that are distorting steel markets. The Committee said that if planned new steel plants, some in regions where excess capacity is already prevalent, become operational, global steelmaking capacity could increase by 4-5% between 2019 and 2021. It called for the G20-led Global Forum on Steel Excess Capacity to swiftly implement agreed policy actions to eliminate excess capacity and market-distorting support measures, and expressed support for the continuation of the Forum’s work. The Committee also discussed recent trade measures affecting steel and steelmaking raw materials, with several delegations expressing concern about the impact of certain trade measures on steel trade flows, as well as the effect of these measures in prompting trade measures in other jurisdictions. Excess capacity remained high at 425.5 million tonnes in 2018.”

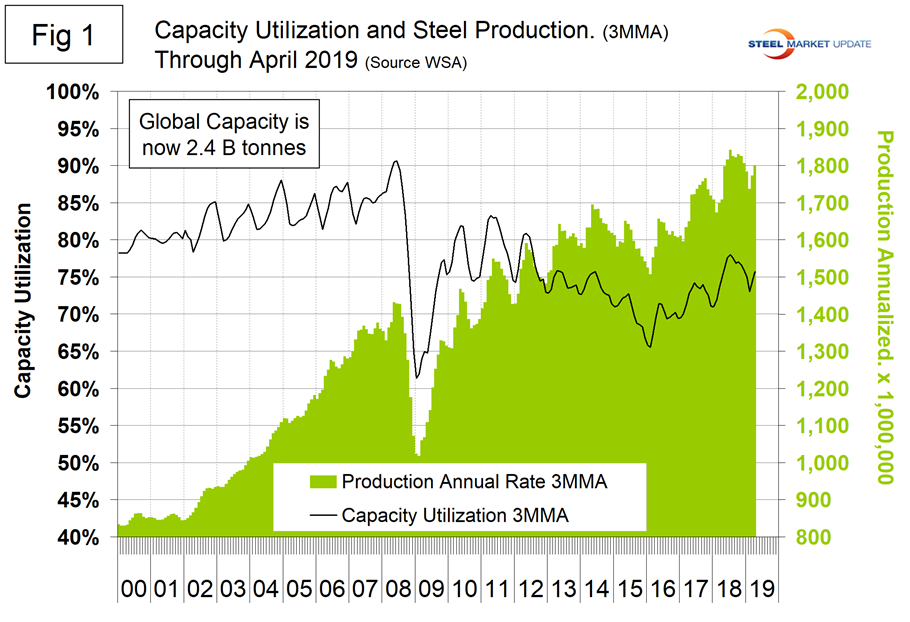

Global steel production in April hit an all-time high annual rate of 1.880 billion metric tons (Mt). Capacity is calculated to be 2.4 billion Mt and capacity utilization in April was 80.0 percent, according to the WSA. In the month of April, Chinese production exceeded an annual rate of one billion metric tons and in three months through April produced an all-time global share of 54.3 percent.

Figure 1 shows annualized monthly production on a three-month moving average (3MMA) basis and capacity utilization since April 2000. On a tons-per-day basis, production in April was 5.222 billion Mt, another all-time high.

