Market Data

January 10, 2019

Steel Mill Negotiations: A Subtle Shift

Written by Tim Triplett

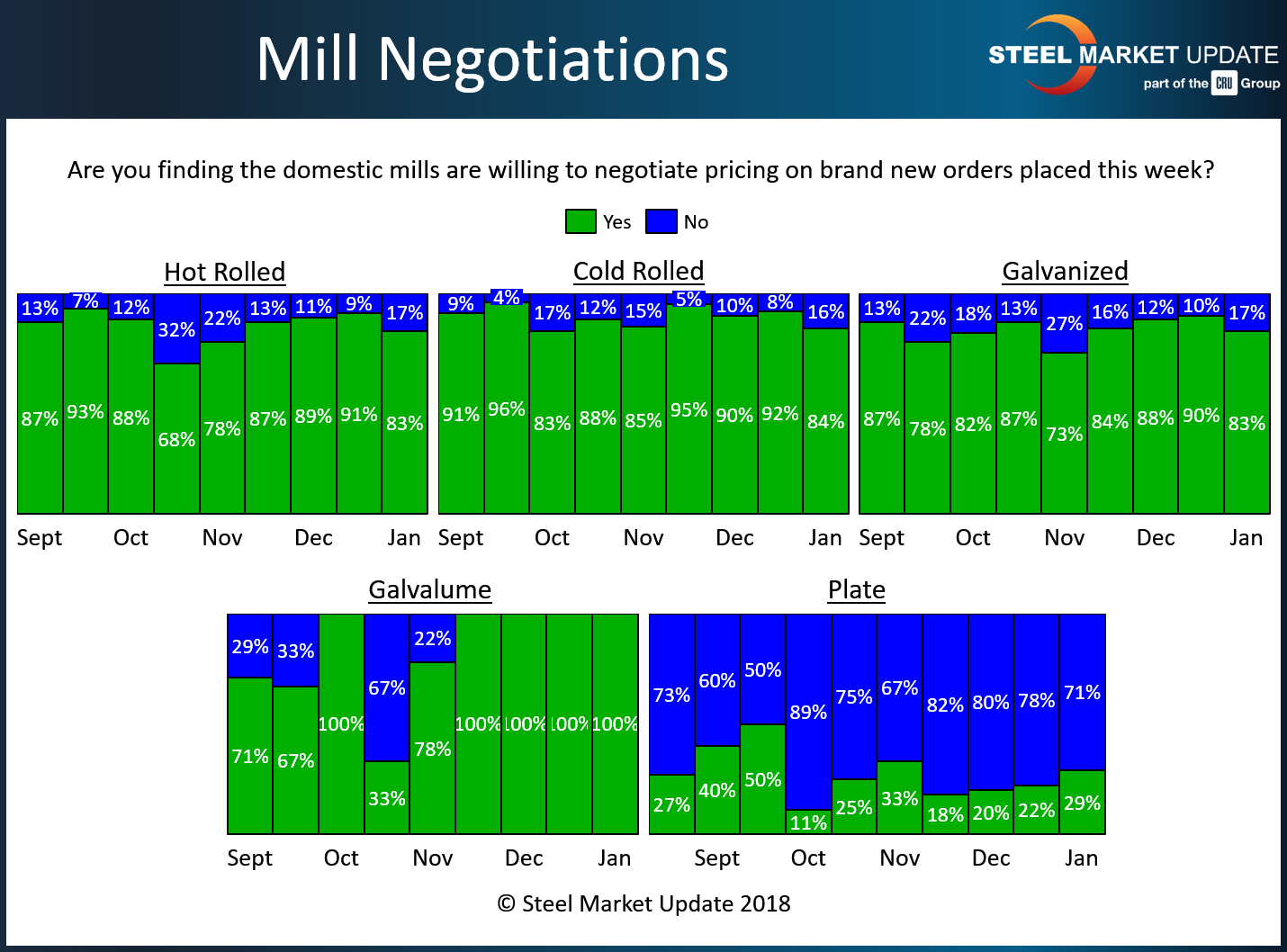

Steel Market Update’s first canvass of the new year shows a subtle shift in the price dynamic between mills and steel buyers. No doubt, buyers still have a lot of leverage and most mills are usually willing to talk price to secure the order. But SMU’s findings show a slight tightening in negotiations.

In the hot rolled category, 83 percent of buyers responding to SMU’s questionnaire said they have found mills willing to talk price. That’s a high percentage, but it’s down from 91 percent in mid-December. About 17 percent say the mills are now holding the line on HR.

In the cold rolled segment, 84 percent said they have found mills open to price negotiation, down from 92 percent two weeks ago. About 16 percent reported current mill prices on cold rolled as firm, double the percentage in the last poll.

The same trend is true in coated products. In the galvanized sector, 83 percent said the mills were open to price discussions, down from 90 percent last month. About 17 percent of GI buyers report that prices are nonnegotiable, up from 10 percent last month. For Galvalume, virtually all respondents reported AZ prices as open to negotiation.

Demand for plate steel continues to outpace supplies, with buyers on allocation and lead times extended. The vast majority of plate buyers, about 71 percent, say the mills remain unwilling to talk price. But a month ago, that figure was 80 percent. This nine-point difference may be an early sign of supply and demand in the plate segment starting to balance out.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.