Market Data

March 21, 2019

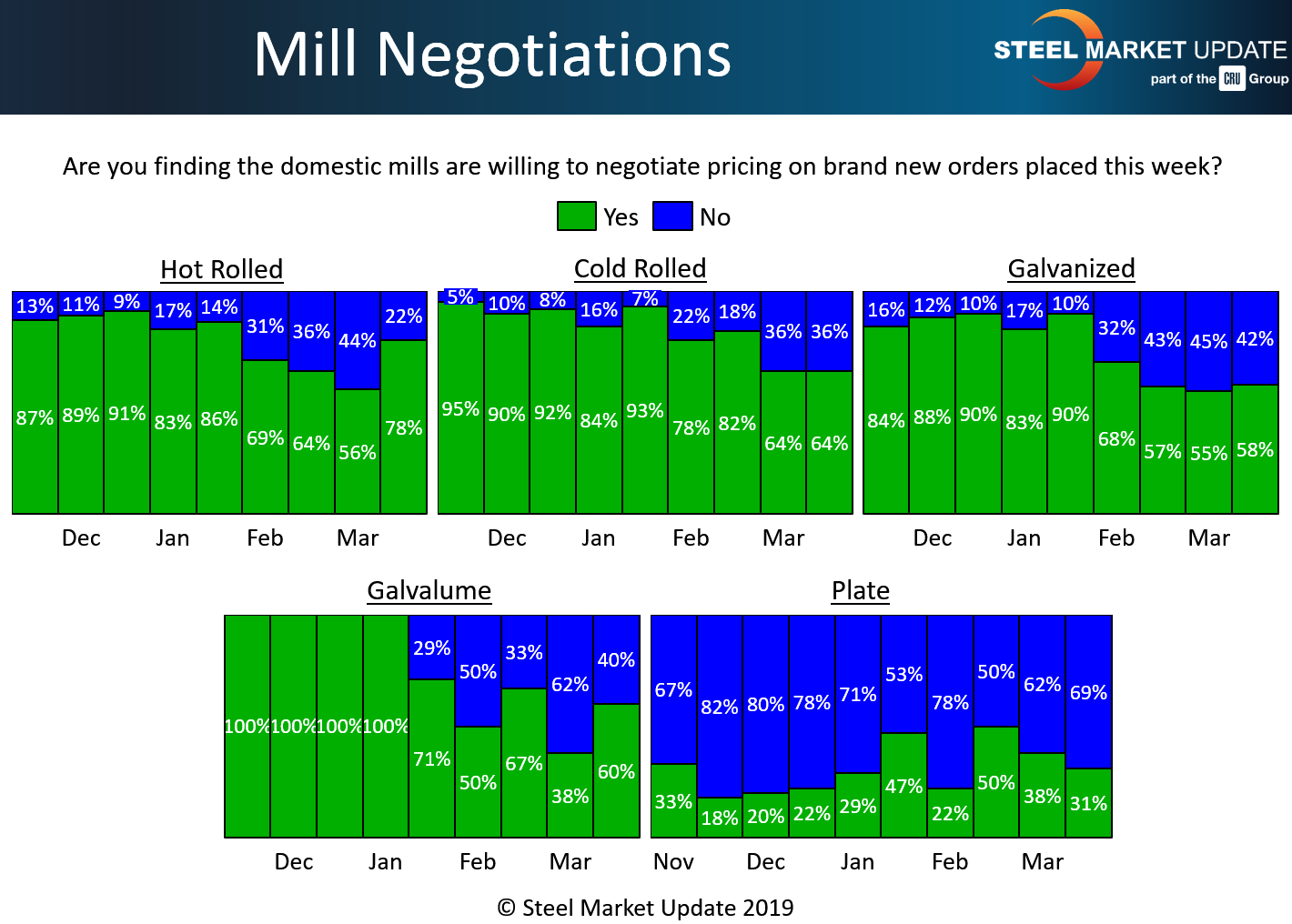

Steel Mill Negotiations: Price Still on the Table

Written by Tim Triplett

Mills are still willing to negotiate on price, especially on hot rolled, even as they work to collect the two $40 per ton price increases they announced in January and February. In every product category except plate, the majority of respondents to Steel Market Update’s questionnaire this week reported mills willing to talk price.

Most notably, 78 percent of respondents said the mills are open to price negotiations on hot rolled, up double digits from the 56 percent in early March. Just 22 percent said the mills are currently holding the line on HR.

In the cold rolled segment, the tone of talks has seen little change this month as 64 percent continued to report the mills open to price negotiations, while 36 percent reported current cold rolled prices as firm.

In the galvanized sector, 58 percent said the mills were open to price discussions, up slightly from 55 percent two weeks ago. About 42 percent of GI buyers report that prices are nonnegotiable. For Galvalume, 60 percent of SMU’s respondents now say the mills are willing to negotiate, while 40 percent say they are not.

Negotiations in the plate market are considerably tighter, with 69 percent of buyers reporting the mills holding firm on plate prices.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.