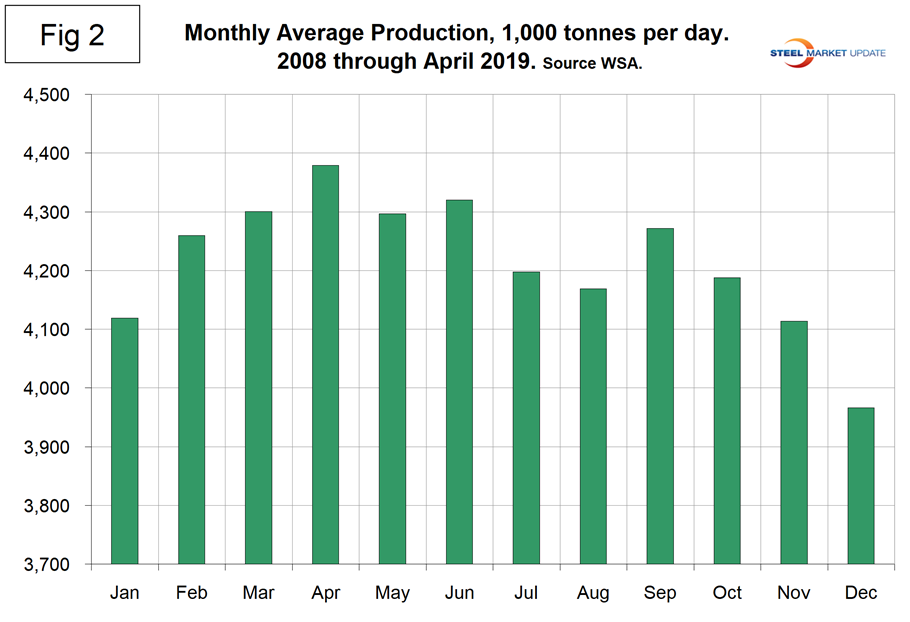

On average, global production on a tons-per-day basis peaked in the early summer in the years 2010 through 2016, but in 2017 and 2018 the second half downtrend was delayed until the fourth quarter, on a 3MMA basis. Figure 2 shows the average tons per day of production for each month since 2008. On average, April increased by 1.81 percent. This year April increased by 4.34 percent.

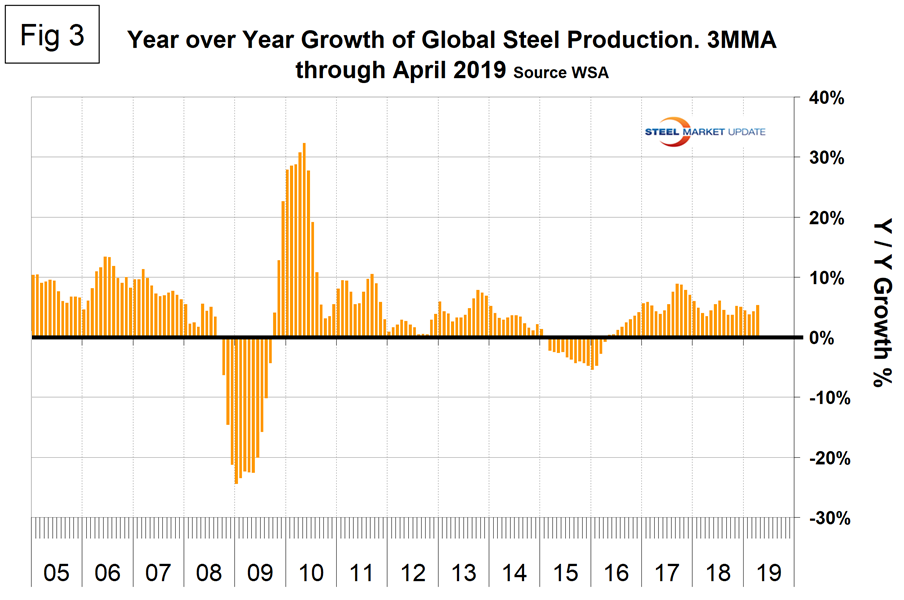

Figure 3 shows the year-over-year growth rate of global production since April 2005. Growth in three months through April was 5.4 percent, the highest growth rate since last July. Note, this is not a seasonal effect as we are considering year-over-year changes.

