Market Data

June 4, 2018

Net Job Creation through May 2018

Written by Peter Wright

Net job creation in May hit 223,000 seasonally adjusted. Year over year, 2,363,000 jobs have been created, an increase of 1.6 percent, according to Bureau of Labor Statistics employment data.

Rising employment and wages are the basis of GDP growth because personal consumption accounts for almost 70 percent of GDP. Steel consumption is related to GDP; therefore, we need to be aware of changes to the employment picture. Net job creation in May, as reported by the BLS on Friday, was up by 64,000 from April’s downwardly revised count. In this context, net means the difference between gains and losses, which are both much larger numbers than we are used to considering. Over a seven-year period, gains averaged 7,211,000 per quarter as losses averaged 6,597,000 on the same basis.

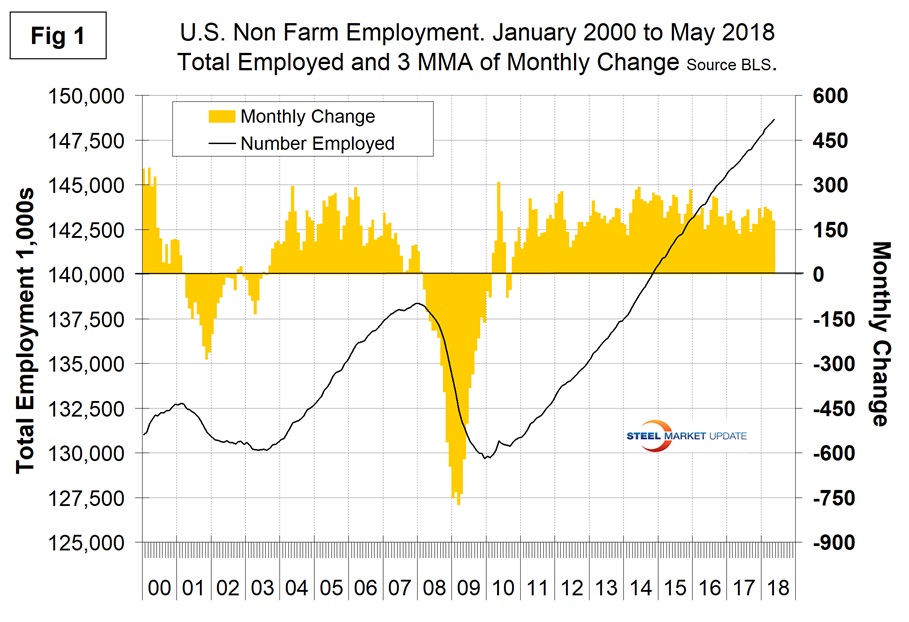

Figure 1 shows the 3MMA of the number of jobs created monthly since 2000 as the brown bars and the total number employed as the black line. These numbers are seasonally adjusted by the BLS, which has been criticized in the past for the ineffectiveness of its seasonal adjustment calculations.

