Market Data

March 7, 2019

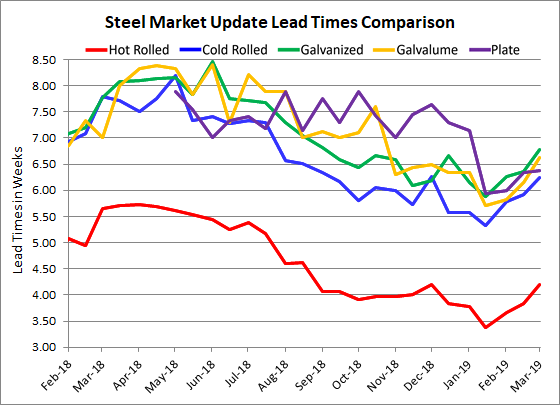

Steel Mill Lead Times: Slowly Moving Out

Written by Tim Triplett

Mill lead times for spot orders of flat rolled steel continue to slowly move out as the market sees upward momentum following the mill price increase announcements in January and February. Hot rolled lead times now average more than four weeks, cold rolled and plate more than six weeks, and galvanized nearing seven weeks.

Lead times for steel delivery are a measure of demand at the mill level. The longer the lead time, the busier the mills. The busier the mills, the less likely they are to negotiate on price.

Hot rolled lead times now average 4.19 weeks, up from 3.38 weeks in mid-January. While significantly longer, current lead times for hot rolled are still well below the 5.65 weeks at this time last year.

Cold rolled orders currently have a lead time of 6.24 weeks, up from 5.33 weeks around Jan. 15, prior to the price increase announcements. Cold rolled lead times were considerably longer at this time last year at 7.79 weeks.

Similarly, over the past six weeks, average lead times for galvanized steel have extended to 6.77 weeks from 5.88 weeks. Galvalume lead times rose to 6.63 weeks from 5.71 weeks during the same period.

Lead times for spot orders of plate steel now average 6.38 weeks, up from 5.93 weeks in mid-January.

As one buyer commented on lead times: “It depends on the mill, the commodity and the material specifications.” Added another: “They very seldom meet the original delivery date anyway.”

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. Our lead times are meant only to identify trends and changes in the marketplace. To see an interactive history of our Steel Mill Lead Times data, visit our website here.