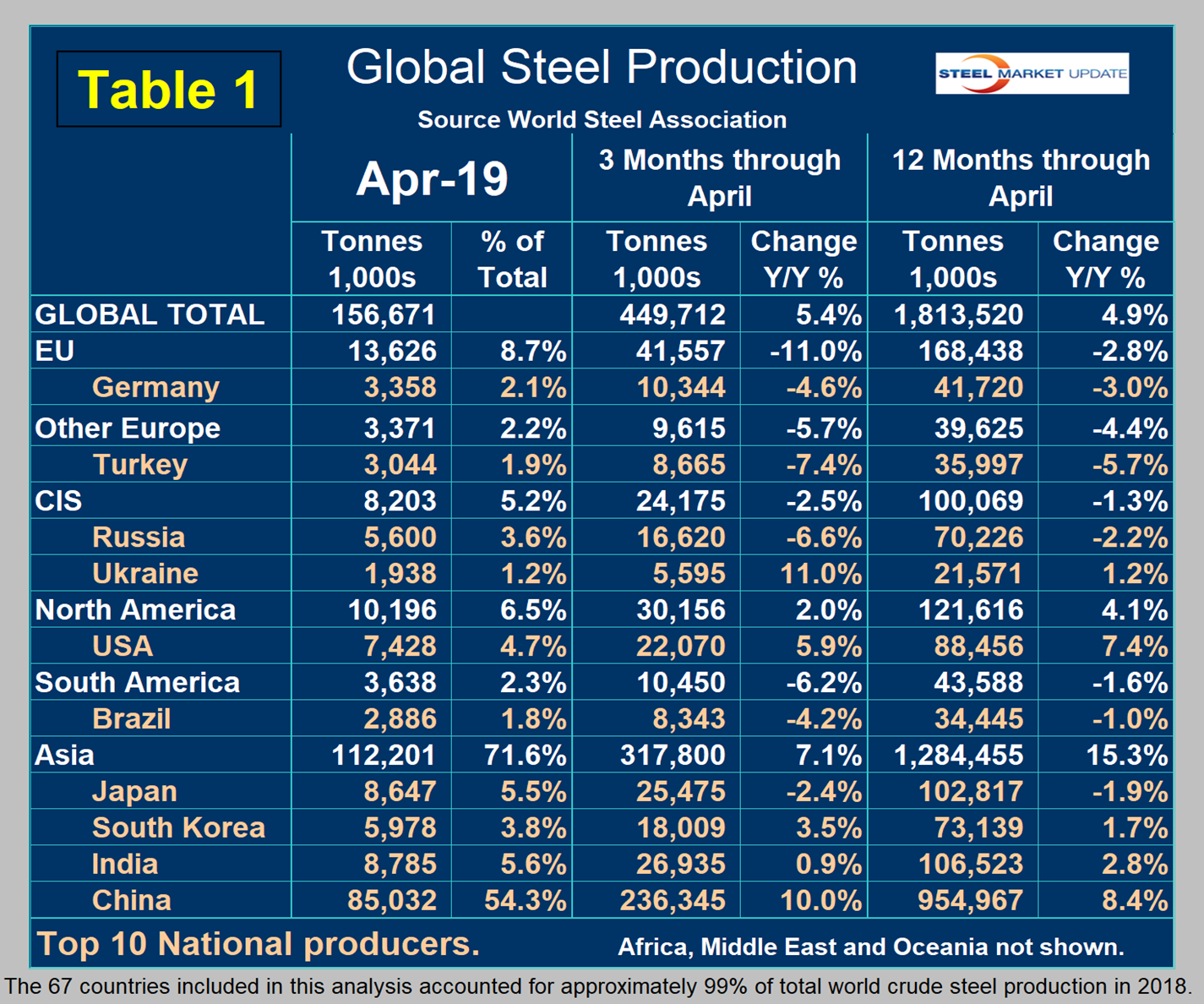

Table 1 shows global production broken down into regions, the production of the top 10 nations in the single month of April, and their share of the global total. It also shows the latest three months and 12 months of production through April with year-over-year growth rates for each period. Regions are shown in white font and individual nations in beige. The world overall had positive growth of 5.4 percent in three months and 4.9 percent in 12 months through April. When the three-month growth rate is higher than the 12-month growth rate, as it was in April, we interpret this to be a sign of positive momentum. On the same basis in April, China grew by 10.1 percent and 8.4 percent, and therefore also had positive momentum. All regions except North America and Asia had negative growth in three months through April year-over-year. Table 1 shows that North America was up by 2.0 percent in three months. Within North America, production was up by 5.9 percent in the U.S., down by 0.7 percent in Canada and down by 7.0 percent in Mexico. (Canada and Mexico are not shown in Table 1.)

In the 12 months of 2018, 119.9 million metric tons were produced in North America of which 72.3 percent was produced in the U.S., 10.9 percent in Canada and 16.8 percent in Mexico.