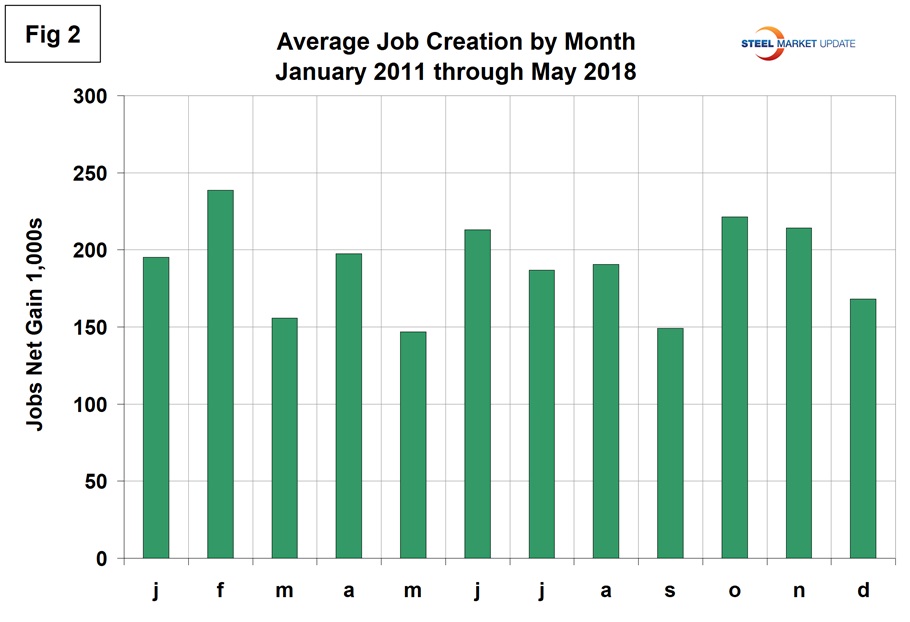

To examine if any seasonality is left in the data after adjustment, we have developed Figure 2. In the eight years since and including 2011, May on average had the lowest number of jobs created of any month of the year, which we attribute to poor seasonal adjustment. On average in those years, May has decreased by 26 percent. This year May rose by 40 percent, therefore much better than the historical norm. In the May report, job creation in March was revised up by 20,000 and April down by 9,000 jobs.

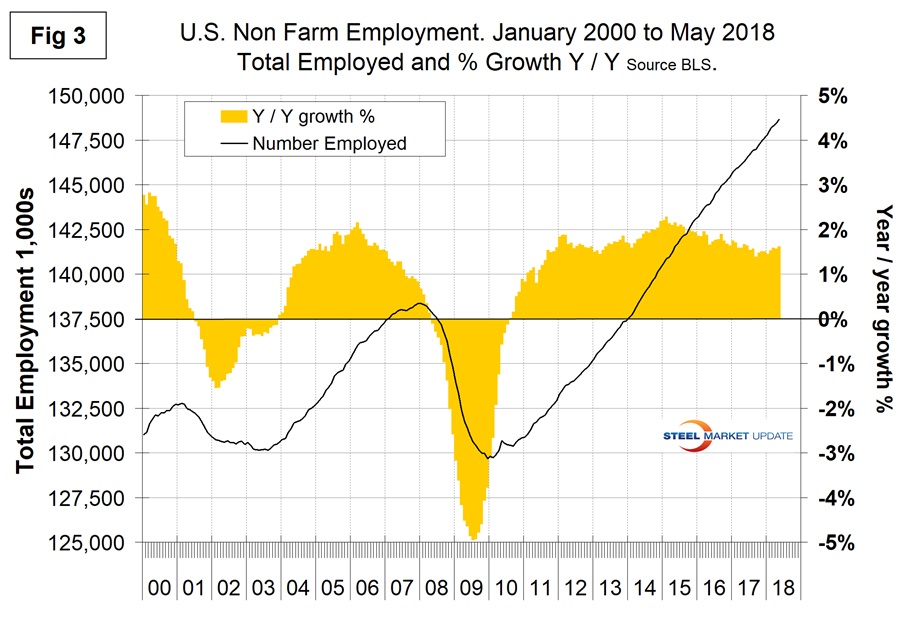

In order to get a better look at whether the situation is improving or deteriorating, we have developed Figure 3 for the first time this month. This shows the same total employment line as Figure 1, but includes the year-over-year growth on a percentage basis. From this we conclude there has been a small gradual improvement since September last year.

Total nonfarm payrolls are now 10,297,000 more than they were at the pre-recession high of February 2008. Total nonfarm employment in May was 148.662 million. According to BLS data, the average workweek for all employees on private nonfarm payrolls was unchanged at 34.5 hours in May. In manufacturing, the workweek decreased by 0.2 hour to 40.8 hours, and overtime edged down by 0.2 hour to 3.5 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls remained at 33.8 hours. In May, average hourly earnings for all employees on private nonfarm payrolls rose by 8 cents to $26.92. Over the year, average hourly earnings have increased by 71 cents or 2.7 percent.

