Market Data

December 6, 2018

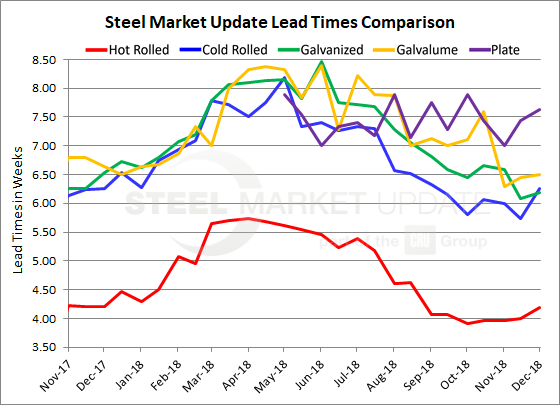

Steel Mill Lead Times: Have We Seen the Bottom?

Written by Tim Triplett

Lead times for spot orders of hot rolled and cold rolled steels appear to have bottomed and extended a bit in early December. Lead times on HR and CR have not been this long since September, but are well below the levels seen when prices were spiking earlier this year. Lead times for steel delivery are a measure of demand at the mill level—the longer the lead time, the busier the mill. The busier the mill, the less likely they are to negotiate on price. Lead times for hot rolled now average a bit over four weeks, cold rolled and galvanized a bit over six weeks, and Galvalume about six and a half weeks.

Hot rolled lead times now average 4.19 weeks, up from 3.97 weeks a month ago, and about the same as they were at this time last year. Until the past few weeks, lead times for HR had declined steadily since peaking at 5.73 weeks in April.

Cold rolled orders currently have a lead time of 6.26 weeks, up from 5.73 weeks in mid-November. CR lead times peaked in May this year at 8.19 weeks.

Galvanized lead times, which have declined from 8.46 weeks in June, have leveled out in the past month at around 6.19 weeks.

At 6.50 weeks, Galvalume lead times are up slightly from 6.30 weeks one month ago. AZ lead times hit their peak this year at 8.40 weeks in June.

It’s too early to tell if lead times are poised to do an about-face and begin increasing ahead of the strong steel demand forecast for the first quarter, but it appears the rate of decline is at least slowing for most flat rolled products.

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. Our lead times are meant only to identify trends and changes in the marketplace. To see an interactive history of our Steel Mill Lead Times data, visit our website here.