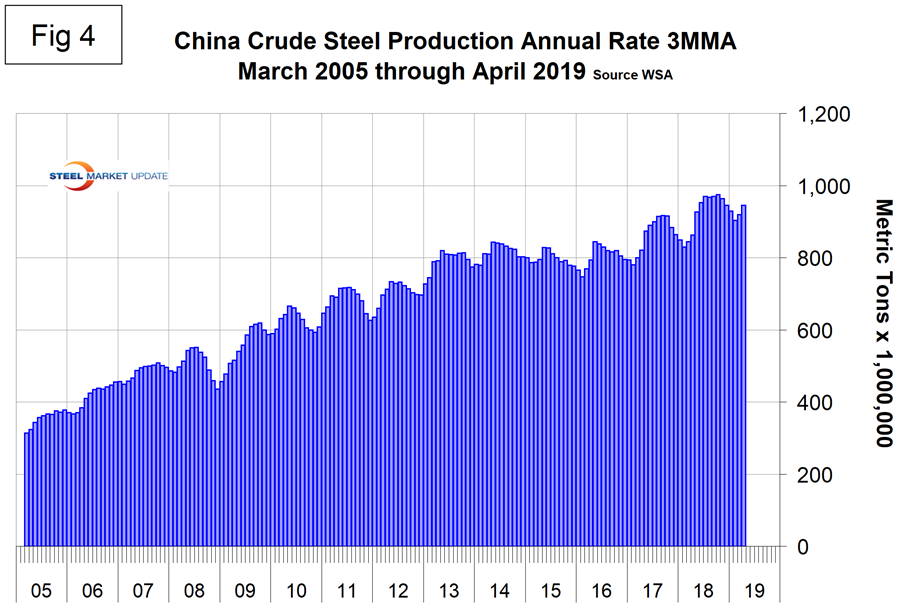

Figure 4 shows China’s production since 2005. As just stated, global steel production was up by 5.4 percent in three months through April year-over-year and China was up by 10.0 percent, both with positive momentum. This misses the main point, though, because in the three months January through March world steel production excluding China contracted. In April, the rest of the world production expanded by 0.6 percent.