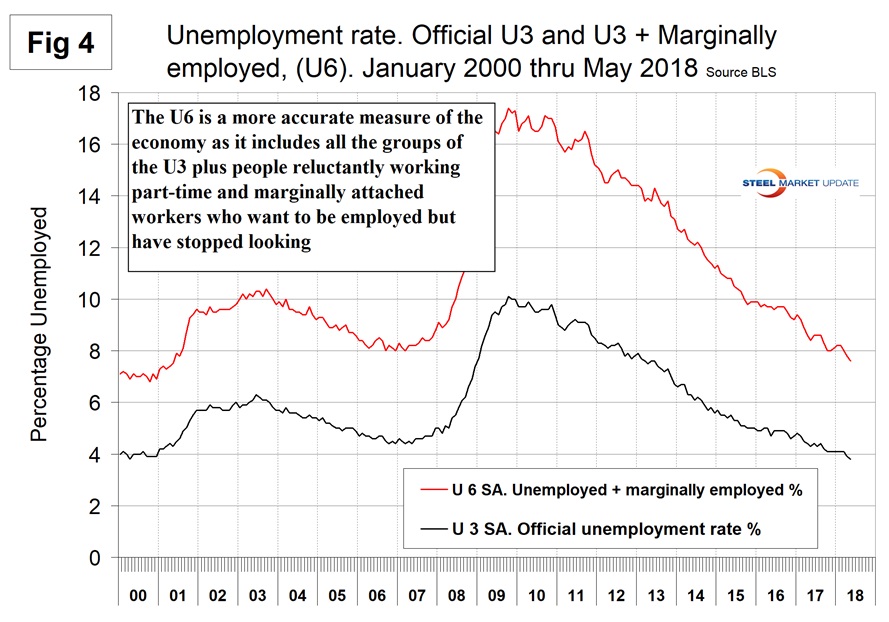

The official unemployment rate, U3, reported in the BLS Household survey (see explanation below) came in at 3.8 percent, down from 3.9 percent in April and the lowest value since our data stream began in January 2000 when the rate was 3.8 percent. This is not a very representative number. The more comprehensive U6 unemployment rate declined from 9.2 percent in January last year to 7.6 percent in this latest report (Figure 4). U6 includes individuals working part time who desire full-time work and those who want to work but are so discouraged they have stopped looking. The differential between these rates was usually less than 4 percent before the recession; in May it was 3.8 percent.

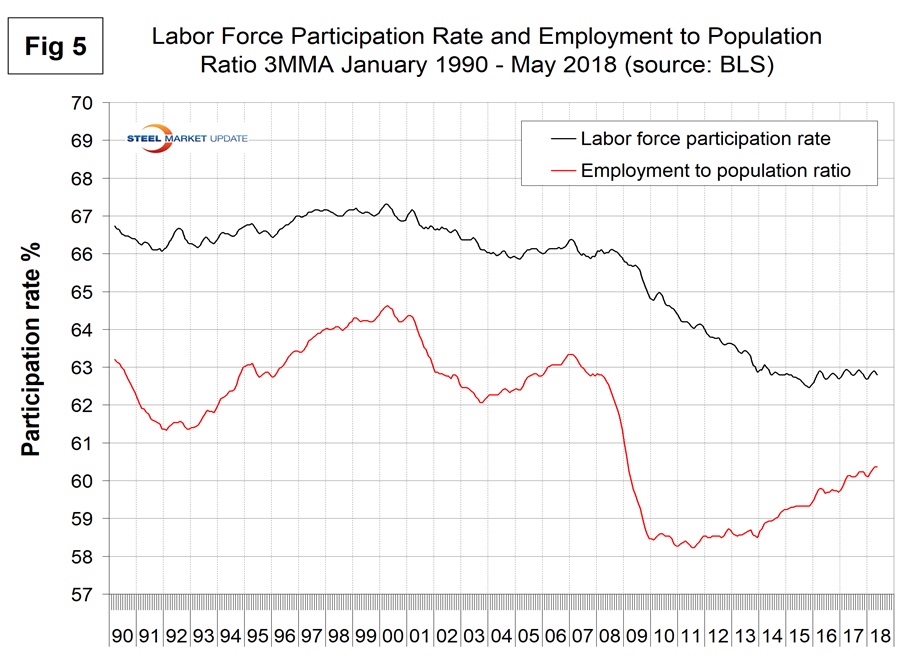

The employment participation rate is calculated by dividing the number of people actively participating in the labor force by the total number of people eligible to participate. This measure was 62.8 percent in May, the same as it was in May two years ago. Another gauge is the number employed as a percentage of the population, which we think is more definitive. In May, the employment-to-population ratio was 60.4 percent, up from 59.7 percent in May 2016. The employment-to-population ratio has made progress for the last four years, but the labor force participation rate has been stalled for two years. Figure 5 shows both measures on one graph.