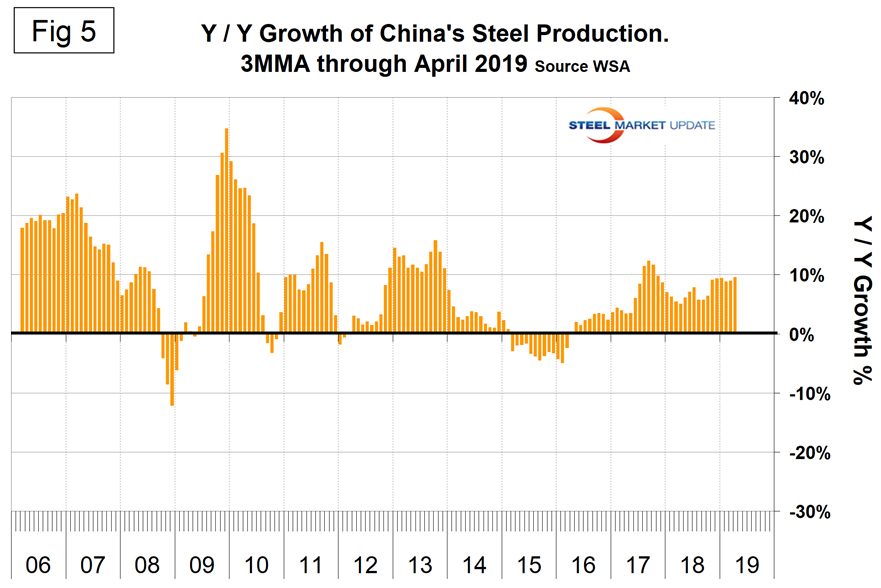

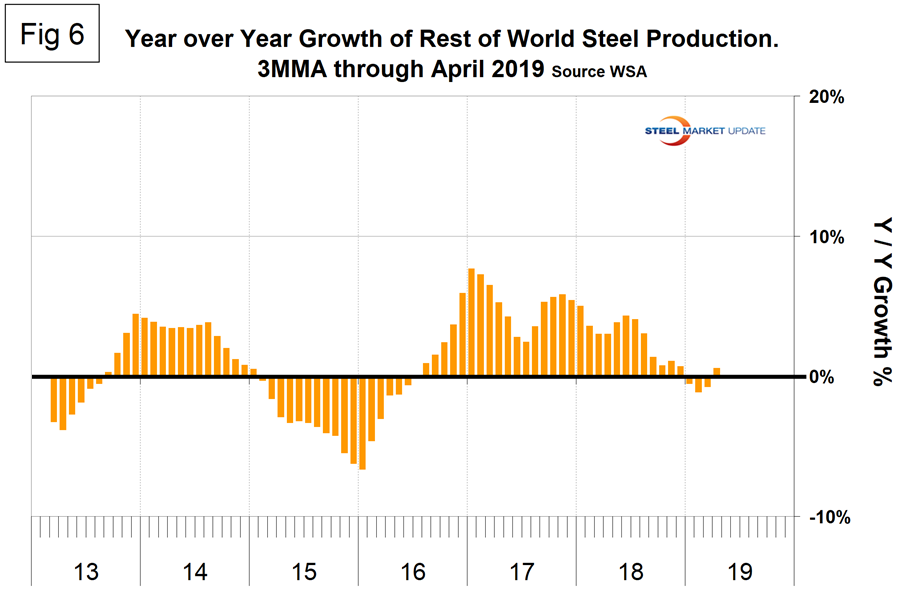

Figure 5 shows the growth of China’s steel production since January 2013 and Figure 6 shows the growth of global steel excluding China. Both to the same scale and time period. China’s domination of the global steel market is increasing and in April for the first time had an annualized production rate of over one billion metric tons. The WSA is forecasting a deceleration in China’s steel production growth in 2019. The chairman of WSA’s economics committee stated recently that China is expected to experience zero growth in 2019, down from 6 percent in 2018. This is partly a result of trade tensions with the U.S.

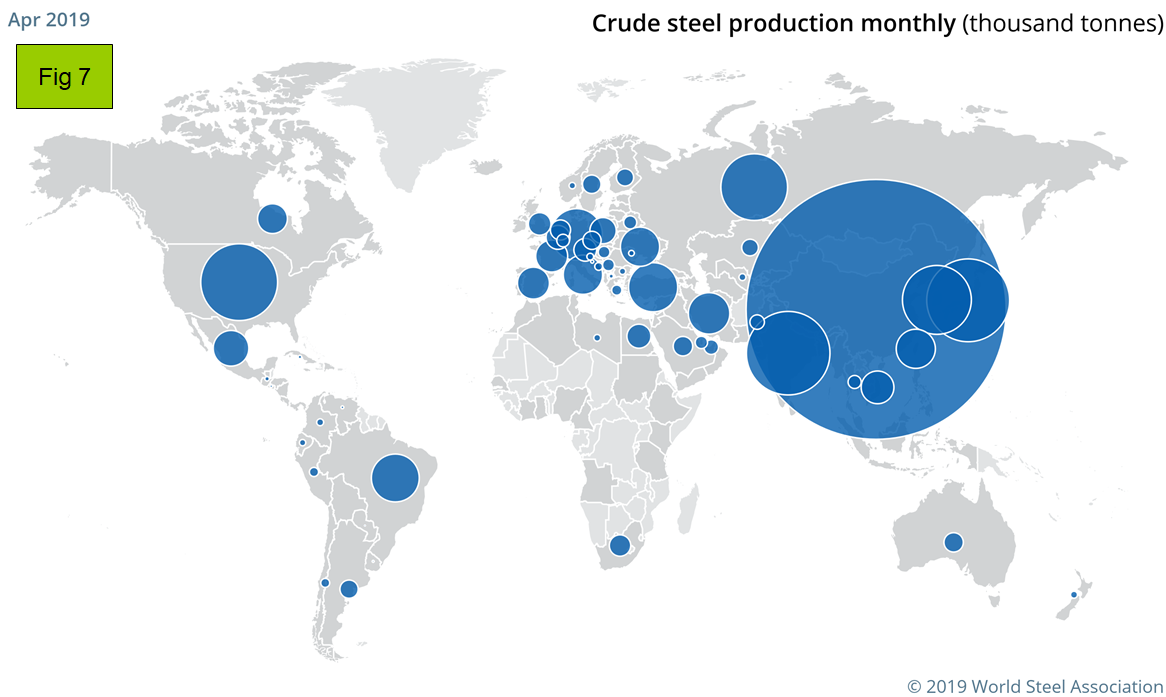

Figure 7 is a visual from the WSA showing the relative size of production in various countries.