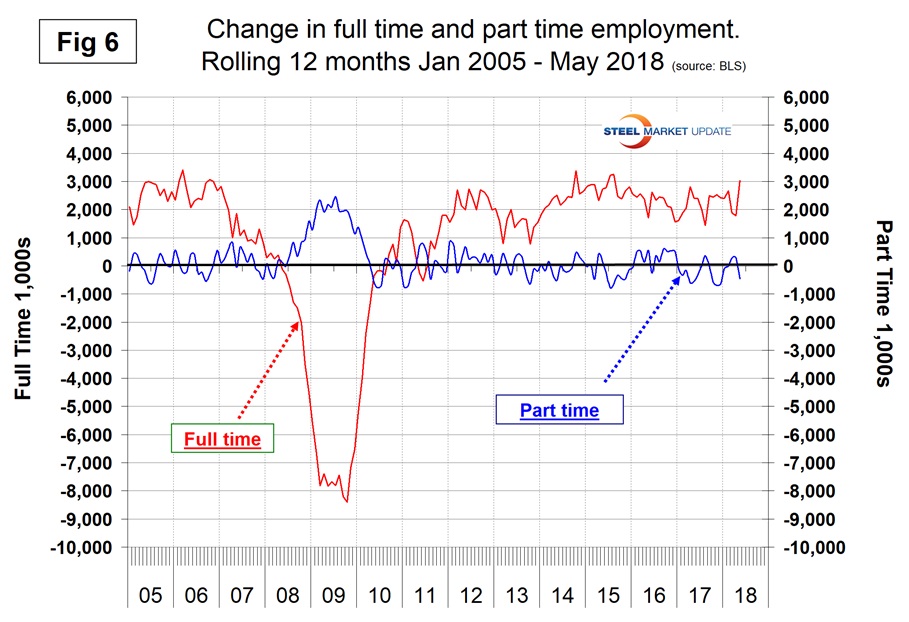

In the 29 months since and including January 2016, there has been an increase of 5,917,000 full-time and a decrease of 495,000 part-time jobs. Figure 6 shows the rolling 12-month change in both part-time and full-time employment. This data comes from the household survey and part-time is defined as less than 35 hours per week. Because the full-time/part-time data comes from the household survey and the headline job creation number comes from the establishment survey, the two cannot be compared in any given month. To overcome the volatility in the part-time numbers, we must look at longer time periods than a month or even a quarter, which is why we look at a rolling 12 months for the full-time and part-time employment picture shown in Figure 6.

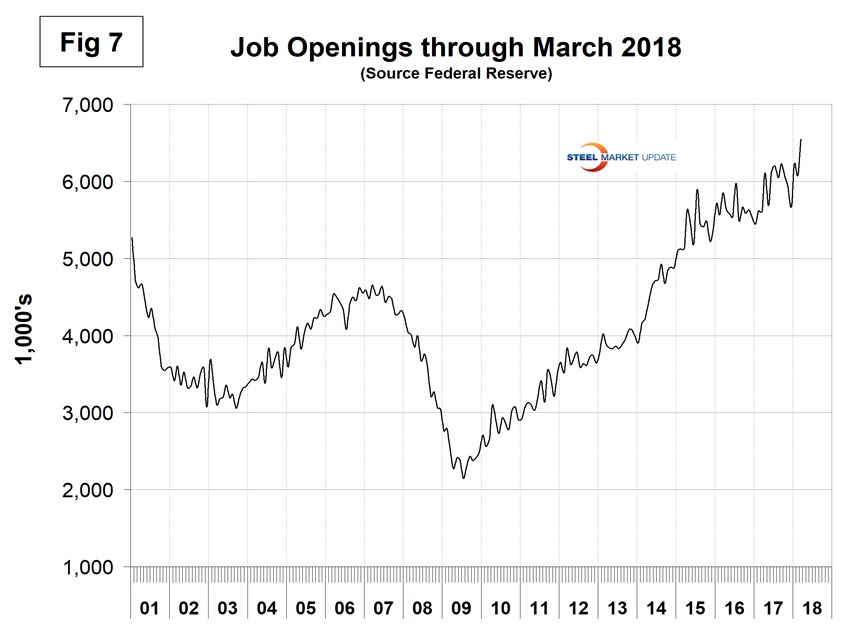

The job openings report known as JOLTS is reported on or about the 10th of the month by the Federal Reserve and is over a month in arrears. Figure 7 shows the history of unfilled job openings through March when openings stood at 6,550, which was the highest in the history of our data. There has been an improving trend since mid-2009.