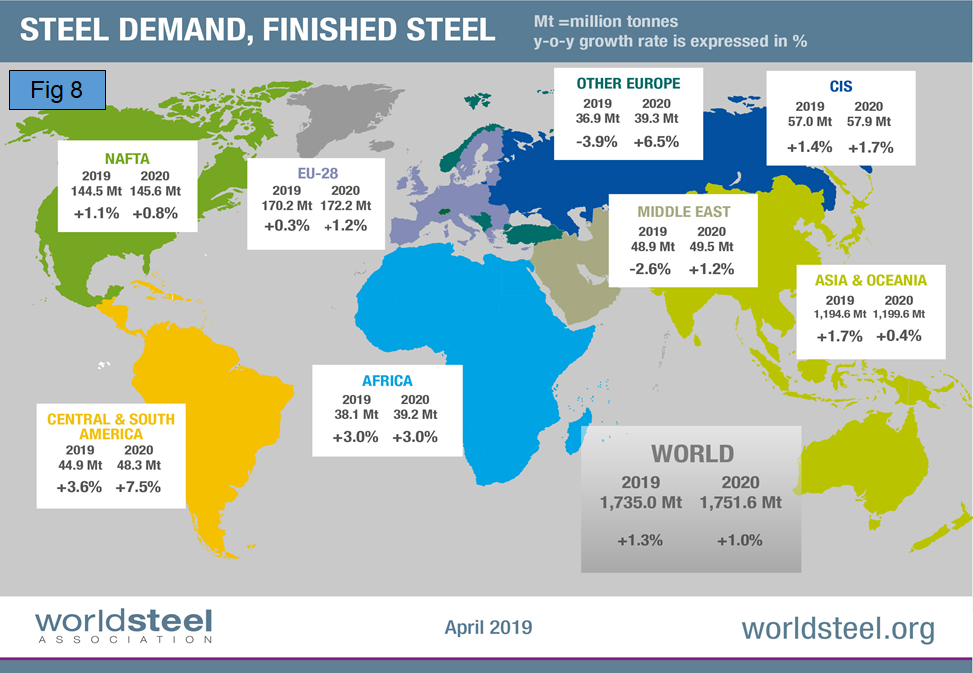

The April 2019 WSA Short Range Outlook (SRO) for apparent steel consumption in 2018 and 2019 is shown by region in Figure 8. The WSA forecasts global steel demand will reach 1.735 billion Mt in 2019, an increase of 1.3 percent over 2018. (Note, the essence of this piece is crude steel production, therefore the numbers are greater than for steel consumption, which relates to rolled products.)

Commenting on the outlook, the chairman of WSA’s economics committee said, “In 2017-18, steel demand in the U.S. benefitted from the strong growth of the economy driven by government-led fiscal stimulus, leading to high confidence and a robust job market. In 2019, the U.S. growth pattern is expected to slow with the waning effect of fiscal stimulus and a monetary policy normalization. Therefore, both construction and manufacturing growth is expected to moderate. Investment in oil and gas exploration is expected to decelerate as well, while a boost in infrastructure spending is not expected.”

SMU Comment: China continues to expand its steel production, and the global steel community as represented by the WSA continues to be complacent about it. In their October statement, WSA said they expected the growth of China’s steel production in 2019 to be zero. Now they are saying, “In 2020, a minor contraction in Chinese steel demand is forecasted as government-led stimulus effects are expected to subside.” New plants are coming on stream in China and almost all of these are BOF-based, according to the August report by the OECD Steel Committee.

This analysis is based on data made public monthly by the World Steel Association. The WSA is one of the largest industry associations in the world. Members represent approximately 85 percent of the world’s steel production, including over 160 steel producers, national and regional steel industry associations and steel research institutes.