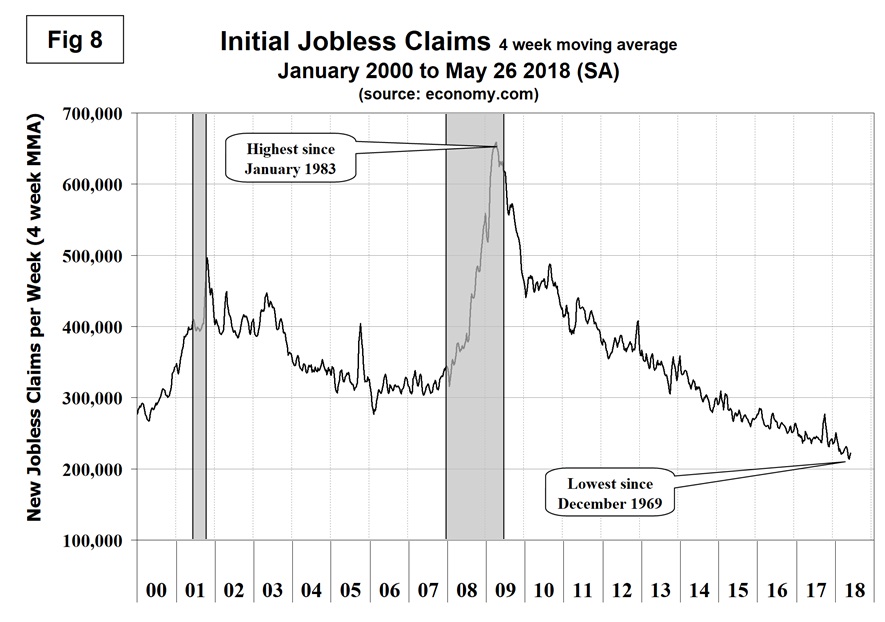

Initial claims for unemployment insurance, reported weekly by the Department of Labor, flattened in 2017 except for the hurricane-driven spike, then resumed their decline in 2018. New claims in April and May were at the lowest level since 1969. In the week ending May 28, initial claims were 221,000 with a four-week moving average of 222,250 claims. This is a continuation of the longest streak since 1973 of initial claims below 300,000 (Figure 8).

SMU Comment: As 2018 unfolds, the employment situation is very good, job openings are at an all-time high, and new claims for unemployment are at a 44-year low. The employment situation has been described as “full” by some analysts. Unit labor costs were up in Q4 2017 and Q1 2018.

Explanation: On the first Friday of each month, the Bureau of Labor Statistics releases the employment data for the previous month. Data is available at www.bls.gov. The BLS reports on the results of two surveys. The Establishment survey reports the actual number employed by industry. The Household survey reports on the unemployment rate, participation rate, earnings, average workweek, the breakout into full-time and part-time workers and lots more details describing the age breakdown of the unemployed, reasons for and duration of unemployment.

At Steel Market Update, we track the job creation numbers by many different categories. The BLS database is a reality check for other economic data streams such as manufacturing and construction. We include the net job creation figures for those two sectors in our “Key Indicators” report. It is easy to drill down into the BLS database to obtain employment data for many subsectors of the economy. For example, among hundreds of sub-indexes are truck transportation, auto production and primary metals production. The important point about all these data streams is the direction in which they are headed. Whenever possible, we try to track three separate data sources for a given steel-related sector of the economy. We believe this gives a reasonable picture of market direction. The BLS data is one of the most important sources of fine-grained economic data that we use in our analyses. The states also collect their own employment numbers independently of the BLS. The compiled state data compares well with the federal data. Every three months, SMU examines the state data and provides a regional report, which indicates strength or weakness on a geographic basis. Reports by individual state can be produced on request.